When it comes to iconic American automakers, General Motors GM and Ford F remain two of the industry’s strongest pillars. Both companies delivered stronger-than-expected first-quarter 2026 earnings, raised guidance, and benefited from tariff refunds. While the headline beat may look encouraging, is it enough to justify fresh investments? Or do near-term risks still cloud the outlook? Let’s break down which stock currently has the edge.

Q1 Results Review

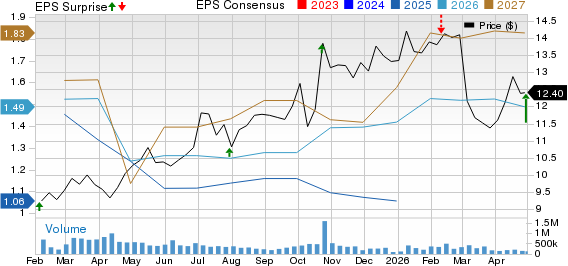

Ford’s first-quarter 2026 adjusted EPS of 66 cents surpassed the Zacks Consensus Estimate of 20 cents and jumped from 14 cents recorded in the year-ago quarter. The company’s consolidated first-quarter revenues came in at $43.3 billion, up 6% year over year. F’s total automotive revenues came in at $39.82 billion, beating the Zacks Consensus Estimate of $39.4 billion and rising from $37.42 billion generated a year ago.

Revenues from Ford Blue grew 14% year over year, while Ford Pro continues to deliver the strongest margins. Ford Pro is supported by strong order books and expanding software and service offerings. Strength across vehicles, software and physical services underpins the segment’s momentum. Paid software subscriptions rose 30% to 879,000 in the first quarter.

Ford Motor Company Price, Consensus and EPS Surprise

Ford Motor Company price-consensus-eps-surprise-chart | Ford Motor Company Quote

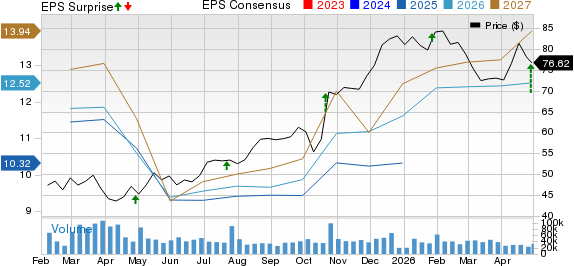

General Motors’ first-quarter 2026 adjusted EPS of $3.70 beat the Zacks Consensus Estimate of $2.61 and increased from the year-ago quarter’s $2.78. However, revenues of $43.62 billion slipped 0.9% year over year and missed the consensus mark of $43.94 billion.

General Motors is building a larger recurring revenue base from OnStar and Super Cruise. In first-quarter 2026, recognized digital revenues exceeded $750 million, up more than 20% year over year, and deferred revenues reached $5.8 billion, up more than 50%. Management expects recognized digital revenues of about $3.1 billion in 2026 and deferred revenues close to $7.5 billion by year end as subscribers rise to roughly 13 million. Super Cruise customers have driven 1 billion hands-free miles, and paid subscribers are expected to exceed 850,000 by the end of 2026.

General Motors Company Price, Consensus and EPS Surprise

General Motors Company price-consensus-eps-surprise-chart | General Motors Company Quote

GM & F Gain From Tariff Adjustment & Lift 2026 View

General Motors increased full-year 2026 EBIT-adjusted guidance to $13.5-$15.5 billion (versus $13-$15 billion guided earlier) and lifted its adjusted earnings outlook to $11.50-$13.50 per share (compared with the prior forecast of $11-$13 per share). That was primarily due to the adjustment of about 500 million tied to a U.S. Supreme Court decision regarding certain tariffs paid under the International Emergency Economic Powers Act (IEEPA).

Ford also highlighted a $1.3 billion IEEPA tariff refund and, as a result, raised its full-year outlook. It raised its adjusted EBIT guidance to a range of $8.5-$10.5 billion from $8-$10 billion. EBIT expectation for the Ford Blue unit has been raised from $4-$4.5 billion to $4.5-$5 billion.

Rising Costs & Macro Risks Remain a Concern

Despite the upward revisions, both automakers flagged meaningful cost pressures ahead. Ford noted that its guidance does not factor in a prolonged Middle East conflict, which could keep oil prices elevated and drive higher logistics and input costs.

Meanwhile, GM acknowledged operational risks to its international business. General Motors raised its commodity inflation outlook for 2026 to $1.5-$2 billion, up by $500 million from prior estimates, reflecting higher logistics and DRAM costs. Ford, too, expects commodity headwinds of about $2 billion, up $1 billion from earlier projections, partly due to higher aluminum sourcing costs after disruptions at a key Novelis plant.

Meanwhile, tariffs remain a sizable burden. GM now expects gross tariff costs of $2.5-$3.5 billion for 2026, while Ford estimates an impact of around $1 billion.

Balance Sheet & Capital Returns of Ford & GM

In first-quarter 2026, GM repurchased 800 million of stock, retiring about 11 million shares and ended the quarter with $5.5 billion remaining under its repurchase authorization. The company also declared a quarterly dividend of 18 cents per share. GM ended first-quarter 2026 with over $19 billion of automotive cash, giving flexibility to invest while returning excess capital to shareholders.

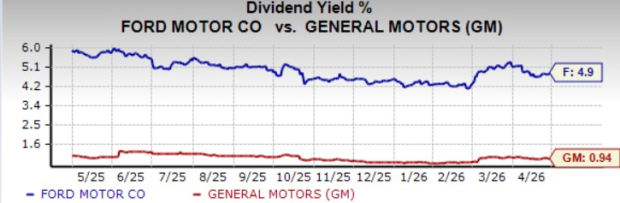

Ford ended the first quarter of 2026 with roughly $43 billion in liquidity, including $17.6 billion in cash (including Ford Credit). Ford’s superior liquidity profile provides a solid foundation for investment in Ford+ priorities. It declared a dividend of 15 cents. But Ford’s dividend yield of roughly 5% is way better than General Motors (less than 1%).

Who Wins Now: Ford or General Motors?

Despite solid first-quarter beats and raised guidance, neither General Motors nor Ford appears to be a compelling fresh buy, as tariff exposure, rising commodity costs, and macro uncertainties could put pressure on near-term performance. Both F and GM carry a Zacks Rank #3 (Hold) and have a Value Score of A. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

The Zacks Consensus Estimate for F and GM’s 2026 EPS estimates have been revised down by 1 cent and 2 cents to $1.49 and $12.42, respectively, in the past seven days.

However, for long-term investors, Ford seems to edge ahead. Its higher dividend yield offers immediate income support, while its strategic pivot toward smaller, affordable EVs—led by a $30,000 pickup on its Universal EV platform—signals a more pragmatic path to profitability. At the same time, Ford Energy’s push into battery storage leverages its LFP cost advantage and opens a new growth avenue beyond autos. Thus, while caution is warranted in the near term, Ford appears better positioned for balanced, long-term returns.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power .

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Ford Motor Company (F): Free Stock Analysis Report

General Motors Company (GM): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).