Lumen Technologies, Inc. LUMN will report its first-quarter 2026 results on May 5, after the market close.

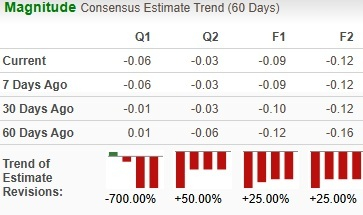

The Zacks Consensus Estimate for the bottom line in the to-be-reported quarter is a loss of 6 cents, compared with a loss of 13 cents reported in the prior-year quarter. The estimate has deteriorated from earnings of 1 cent over the past 60 days.

Image Source: Zacks Investment Research

The consensus estimate for total revenues is pinned at $2.84 billion, down 10.7% year over year.

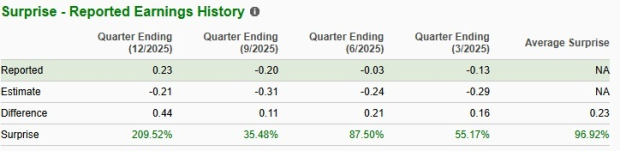

LUMN’s earnings beat the Zacks Consensus Estimate in the trailing four quarters, the average surprise being 96.92%.

Image Source: Zacks Investment Research

What Our Model Predicts for LUMN’s Q1

Our proven model predicts an earnings beat for LUMN this time around. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the chances of an earnings beat. This is the case here. You can uncover the best stocks to buy or sell before they are reported with our Earnings ESP Filter.

LUMN has an Earnings ESP of +27.27% and a Zacks Rank #1 (Strong Buy).

You can see the complete list of today’s Zacks #1 Rank stocks here.

Factors to Focus on Ahead of LUMN’s Q1 Earnings

Investors are likely focused on Lumen’s long-term growth narrative more than near-term revenue trends. The company’s long-term story is tied to its AI-driven network transformation and focus on financial profile.

Lumen has been repositioning itself as an enterprise-focused infrastructure provider, supported by significant balance sheet improvement and strategic realignment.

The explosive growth of AI workloads has been driving demand for low-latency, high-bandwidth fiber connectivity between data centers, cloud regions and enterprise clients, resulting in increasing demand for Lumen's Private Connectivity Fabric (“PCF”) and network-as-a-service (NaaS) solutions. Driven by significant AI-fueled connectivity demand, Lumen secured a total of $13 billion in PCF deals at the end of the fourth quarter of 2025.

However, the revenue contribution from these deals is still in the early stages. Lumen recognized revenues of $41 million and $116 million for the fourth quarter and full-year 2025, respectively, associated with the PCF deals.

Recently, LUMN collaborated with Amazon on AWS Interconnect – last mile, which marks a key step in integrating network connectivity directly into the cloud, enabling enterprises to set up private connections in minutes rather than weeks. This reinforces Lumen’s positioning as a critical enabler of AI and data-intensive workloads.

Lumen Technologies, Inc. Price and EPS Surprise

Lumen Technologies, Inc. price-eps-surprise | Lumen Technologies, Inc. Quote

Beyond PCF, NaaS adoption continues to be one of the most important leading indicators of growth, with its customer base now exceeding 2000. The company reported strong adoption metrics in the fourth quarter, including significant increases in customers, ports and services. NaaS customers were up 29% sequentially in the fourth quarter. Fabric ports deployed increased 31% and the number of services sold surged 26% sequentially. Within NaaS, Internet on Demand, or IoD Offnet is likely to emerge as a strong tailwind.

Cost discipline is likely to boost margins. The company exceeded its 2025 cost-reduction target, achieving more than $400 million in run-rate savings. It now targets $700 million exiting 2026 and $1 billion by year-end 2027. This cost optimization, combined with improving revenue mix, underpins guidance for adjusted EBITDA.

The company has guided 2026 as the year of adjusted EBITDA inflection, with full-year EBITDA expected in the range of $3.1 billion to $3.3 billion. The guidance includes the impact from the AT&T transaction and organic business revenue declines of 75 basis points. It excludes $400 million in transformation costs related to the multiyear target of lowering expenses by $1 billion through 2027. As a result, the first quarter is likely to have been impacted by declining legacy revenues and ongoing transformation costs.

From a financial standpoint, Lumen now has a significantly improved balance sheet. The company has reduced its total debt to less than $13 billion and lowered annual interest expense by approximately $500 million. The sale of the fiber-to-the-home business reduces annual capex by more than $1 billion, allowing Lumen to focus investment on enterprise and AI infrastructure.

Nonetheless, despite deleveraging, the debt is still massive. Further, as the company shifts toward newer growth products like fiber and cloud-based offerings, the secular headwinds in the legacy business will continue to prove a strain on the top-line expansion, at least in the near term.

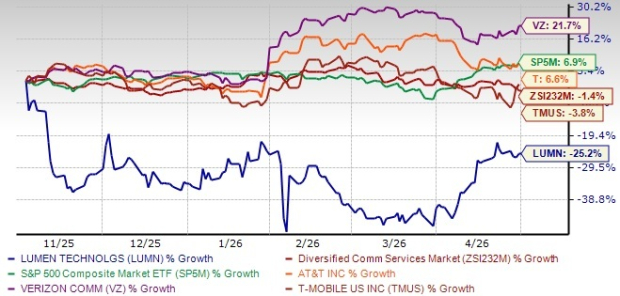

LUMN Stock Plunges

LUMN’s shares have lost 25.2% in the past six months. It has significantly underperformed the 1.4% decline of its Diversified Communication Services industry and the 6.9% gain of the Zacks S&P 500 composite.

Price Performance

Image Source: Zacks Investment Research

Lumen also underperformed some of its peers, such as Verizon Communications VZ, AT&T T and T-Mobile US, Inc. TMUS. Verizon and AT&T have registered a rise of 21.7%, and 6.6%, respectively, while T-Mobile is down 3.8% over the same time frame.

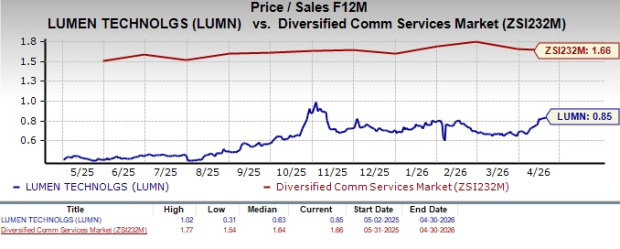

Key Valuation Metric for LUMN

From a valuation perspective, LUMN is trading at a massive discount. Going by its trailing 12-month price-to-sales ratio, it is trading at a multiple of 0.85X, much below the industry’s ratio of 1.66X.

Image Source: Zacks Investment Research

In comparison, Verizon, AT&T and T-Mobile are trading at multiples of 1.39, 1.4 and 2.25, respectively.

LUMN’s Investment Considerations

Lumen’s efforts at aligning itself with the massive growth of AI, cloud computing and digital telecom services show promise. Increasing PCF demand and deals with tech giants are creating a strong foundation for growth. Expansion into NaaS markets is an additional tailwind. Extensive cost cuts and discounted valuation make LUMN a compelling investment opportunity.

What to do With LUMN Stock Before Q1

The company’s AI-driven transformation, growing PCF pipeline and accelerating NaaS adoption continue to strengthen its long-term growth outlook. Combined with improving cost structure and discounted valuation, the risk-reward appears attractive for investors.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. Little-known AI firms tackling the world's biggest problems may be more lucrative in the coming months and years.

See Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

AT&T Inc. (T): Free Stock Analysis Report

Verizon Communications Inc. (VZ): Free Stock Analysis Report

T-Mobile US, Inc. (TMUS): Free Stock Analysis Report

Lumen Technologies, Inc. (LUMN): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).