SoFi Technologies (SOFI) stock has been under significant selling pressure for some time now. It has lost over 50% of its value from its 52-week high of $32.73. The latest decline followed the company’s Q1 earnings release, even though the financial technology company posted strong results.

In the first quarter, SoFi showed solid momentum. Members continued to grow, more products were adopted, and loan originations picked up, leading to an acceleration in its top-line growth rate. However, the market reacted negatively, sending shares down 15.4% on April 29.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Despite robust growth in key areas, SoFi’s forward guidance came below expectations. Moreover, management didn’t raise the full-year guidance, which was expected following a strong quarterly performance. Another concern was the slowdown in the company’s capital-light businesses.

Notably, SoFi stock benefitted from its revenue diversification initiatives and growing mix of capital-light, fee-based revenues, such as technology platform and financial services offerings. However, the technology platform saw revenue decline in Q1 due to the loss of a major client. Meanwhile, the company leaned more heavily on its lending business, which is more capital-intensive.

Although lending growth could help drive revenue in the near term, it’s generally seen as less attractive because it ties up more capital and can carry credit risk. Taken together, financial services and the technology platform generated over $500 million in Q1 revenue, up 24% year-over-year (YoY), making up just under half of total revenue. That’s a noticeable slowdown compared to Q4 2025, when those same segments brought in $579 million, grew 61% YoY, and accounted for 57% of total revenue.

Overall, Q1 marked an unfavorable shift in its revenue mix toward more capital-intensive lending, which weighed on its share price.

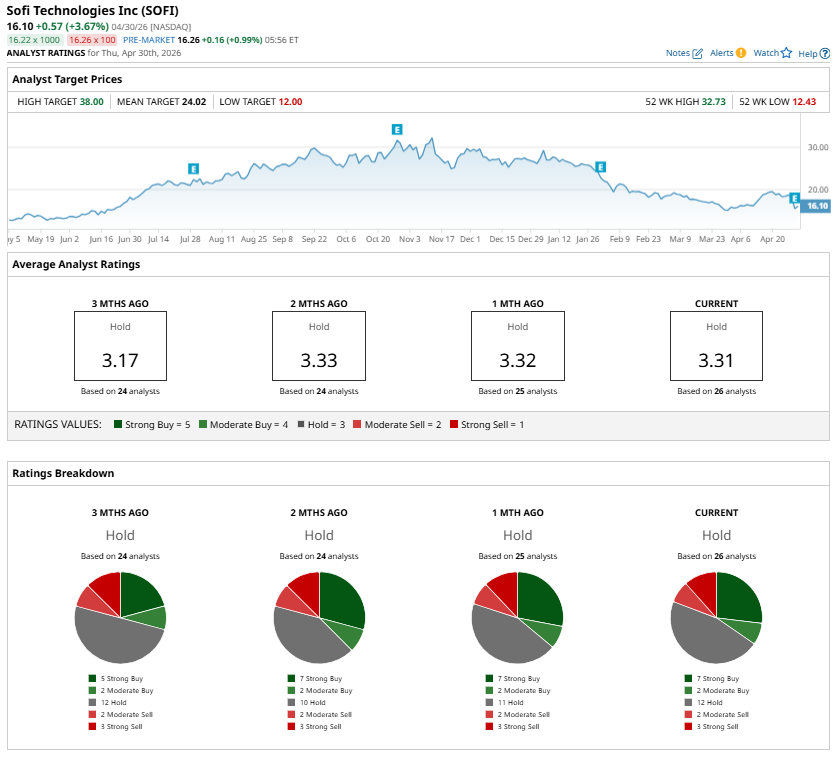

www.barchart.com

www.barchart.com What’s Ahead for SoFi?

SoFi appears positioned to maintain solid top-line momentum, driven by continued expansion in its member base and product adoption. Supporting its growth is the growing adoption of products from existing members. In the first quarter, 43% of new products were adopted by current members, up from 40% in the previous quarter. This is improving customer lifetime value.

Despite these favorable dynamics, SoFi’s revenue mix in 2026 is expected to tilt more heavily toward its capital-intensive lending segment. Management has guided for Technology Platform revenue of $325 million in 2026, down from $450.2 million in 2025. The contraction reflects the loss of a significant client. That said, the longer-term outlook remains constructive, supported by new partner onboarding and organic growth from existing clients, which should gradually rebuild scale.

At the same time, the Financial Services segment is expected to sustain momentum. Management expects at least 40% revenue growth in this division in 2026, following a strong first quarter where net revenue reached $429 million, up 41% YoY. Supporting the segment’s growth is the Loan Platform Business (LPB), a capital-light model that enables SoFi to originate loans for third parties, earn fees, and transfer credit risk off its balance sheet.

In the first quarter of 2026, total fee-based revenue rose 23% YoY to $386.8 million. Growth was driven by LPB activity alongside contributions from referral, brokerage, and interchange fees. Notably, LPB originations surged 90% YoY, reflecting the strong demand for the platform.

Meanwhile, the core lending business continues to expand at a robust pace. Management is targeting at least 30% growth in lending revenue for 2026, supported by healthy origination volumes across personal, student, and home loans. This strength reflects both favorable demand conditions and SoFi’s competitive positioning in the lending space.

However, the increasing reliance on lending introduces credit risk in the company’s revenue mix. While SoFi has made progress in diversifying toward fee-based and capital-light income streams, the anticipated 2026 skew toward lending could moderate investor enthusiasm. Lending-driven growth, while strong, is typically viewed as less resilient than platform or fee-based revenues and is capital-intensive. As a result, this mix shift may act as a constraint on valuation expansion in the near term.

Buy, Sell, or Hold SOFI Stock?

SoFi’s underlying fundamentals remain solid, with strong member growth, rising product adoption, and continued top-line expansion. However, a slowdown in higher-margin, capital-light raises concerns in the short term.

Over the long term, SoFi’s diversified revenue, improving customer lifetime value, and potential recovery in its technology platform support a constructive outlook. Because of this, long-term investors might see the recent dip as a buying opportunity. Those who already own the stock may also consider holding, especially since many of the current concerns appear to be already reflected in the price.

In the near term, however, gains could be limited due to ongoing credit risk exposure and a less favorable revenue mix.

www.barchart.com

www.barchart.com On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

A Short Squeeze Could Trigger in EZCORP Stock as It Trades at New 10-Year Highs SoFi Stock Is Down 50%. Should You Buy Now, Cut Your Losses, or Stay Put? As PayPal Plans to Make Venmo a Standalone Business Unit, Should You Buy, Sell, or Hold PYPL Stock? Dear Unity Software Stock Fans, Mark Your Calendars for May 7