Amazon (AMZN) is not just a retail giant anymore. It has become one of the biggest names in cloud computing and AI infrastructure, and that is where the real debate is now. Tech investors have spent the past few months trying to separate the AI winners from the AI spenders, and Amazon sits right in the middle of that conversation. On one side, it is pouring money into data centers and custom chips.

On the other hand, it says that spending is tied to long-term demand. That is why Andy Jassy’s latest remarks about Trainium matter so much. He said Amazon’s chip business could eventually generate $50 billion in annual revenue on its own. That is not a small side project. It could become one of the most important parts of the Amazon story.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Amazon has always had more than one engine. It sells goods, rents cloud capacity, runs ads and streaming services, and now builds its own silicon. That mix gives it more ways to grow than a pure retailer or a pure cloud company. It also makes Amazon harder to value, because the market has to price in everything from online shopping to AI chips.

Amazon Doubles Down on AI

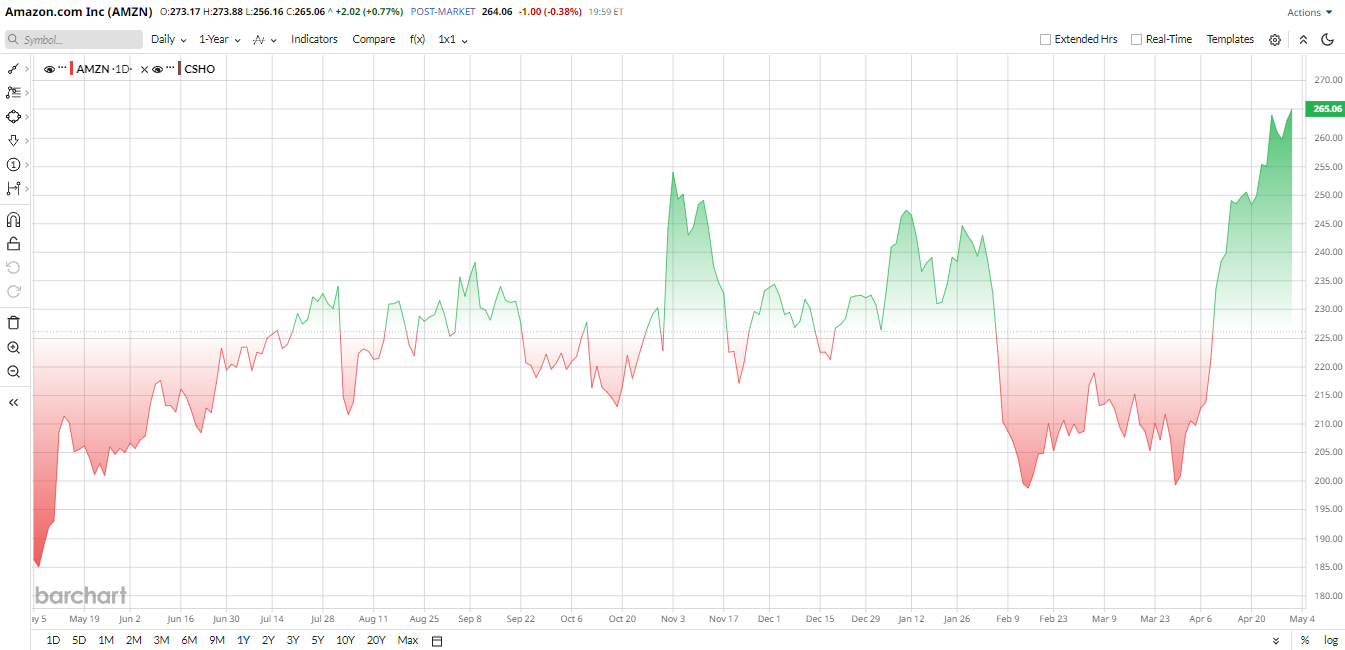

AMZN has had a strong 2026 so far. The stock is up about 16% this year and has gained roughly 41% over the past 12 months. Even so, investors have not been willing to give it a free pass. However, the shares slipped after the latest quarter despite earnings beating because the market is still uneasy about heavy capital spending, especially with Amazon keeping its 2026 AI investment target near $200 billion. That kind of spending can weigh on free cash flow in the short run, even when the long-term opportunity looks attractive.

The company is moving fast on AI. It added OpenAI models to Bedrock, expanded its custom chip rollout, and signed new AWS agreements with OpenAI, Anthropic, Meta (META), Nvidia (NVDA), and Uber (UBER). Amazon also said it secured a commitment from OpenAI for about two gigawatts of Trainium capacity and up to five gigawatts from Anthropic. That is a serious sign that Trainium is gaining traction outside Amazon’s own walls.

www.barchart.com

www.barchart.com Why Trainium Is Starting to Matter

The Trainium story is no longer just about internal efficiency. Amazon said its chips business has already reached a $20 billion run rate, and Jassy told investors it could soon grow into a $50 billion business if it stood alone. That is a huge number for a custom silicon effort. It suggests Amazon sees Trainium as more than a tool to save money on AWS. It may become a revenue line of its own.

Amazon is still seeing strong demand for AI infrastructure. The bigger takeaway is that Trainium could help Amazon capture more value from every AI workload running on AWS. If customers keep adopting it, Amazon may not need to rely as much on outside chip suppliers. That could improve margins over time and make AWS even stickier.

The Latest Quarter Still Showed Real Strength

Amazon’s March quarter was solid across the board. Revenue rose 17% year-over-year (YoY) to $181.5 billion, or 15% excluding foreign exchange effects. AWS was the standout again, with sales up 28% to $37.6 billion, while North America grew 12% to $104.1 billion and international revenue climbed 19% to $39.8 billion.

Operating income increased to $23.9 billion from $18.4 billion a year earlier. Net income jumped to $30.3 billion, or $2.78 per share, from $17.1 billion, or $1.59 per share. Amazon also said trailing 12-month operating cash flow rose 30% to $148.5 billion, but free cash flow fell to $1.2 billion because of much heavier investment in property and equipment, much of it tied to AI.

Jassy struck an upbeat tone on the call. He said AWS grew 28%, the chips business topped a $20 billion revenue run rate, and advertising passed $70 billion in trailing 12-month revenue. He also said the company is making customer lives easier across its businesses, which is the kind of message investors like to hear when the spending bill looks so large.

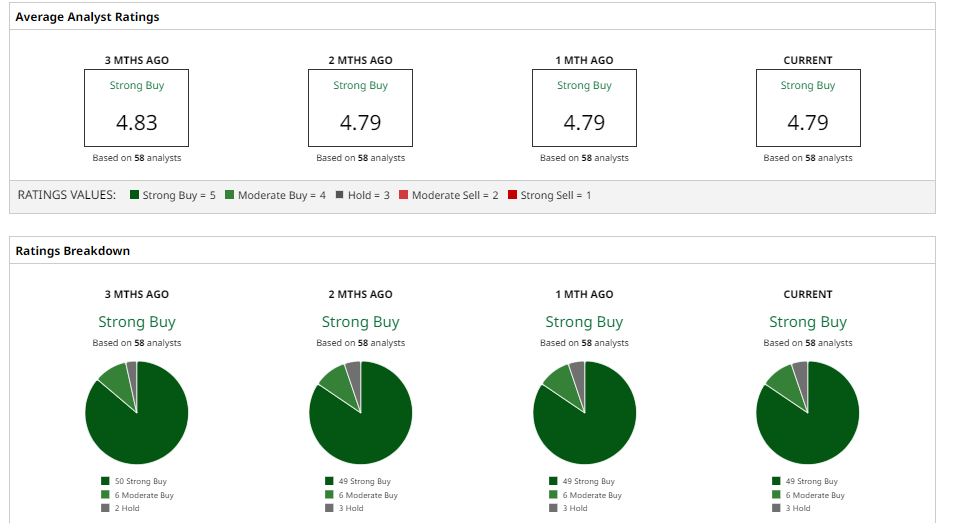

What Wall Street Thinks of AMZN Stock

Analysts still look constructive on AMZN stock. Morgan Stanley just lifted its target to $330 and kept an “Overweight” rating.

Likewise, Bank of America bumped its target to $310, pointing to AWS upside without a matching increase in capex guidance.

Also, RBC Capital moved to $320 and said Trainium’s growing commitment base supports the AI case.

Overall, AMZN is still a consensus “Strong Buy” on Wall Street with an average price target of $290.57, which implies more than 8% upside.

That leaves Amazon in a familiar spot. The stock is not cheap, and the spending is real. But if Trainium keeps scaling the way Jassy suggests, the market may look back on this quarter as the moment Amazon’s AI chip business stopped being a footnote and started becoming a major growth driver.

www.barchart.com

www.barchart.com On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Wolfspeed Just Announced New Executives. Does That Make WOLF Stock a Buy, Sell, or Hold? Hertz Stock Is Soaring After Expanding an Autonomous Vehicle Partnership with Uber. A Short Squeeze Could Take It Even Higher. Compute Spending Just Broke the Dot-Com Record High. Here’s the Safe Way to Invest in AI Now…. Just in Case. Silicon Motion Stock Popped More Than 40% in a Single Day. Investors Are Still Ravenous for Storage Amid the AI Rally.