Software giant Salesforce (CRM) is hitting turbulence on Wall Street as sentiment toward the broader software sector weakens. Investor anxiety has intensified, particularly after artificial intelligence (AI) startup Anthropic introduced its Claude Cowork plugins earlier this year, fueling concerns that AI agents could begin replacing, rather than simply enhancing, traditional SaaS platforms.

The stock has already taken a significant hit this year, but Salesforce is pushing back against the narrative by doubling down on its AI ambitions. On May 1, investor sentiment showed signs of improvement, with the stock climbing over 4% after the company announced plans to revamp its revenue reporting from fiscal 2027 onward, aligning it more closely with its “Agentic Enterprise” strategy. Under the new structure, revenue will be divided into two core segments: “Agentforce Apps” and “Data 360, Platform & Other.”

More Yield, Less Trap: Sign up free to get Barchart’s daily Dividend Investor newsletter straight to your inbox.

Key offerings such as Sales, Slack, MuleSoft, and Tableau will be reorganized into broader AI-driven categories, while revenue from major acquisitions like Informatica will be reported separately for one year post-closing. With this new reporting structure shift signaling a sharper AI focus, Salesforce is clearly repositioning itself for the next phase of enterprise software. Given this new development, here’s a closer look at CRM stock.

About Salesforce Stock

Based in San Francisco, Salesforce is widely recognized as the global leader in customer relationship management (CRM), helping businesses build and manage stronger customer connections. Founded in 1999, the company played a key role in pioneering cloud-based software and continues to evolve as enterprises shift toward an AI-driven era of digital transformation.

A major pillar of this evolution is Agentforce, Salesforce’s flagship AI initiative, which introduces autonomous AI agents capable of handling tasks for both employees and customers. By unifying data across an organization, Salesforce enables a complete 360-degree view of each customer. Its broad suite of solutions, spanning sales, service, marketing, commerce, and IT, helps businesses operate more efficiently while staying aligned across teams.

Together, these offerings underscore Salesforce’s move toward a more intelligent and streamlined approach to customer management in a rapidly changing digital landscape. Its ecosystem also features widely used platforms like Slack, Tableau, and MuleSoft. The company’s market capitalization currently stands at around $150.4 billion.

While Salesforce has seen a modest bounce following its reporting overhaul, the broader trend paints a far harsher reality. The stock has plunged 32.18% over the past year and is down another 29.57% so far in 2026, an underperformance that’s hard to ignore, especially compared to the broader S&P 500 Index ($SPX), which has surged 26.8% over the past 52 weeks and gained an additional 5.33% year-to-date (YTD).

www.barchart.com

www.barchart.com After a steep pullback, Salesforce’s valuation has cooled significantly, with the stock now trading at just 18.2 times forward earnings, well below the sector median of 23.9 times and sharply discounted from its own five-year average of 33.3 times, signaling a notable reset in expectations.

Salesforce’s Fundamentals Remain Strong

Even as investors rotate out of software names, Salesforce continues to show resilient underlying momentum. In its fiscal 2026 fourth-quarter results, released on Feb. 25, the company delivered a clear beat on both revenue and earnings. Revenue came in at $11.20 billion, up 12.1% year-over-year (YOY), its fastest growth in two years, and slightly above the $11.17 billion consensus estimate.

That growth was fueled in part by the successful integration of Informatica, along with a solid 13% rise in subscription and support revenue. Forward-looking indicators also reinforced the strength of demand. Current remaining performance obligation (cRPO), a key measure of contracted revenue yet to be recognized, jumped almost 16% YOY to $35.1 billion, pointing to strong visibility ahead.

Profitability was another standout. Adjusted EPS surged a notable 37.1% to $3.81, comfortably beating expectations of $3.03 per share. And, Salesforce returned a significant $14.3 billion to shareholders during the period, including $12.7 billion through share repurchases and $1.6 billion in dividends. A major highlight was Agentforce, the company’s autonomous AI platform, which is rapidly gaining traction.

In the earnings release, CEO Marc Benioff described Salesforce as evolving into the “operating system for the Agentic Enterprise.” Agentforce’s annual recurring revenue (ARR) climbed to $800 million, marking an impressive 169% YOY increase. Engagement levels were equally strong, with over 2.4 billion “Agentic Work Units” delivered and 19 trillion tokens processed. Notably, adoption is deepening within the existing customer base, with 60% of bookings for Agentforce and Data 360 coming from expansions.

Looking ahead, Salesforce struck a cautiously optimistic tone. For the first quarter of fiscal 2027, it expects revenue between $11.03 billion and $11.08 billion, with adjusted EPS in the range of $3.11 to $3.13. Additionally, the company reaffirmed its long-term ambitions, raising its fiscal 2030 revenue target to $63 billion, underscoring confidence in its AI-led growth trajectory.

What Do Analysts Think About Salesforce Stock?

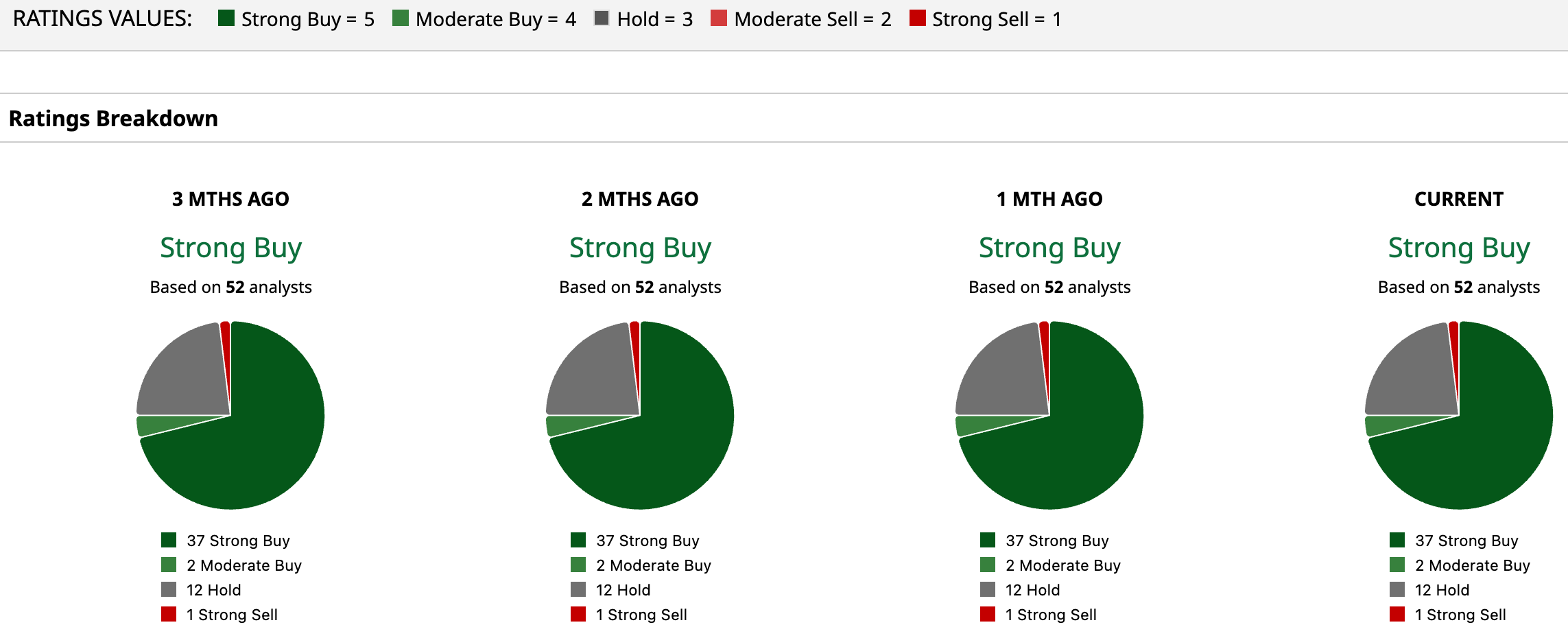

Even after a bruising pullback so far in 2026, Wall Street is still firmly in Salesforce’s corner. The company currently holds a consensus “Strong Buy” rating, with conviction skewed heavily bullish; 37 of 52 analysts rate it a “Strong Buy,” two lean “Moderate Buy,” 12 stay cautious with “Hold,” and only one remains outright bearish with a “Strong Sell.”

The upside narrative is just as compelling. The average price target of $276.43 points to a potential gain of 48.6% from current levels, while the most optimistic forecast on the Street, $475, suggests the stock could surge as much as 155.3%, a clear signal that many analysts still see a powerful rebound story ahead.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com On the date of publication, Anushka Mukherji did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

CRM Stock Jumps as Salesforce Makes Clear It’s an AI Agent Company Now More AI Is Coming to iOS 27. Why That Could Make Apple Stock a Buy Here. Seagate and Western Digital Are a Hard Disk Drive Duopoly. Barchart Ranks the Storage Stocks Here. McDonald’s Is Down 4% and Starbucks Is Up 25% in 2026. The Better Dividend Stock Might Surprise You.