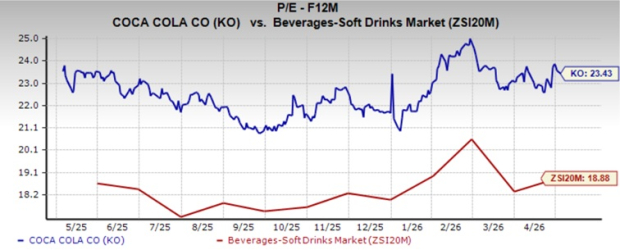

The Coca-Cola Company KO has experienced a steady increase in its share price in recent months, driving its valuation to elevated levels. However, its price-to-earnings (P/E) multiple of 23.43X is above the Zacks Beverages – Soft Drinks industry average of 18.88X and the S&P 500’s average of 21.98X. This valuation premium raises investor concerns about the stock’s valuation.

Additionally, the company’s forward 12-month price-to-sales (P/S) ratio of 6.8X is below the industry average of 5.21X.

Image Source: Zacks Investment Research

KO Overvalued vs. Peers

At 23.43X times P/E, Coca-Cola trades at a significantly higher valuation than its competitors, such as PepsiCo Inc. PEP, Keurig Dr Pepper, Inc. KDP and Primo Brands Corporation PRMB, which are delivering solid growth and trade at lower multiples. PepsiCo, Keurig Dr Pepper and Primo Brands have forward 12-month P/E ratios of 17.54X, 12.16X and 13.95X, all significantly lower than Coca-Cola.

In the year-to-date period, Coca-Cola’s shares have gained 11.8% compared with the broader industry and the Zacks Consumer Staples sector’s growth of 9.4% and 5.5%, respectively. The company has also outperformed the S&P 500’s rise of 6.4%.

KO’s performance is stronger than that of its key competitor, PepsiCo and Keurig Dr Pepper, which have risen 7.8% and 3.1%, respectively, year to date. Meanwhile, the KO stock has underperformed Primo Brands’ growth of 22.9%.

Coca-Cola’s YTD Stock Return

Image Source: Zacks Investment Research

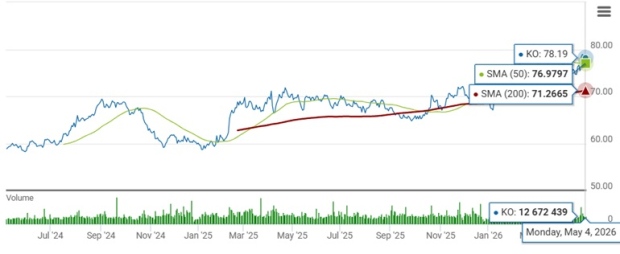

KO’s current share price of $78.19 is 4.6% below its recent 52-week high mark of $82. Also, the stock trades 19.6% above its 52-week low of $65.35. Coca-Cola trades below its 50-day moving average, indicating a bearish sentiment. The stock moves above the 50 and 200-day moving averages, suggesting a long-term potential.

KO Stock Trades Below 50 & 500-Day Moving Averages

Image Source: Zacks Investment Research

Factors Supporting KO’s Recent Momentum

Coca-Cola’s recent stock momentum is underpinned by a combination of strong operational execution and resilient demand. In first-quarter 2026, the company delivered 3% volume growth across all segments and extended its streak of value share gains to 20 consecutive quarters, highlighting consistent market outperformance. This broad-based growth was supported by a powerful brand portfolio, with key products like Coca-Cola, Fanta and Powerade driving volume gains globally.

Innovation and marketing have also played a pivotal role. Product launches and localized campaigns, such as cherry-flavored variants and global sports partnerships, have strengthened consumer engagement and boosted sales. Additionally, Coca-Cola’s focus on affordability and revenue growth management has helped maintain demand across income segments, particularly amid macroeconomic pressures.

The company continues to benefit from its scale and distribution network, adding more than 600,000 outlets and expanding cold drink equipment placements to drive impulse purchases. Margin expansion, supported by cost efficiencies and disciplined execution, contributed to double-digit EPS growth. Combined with strong cash flow generation and a balanced growth strategy between volume and pricing, these factors collectively reinforce investor confidence and support Coca-Cola’s upward stock momentum.

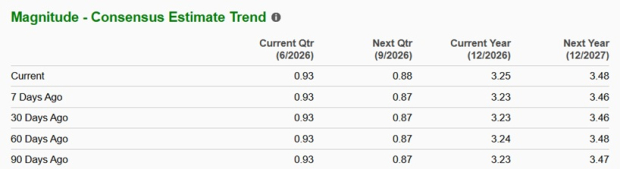

Coca-Cola’s Estimate Revision Trend

The Zacks Consensus Estimate for Coca-Cola’s 2026 and 2027 EPS inched up 0.6% each in the past seven days. The upward revision in earnings estimates indicates that analysts are gaining confidence in the company’s growth potential.

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for KO’s 2026 sales and EPS suggests year-over-year growth of 2.5% and 8.3%, respectively. For 2027, the Zacks Consensus Estimate for PepsiCo’s sales and EPS implies 2.5% and 7.1% year-over-year growth, respectively.

Are There Risks Attached to KO’s Growth Story?

Despite Coca-Cola’s strong momentum, several risks could challenge its growth trajectory. The company continues to operate in a “complex external environment,” with inflation, macroeconomic uncertainty, and geopolitical tensions, particularly in the Middle East, creating volatility across key markets. These factors have already impacted demand in certain regions, such as volume declines in March within Eurasia and the Middle East.

Cost pressures also remain concerning. Commodity inflation in inputs like tea and coffee, along with potential supply disruptions affecting packaging materials, could weigh on margins, even if management currently views these pressures as manageable. Additionally, Coca-Cola’s increasing focus on affordability to support lower-income consumers may limit pricing power and create mix headwinds.

Finally, regional imbalances, such as weaker price/mix in the Asia Pacific and geopolitical or tax-related challenges in markets like Mexico, could affect consistency. While Coca-Cola’s scale and strategy provide resilience, execution risks and external uncertainties remain key watchpoints.

Coca-Cola’s Investment Rationale

KO exhibits a balanced risk-reward profile at the current levels, supported by strong brand equity, consistent execution and resilient demand trends. The company’s ability to drive volume growth, expand margins and innovate across markets underpins its long-term growth outlook.

However, its premium valuation relative to peers limits near-term upside and leaves the stock vulnerable to macroeconomic or execution-related setbacks. Ongoing cost pressures, geopolitical uncertainties and pricing constraints could weigh on its performance. While Coca-Cola remains a fundamentally strong and defensive play, investors may prefer to wait for a more attractive entry point or clearer margin expansion visibility before increasing exposure.

PepsiCo currently has a Zacks Rank #2 (Buy). You can see the complete list of today's Zacks #1 Rank (Strong Buy) stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

CocaCola Company (The) (KO): Free Stock Analysis Report

PepsiCo, Inc. (PEP): Free Stock Analysis Report

Keurig Dr Pepper, Inc (KDP): Free Stock Analysis Report

Primo Brands Corporation (PRMB): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).