Few stocks have had a year like Intel (INTC). Shares of the chipmaker have nearly tripled in 2026, and the rally has caught the White House's attention. President Donald Trump is publicly taking a victory lap, and now Wall Street is asking the same question that investors are sitting with: Is there still time to get in?

The answer depends on how you look at what Intel is building — and what its first-quarter results revealed about the road ahead. Let's take a closer look.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

www.barchart.com

www.barchart.com Trump's Intel Bet Is Paying Off

The U.S. government made an unusual move last summer when it acquired a 10% stake in Intel by purchasing 433.3 million shares at $20.47 per share for roughly $8.9 billion. The funding came from two sources: $5.7 billion from the CHIPS and Science Act and $3.2 billion from secure semiconductor programs.

On Truth Social, Trump credited himself for the windfall. "I am responsible for making the United States of America over [$30 billion] in the last 90 days on that stock alone," wrote Trump.

With INTC stock recently closing near $108, the government's position has swelled to more than $46 billion. That is an unrealized gain of more than $35 billion on paper.

Q1 Results Show a Business in Transition

In Q1 2026, Intel reported revenue of $13.6 billion, up 7% year-over-year (YOY). Adjusted EPS stood at $0.29, coming in above consensus estimates of $0.01 and rising 123% YOY.

Intel reported non-GAAP gross margins of 41%, beating guidance by 650 basis points. The chip giant has now beaten financial estimates for six consecutive quarters, helping raise the INTC stock price by more than 430% in the past year.

CEO Lip-Bu Tan made one thing clear on the earnings call: demand is outpacing supply across business segments. "A year ago the conversation around Intel was about whether we could survive," said Tan. "Today it's about how quickly we can add manufacturing capacity."

Intel Widens Its AI Moat

For the past few years, the AI trade has been entirely about graphics processing units (GPUs) and the companies building them.

Tan explained on the call that, as AI moves from training to inference and into agentic workloads, the role of the CPU is growing. The ratio of CPUs to GPUs in AI deployments used to be roughly 1:8, but now the ratio is moving toward 1:4 — and potentially closer to parity as multi-agent AI systems expand.

Intel's data center and AI (DCAI) revenue segment grew 22% YOY in Q1. Xeon server CPU demand is described as "strong and sustained" with momentum expected to carry into 2027. The company has also recently signed a multiyear agreement with Alphabet's (GOOGL) Google to supply Xeon processors.

CFO David Zinsner said that demand is so strong that Intel is undershipping the market by a meaningful amount. When pressed for a specific figure on how much revenue the supply constraints are costing, his answer was short: "It starts with a ‘B.’"

Is INTC Stock Still a Good Buy?

The Intel 18A manufacturing node is still in its early ramp and is currently a headwind to margins. Input costs — including memory, substrates, and T-glass — are rising, and the company is guiding Q2 gross margins at 39%, slightly below Q1.

At the same time, Intel 18A yields are tracking ahead of internal targets. Intel 14A, the next-generation process node, is showing solid early results. The company is also deepening its partnerships with SpaceX, xAI, and Tesla (TSLA) through the Terafab project, exploring new ways to improve the economics of semiconductor manufacturing.

For investors still on the sidelines, the question is whether the transformation is already priced in or whether this is still the early innings of a longer comeback.

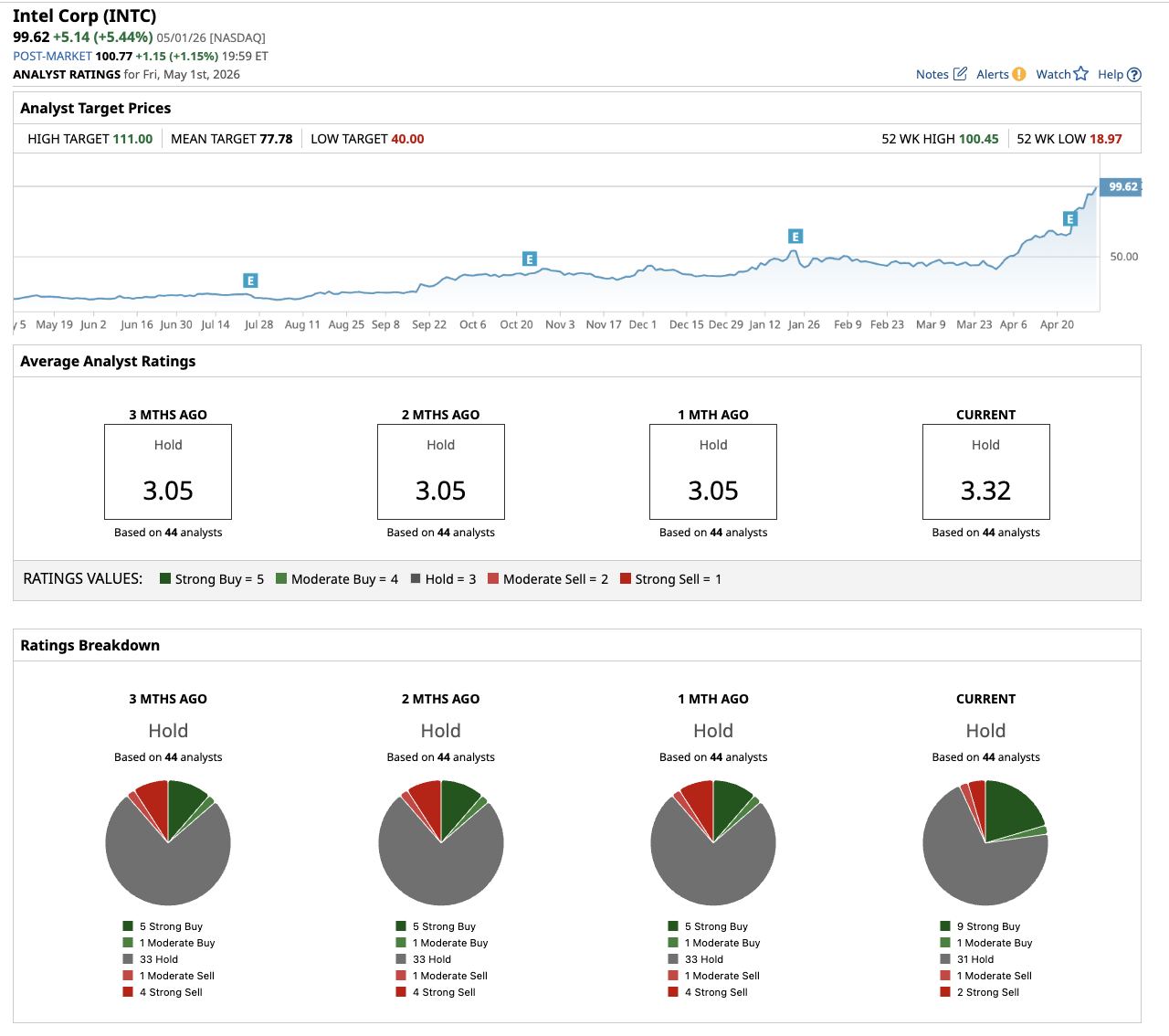

Out of the 44 analysts covering INTC stock, nine recommend a “Strong Buy”, one recommends a “Moderate Buy” rating, 31 recommend a “Hold” rating, one analyst recommends a “Moderate Sell,” and two recommend a “Strong Sell” rating. The average price target of $79.19 suggests potential downside of 27% from current levels. Meanwhile, the high price target of $118 implies shares could climb 9% from here.

www.barchart.com

www.barchart.com On the date of publication, Aditya Raghunath did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Intel Stock Is Up 190% in 2026 and Trump Says the U.S. Has Made $30 Billion. The Early Innings for INTC May Be Over. 10% Layoffs Won’t Be the End as Zuckerberg Says AI Will Drive More Job Cuts Later This Year So Much for the Software Apocalypse: Atlassian Stock Surges as Data Center Revenue Grows 44% ‘It Has Ticked Off Literally Everybody in the Lending World’: Why Billionaire Steve Eisman Is Shorting This Software Stock