With artificial intelligence (AI) giants repeatedly making history — and investors ready to buy their shares for any price — a real drama is unfolding in the market. At the center of attention lies Super Micro Computer (SMCI), one of the key manufacturers of server racks and liquid cooling systems for data centers.

Super Micro represents a story of two sides. On one hand, the company has a phenomenal business case as the AI revolution surges. But from another perspective, the firm looks as if it's standing on the edge of turmoil. Accordingly, investors have to ask themselves what exactly is the case with SMCI stock: Is Super Micro a fundamentally strong business experiencing a temporary storm? Or has the company overplayed itself in a very dangerous game? Let's take a closer look.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Super Micro's Financials

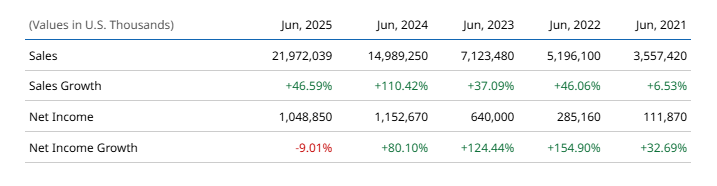

Looking exclusively at revenue and the market valuation of Super Micro, investors may ask themselves why they've waited to invest in SMCI stock. Super Micro produces the physical foundation for AI by making server racks. Amid the global data-center buildout, the firm's revenue has demonstrated massive growth, climbing from annaul sales of $7.1 billion in June 2023 to $21.9 billion in June 2025.

www.barchart.com

www.barchart.com However, net income tells a more complex story. While net profit climbed from $640 million in June 2023 to $1.15 bliion in June 2024, it then decreased to $1.04 billion in June 2025. Why has net income fallen amid such strong revenue growth? The answer lies in Super Micro's aggressive strategy to capture the market.

A Fundamental Boom and the Malaysia Gambit

Over the past few years, Super Micro has pursued the construction of huge new capacities, including an advanced factory in Malaysia. To load its facilities with orders and not allow downtime, management also took a conscious step by engaging in harsh price decreases. Super Micro sacrificed current margin to take away clients from competitors like Dell Technologies (DELL).

This strategy seems to have worked so far. Super Micro's factory in Malaysia has reached full capacity, for example, and the company has more clients and a larger share of the market. What's more, accounting for the fact that production costs in Asia are significantly lower than the United States, Super Micro has levers to begin recovering its margin on strong factory volumes.

Super Micro's Attractive Valuation

In the background of this strategic victory, the market valuation of Super Micro looks great — perhaps absurdly. Shares of SMCI stock currently trade near $32, and the market capitalization sits at $16.7 billion. The most revealing multiple is the firm's forward price-to-earnings (P/E) ratio, which now comes in at just 14.6 times.

www.barchart.com

www.barchart.com For comparison, other tech companies with similar paces of growth trade at P/E ratios of 30 times, 40 times, or even 50 times. Super Micro's much lower P/E ratio is typically more characteristic of a stagnating manufacturer of toothpaste, not a leader in AI infrastructure.

From the perspective of dry digits and business logic, SMCI stock's valuation looks like a real gift. But the market rarely errs so simply. When a stock trades for so cheap, it can mean there's very large skeleton in the company's closet.

Super Micro Faces a Legal Mess

The problem with Super Micro hides not in its balance sheet or its factories. Rather, Super Micro Computer seems to be facing a legal mess.

Issues first arose when, with an investigation from short seller Hindenburg Research in the background, prestigious auditor Ernst & Young severed ties with Super Micro in 2024. The company later found a replacement public accounting firm in BDO USA, and the situation seemed to stabilize. So, the logic at the beginning of 2026 was simple: If BDO USA did not find fatal problems to report after a year, that would mean the potential issue was resolved, right?

However, in March 2026, a much scarier skeleton fell out of Super Micro's closet: a U.S. Department of Justice investigation over the alleged violation of harsh export controls. The DOJ suspects that three people associated with the company smuggled high-tech servers and sanctioned chips to China, bypassing U.S. bans. Preliminary estimates suggest volumes up to $2.5 billion.

These suspected violations have crossed out a lot of positives for Super Micro. After all, an investigation from the DOJ is not a simple fine. In the worst-case scenario, this threatens the recall of export licenses, the blocking of accounts, and even the company potentially landing on a government blacklist. For a global manufacturer of AI hardware, that could practically be a death sentence for the business.

The market fears legal uncertainty. For potential SMCI stock investors, what difference does it make how cheap the P/E is or how many racks the company produces if tomorrow the firm faces huge consequences from the U.S. government?

The Advantage of Technological Stickiness

At first glance, after news of the DOJ investigation, clients were obliged to panic and run from Super Micro to competitors. But in the world of high-tech data centers, everything is more complex. A powerful factor is at play for Super Micro in the form of technological “stickiness.”

When a tech giant builds a data center, it purchases thousands of server racks. But the primary contract is only the beginning. A company's personnel learns to service their specific infrastructure while logistics and software sharpen under it. On top of that, in liquid cooling systems — which are currently a main driver of the market due to the colossal heat emissions of chips — different manufacturers use different connectors and standards, meaning Super Micro's systems can be incompatible with those of competitors.

With that in mind, if a company began to build a data center using Super Micro's architecture, any transition to another vendor could cost astronomical sums and lead to critical delays. Clients already "sat down" on Super Micro's ecosystem. Technological dependence is so high that firms are unlikely to refuse deliveries simply because of reputational risks.

Still, the loyalty of the richest corporations of the world is powerless before the government. If the DOJ decides to halt Super Micro's export operations or freeze contracts with chip manufacturers, this technological stickiness may not save the company.

A Balance of Risk and Reward

Super Micro Computer is a textbook example of the risk-reward dilemma. From one side, the combination of Super Micro's financials and valuation is promising. Revenue continues to fly high, the Malaysia facility is working like clockwork, and margin recovery seems to be in store. That makes SMCI stock look primed to grow.

However, a sword still hangs over Super Micro — and the problem is that legal risks are not cured by good financial reports. The DOJ investigation could result in severe consequences for the company.

Which way is the balance tilted right now? The honest answer is that it's hard to say. With too many unknown variables, the answer is inaccessible to a rank investor.

The Bottom Line on SMCI Stock

The current valuation does perhaps say one thing about SMCI stock: the market seems to have already priced a deep crisis into shares. Fear is calling the shots, and SMCI is being valued as if the die has already been cast.

For conservative investors who like calm and predictable dividends, Super Micro looks like a toxic asset right now. But for investors with the stomach for massive risk, SMCI stock may represent a historical chance. To buy shares of an AI infrastructure company at the price of a stagnating retailer could be rare luck. If the worst-case scenario with the DOJ is not realized, and the company gets off with a conditional fine, the spring of tension will uncompress with incredible force.

High profitability always goes hand in hand with high risk. In the case of Super Micro, both of these scales are cranked up to the maximum. Whether you are ready to play this risky game is only up to you.

On the date of publication, Mikhail Fedorov did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

After an Earnings Blowout, Morgan Stanley Just Raised This Chip Stock’s Target Price by $8 You Must Decide for Yourself If Super Micro Computer Stock Is Toxic or a Tantalizing Buy Here as Legal Drama Swirls Palantir’s Record Revenue Signals Strength — Ignore Overvaluation Fears for PLTR Stock Super Micro Computer Soars on Earnings Beat. Here's What Comes Next for SMCI Stock.