Peloton (PTON) stock is up 54% from its 2026 lows hit in mid-March amid the U.S.-Iran war. Like many other former pandemic-era darlings such as Zoom Video Communications (ZM) and DocuSign (DOCU), it has been trying to adjust to the post-Covid world and is working on a turnaround.

The stay-at-home fitness industry has been on shaky ground ever since gyms reopened after the Covid-19 pandemic. Peloton’s subscription base and revenues have been falling as consumers shifted back to gyms. In the fiscal Q3 2026, it reported revenues of $631 million, which, for context, is almost exactly half the amount it generated in the corresponding quarter in the fiscal year 2021.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

www.barchart.com

www.barchart.comMeanwhile, there was a silver lining in Peloton’s fiscal Q3 earnings, which were released yesterday, May 8, as it reported a 1% year-over-year (YOY) rise in revenues. Importantly, the key driver of better-than-expected revenues was the Product segment, which reported only 1% fall in revenues. While the segment’s revenues still fell YOY, there are signs of stabilization following much steeper declines in the previous quarters. Notably, following the fiscal Q3 earnings release, Peloton updated its annual outlook, which calls for only 2% YOY decline in revenues at the midpoint.

Peloton Expects to Post an Annual Profit This Year

While Peloton is no longer the kind of growth story it was during the pandemic, the company has started focusing on profitability. It has been on a cost-cutting spree, and apart from layoffs, it has rationalized its store footprint by shutting down some stores. However, it is investing in smaller micro stores, which it said are much more productive than legacy stores on a sales per square foot basis.

It has also been expanding its target market and is working towards becoming a wellness partner for its members, offering classes for mental well-being, sleep, and nutrition. The company is now selling its hardware to gyms, and the segment saw a 14% annual increase in revenues in the most recent quarter. Peloton also entered the secondhand market, and in the March quarter, over half of its gross customer adds came from sales of used equipment.

The turnaround actions are having a visible impact on Peloton’s earnings, and it expects to post positive operating income and net profit in the fiscal year 2026. It would be the first time that the company would hit the milestone, which is no mean feat considering the kind of losses and cash burn it was previously witnessing.

Peloton Has A Much Stronger Balance Sheet Now

Peloton’s balance sheet is in a much better shape now, and its net debt fell 70% to $173 million at the end of March. Notably, Peloton has been posting healthy free cash flows and expects to generate around $350 million of free cash flows in the current fiscal year.

The company plans to initiate the process of credit rating following the hire of a permanent CFO. Having a credit rating would help Peloton lower its cost of funds, especially in light of the company’s much-improved financial health.

Another issue that Peloton had been battling was the massive share-based compensation, which reached $300 million in the fiscal year 2024. However, the company has addressed the issue and expects share-based compensation to be near $200 million in this fiscal year. While that number is still high considering the Peloton's market cap of around $2.4 billion, it is trending in the right direction, and the management expects this number to fall further in the coming years.

Should You Buy Peloton Stock?

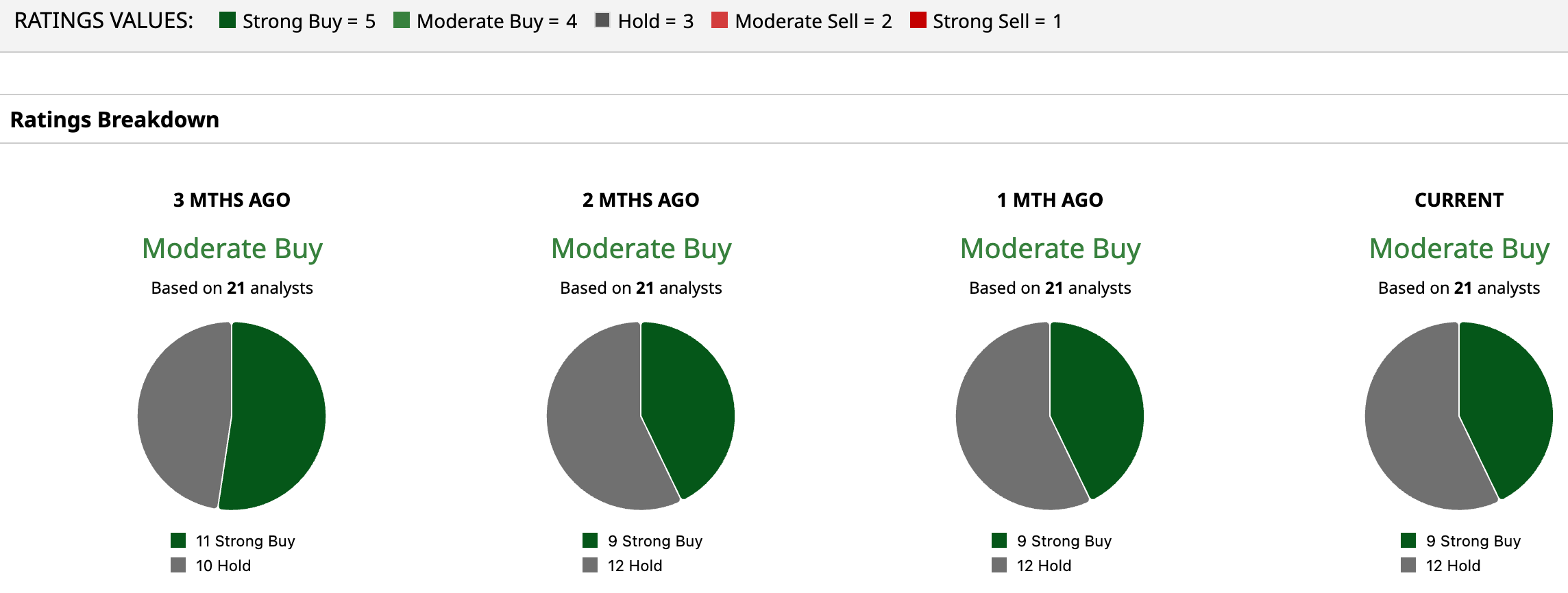

Peloton has a consensus rating of “Moderate Buy” from the 21 analysts polled, while its mean target price of $8.19 is over 44% higher than current price levels.

www.barchart.com

www.barchart.com www.barchart.com

www.barchart.comPTON trades at a forward price-to-earnings (P/E) multiple of 38.52 times. While the valuations would appear on the higher side considering its negative top-line growth, the number should be seen in perspective. Peloton’s profits should increase considerably in the coming years as its turnaround action pays off. Moreover, Peloton can command premium valuations, considering that the bulk of its revenues now come from subscriptions rather than product sales. Overall, I remain invested in PTON and see the stock going higher from these levels.

On the date of publication, Mohit Oberoi had a position in: PTON . All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

This Turnaround Stock Is Up 54% From the 2026 Lows. I See More Growth Ahead. PayPal Faces a Brutal Reality: 3 Real Problems Hurting the Stock Now Solar ETFs Are Shockingly Cheap Now. Politics Will Decide If They’ll Burn You to a Crisp. Google Stock Could Rally as the Company Builds OpenClaw Competitor Remy. How to Play GOOGL Here.