Callaway Golf Company CALY appears to be building a stronger long-term growth story around its golf ball business, with management highlighting steady market-share gains, improving profitability and growing consumer demand during the first-quarter 2026 earnings call.

The company’s latest Chrome Tour lineup has emerged as a key growth driver. Management noted that customer reception has been strong, helping Callaway expand its presence in the premium golf ball category. At the same time, the Supersoft franchise continues to perform well, giving the company momentum across multiple price points.

A major highlight was Callaway’s growing share in the green grass channel, which has become its largest and most strategic distribution platform. The company’s U.S. golf ball market share at green grass locations reached a record 23.9% in March, rising 350 basis points year over year. Management credited this performance to years of investment in product quality, manufacturing capabilities and distribution expansion.

Callaway also believes its golf ball manufacturing operations are now operating at world-class efficiency levels. This is important because higher production efficiency can support margin expansion even amid ongoing tariff and raw material cost pressures. The company already delivered a 260-basis-point improvement in gross margin during the quarter despite elevated tariffs.

Beyond golf balls, healthy demand for the new Quantum club lineup and strong growth at TravisMathew are supporting overall momentum. Management raised full-year revenue and EBITDA guidance, reflecting confidence in consumer demand and the resilience of the golf market.

With increasing market share, stronger profitability and continued innovation, Callaway’s golf ball business could remain an important engine of sustainable long-term growth.

CALY’s Price Performance, Valuation & Estimates

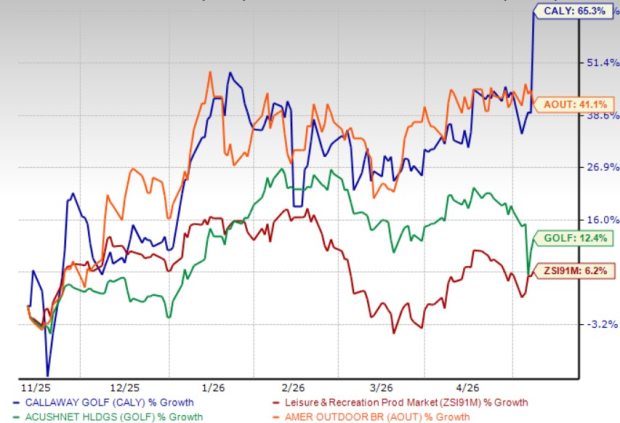

Shares of CALY have gained 65.3% in the past six months compared with the industry’s increase of 6.2%. In the same time frame, shares of other companies like Acushnet Holdings Corp. GOLF and American Outdoor Brands, Inc. AOUT have gained 12.4% and 41.1%, respectively.

Price Performance

Image Source: Zacks Investment Research

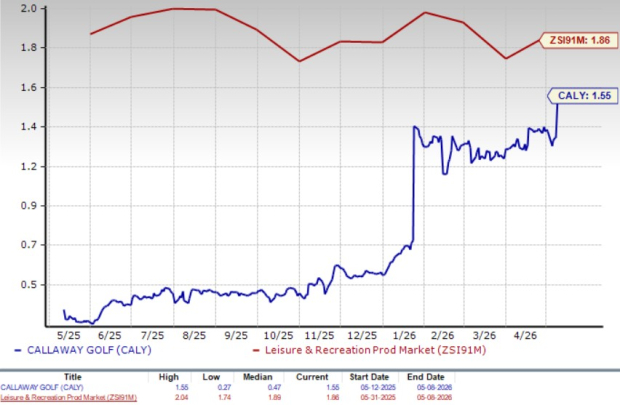

CALY is currently trading at a discount compared with the industry, with a forward 12-month price-to-sales ratio of 1.55. Acushnet Holdings and American Outdoor are trading at P/S of 0.48X and 1.85X, respectively.

P/S (F12M)

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for CALY’s 2026 earnings has increased in the past seven days.

Image Source: Zacks Investment Research

CALY currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

See Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Acushnet (GOLF): Free Stock Analysis Report

American Outdoor Brands, Inc. (AOUT): Free Stock Analysis Report

Callaway Golf Company (CALY): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).