The Cigna Group CI is well poised for growth on the back of strong segmental performance, improving operating efficiency and shareholder-friendly moves. Based in Bloomfield, CT, Cigna has a market capitalization of $79.6 billion. The company’s shares have gained 7.2% year to date, underperforming the industry’s average increase of 20.1% over the same period.

Its forward P/E ratio of 9.35x is lower than the industry average of 17.72x, indicating a relatively attractive valuation. Supported by solid prospects, Cigna currently holds a Zacks Rank #3 (Hold) and has a Value Score of A.

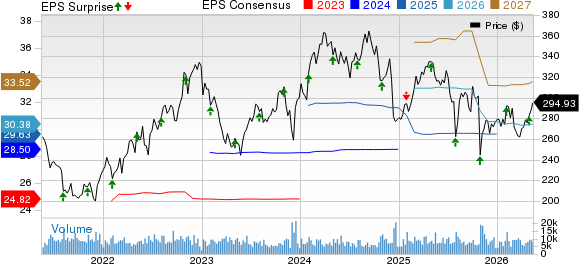

Zacks Estimates for CI

The Zacks Consensus Estimate for 2026 earnings is pegged at $30.38 per share, suggesting a 1.8% year-over-year increase. Over the past month, estimates have witnessed seven upward revisions against one downward revision. The consensus estimate for 2026 revenues is pinned at $287.5 billion, indicating 4.7% year-over-year growth.

Cigna beat earnings estimates in each of the trailing four quarters, with the average surprise being 1.9%.

Cigna Group Price, Consensus and EPS Surprise

Cigna Group price-consensus-eps-surprise-chart | Cigna Group Quote

CI’s Growth Drivers

CI’s first-quarter 2026 adjusted income from operations rose 12% year over year, driven by strong growth in the Cigna Healthcare and Evernorth Health Services. The company expects Evernorth Health Services’ adjusted operating income, on a pre-tax basis, to reach at least $6.9 billion in 2026, while the Cigna Healthcare unit is expected to generate a minimum of $4.5 billion in 2026. Cigna’s first-quarter 2026 adjusted revenues increased 4.7% year over year to $68.5 billion.

Business mix shifts and improved operating efficiency are major positives. The adjusted SG&A expense ratio improved to 4.8% in the reported quarter from 5.8% a year ago. Evernorth Health Services introduced a transformative pharmacy benefits model that passes drug manufacturer discounts directly to customers at the point of sale, lowering out-of-pocket costs. Cigna plans to adopt this model for its fully insured customers starting in 2027 while also raising its 2026 profits outlook for the Cigna Healthcare segment.

Cigna continues to demonstrate a strong commitment to enhancing shareholder value. The company repurchased nearly 11.9 million shares for approximately $3.6 billion in 2025. Although it didn’t make any buybacks in the first quarter, management approved a 3.3% increase in the quarterly dividend in February 2026, raising it to $1.56 per share. Its current dividend yield of 2.12% is higher than the industry average of 1.94%.

CI: Risks to Watch

There are some factors that investors should keep an eye on.

The company’s total benefits and expenses have escalated over the past several years due to higher pharmacy and other service costs. Total benefits and expenses witnessed a year-over-year increase of 4% in 2024, 12% in 2025 and 4% in the first quarter of 2026. Pharmacy and other service costs increased 12% year over year, reflecting changes in claims composition. The persistent escalation of expenses might weigh on margin growth.

Cigna has been grappling with a significant debt level over the past several years. At the end of the first quarter of 2026, it had a long-term debt of $29.4 billion, significantly higher than the cash balance of $7 billion. Its long-term debt to total capital ratio of 40.9% is slightly above the industry average of 40.5%. The elevated leverage level is likely to keep pressure on the company’s interest expenses going forward.

Key Picks

Some better-ranked stocks in the broader Medical space are BrightSpring Health Services, Inc. BTSG, Globus Medical, Inc. GMED and Centene Corporation CNC, each sporting a Zacks Rank #1 (Strong Buy) at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for BrightSpring Health’s 2026 earnings is pegged at $1.64 per share, which has witnessed five upward revisions in the past 30 days, with no movement in the opposite direction. BTSG beat earnings estimates in three of the trailing four quarters and missed once, with the average surprise being 14.6%. The consensus estimate for 2026 revenues is pinned at $15.1 billion, implying 16.6% year-over-year growth.

The Zacks Consensus Estimate for Globus Medical’s 2026 earnings is pegged at $4.66 per share, indicating a 17.1% year over year increase. GMED beat earnings estimates in each of the trailing four quarters, with the average surprise being 26.3%. The consensus estimate for 2026 revenues is pinned at $3.2 billion, implying 8.8% year-over-year growth.

The Zacks Consensus Estimate for Centene’s 2026 earnings is pegged at $3.47 per share, which has witnessed nine upward revisions in the past 30 days, with no movement in the opposite direction. CNC beat earnings estimates in three of the trailing four quarters and missed once, with the average surprise being 74.9%. The consensus estimate for 2026 revenues is pinned at $190.8 billion.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

See Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Cigna Group (CI): Free Stock Analysis Report

Centene Corporation (CNC): Free Stock Analysis Report

Globus Medical, Inc. (GMED): Free Stock Analysis Report

BrightSpring Health Services, Inc. (BTSG): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).