Microsoft-owned LinkedIn (MSFT) is the premier place people go to when they want to find a job. Strangely, LinkedIn recently fired a chunk of its own employee base, presumably due to AI. It announced that 900 employees are being let go from its global workforce of 17,500.

That may not look like a lot, but it does signal that they have started cutting back on their workforce. Usually, this would mean that budgets are tight, but that's no longer the case in 2026.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

In fact, it could signal a shift toward broader layoffs, beyond just LinkedIn. You could see healthy, fast-growing businesses start doing layoffs as they grow, simply because AI can do the job cheaper and Wall Street wants to see more money being spent on AI instead.

LinkedIn's business is performing well. The company recently reported 12% year-over-year revenue growth and had just crossed $5 billion in quarterly revenue for the first time earlier this year. CEO Daniel Shapero said the cuts were a move to "reinvent how we work, with agile teams focused on our highest priorities," while scaling back spending on marketing campaigns, vendor partnerships, customer events, and underutilized office space.

www.barchart.com

www.barchart.comMicrosoft Will Likely Keep Laying Off Workers

For the first time in its history, the company is planning voluntary early retirement for 7% of its U.S. workforce. That's on top of 15,000 workers being laid off last year, and that's even before most programming was done using AI. Now, no white-collar employee is truly "safe" from being laid off. Of course, AI cannot do everything on its own, but Microsoft needs far fewer workers to build and upkeep software now. Even non-software roles are starting to see pressure due to the barrier to entry caving in.

Microsoft's gaming, sales, and middle management may see more layoffs in the coming years. Gaming has been among the victims in recent years, and it could see more cuts due to AI. Many Microsoft employees in the gaming segment either does artwork, programming, story writing, or something along those lines. AI has cheapened all of that immensely.

Microsoft is also completely overhauling its HR function for the "AI era," and it is consolidating teams like People Analytics, Talent Management, and Culture & Inclusion. Several long-tenured HR leaders have already departed.

What this Means for MSFT Stock

As bad as it may be for employees at Microsoft, Wall Street is loving it. And I would argue, it wants to see more.

Tech companies have long had a culture of investing massively in their employees. That culture is now gone, and the competition now is to see which company can run the tightest, most efficient ship.

That's one reason why Wall Street rewarded Palantir (PLTR) so generously over the past few years. Everyone wants to cheer for the underdog, but the average white-collar worker is no longer seen as an asset at these companies.

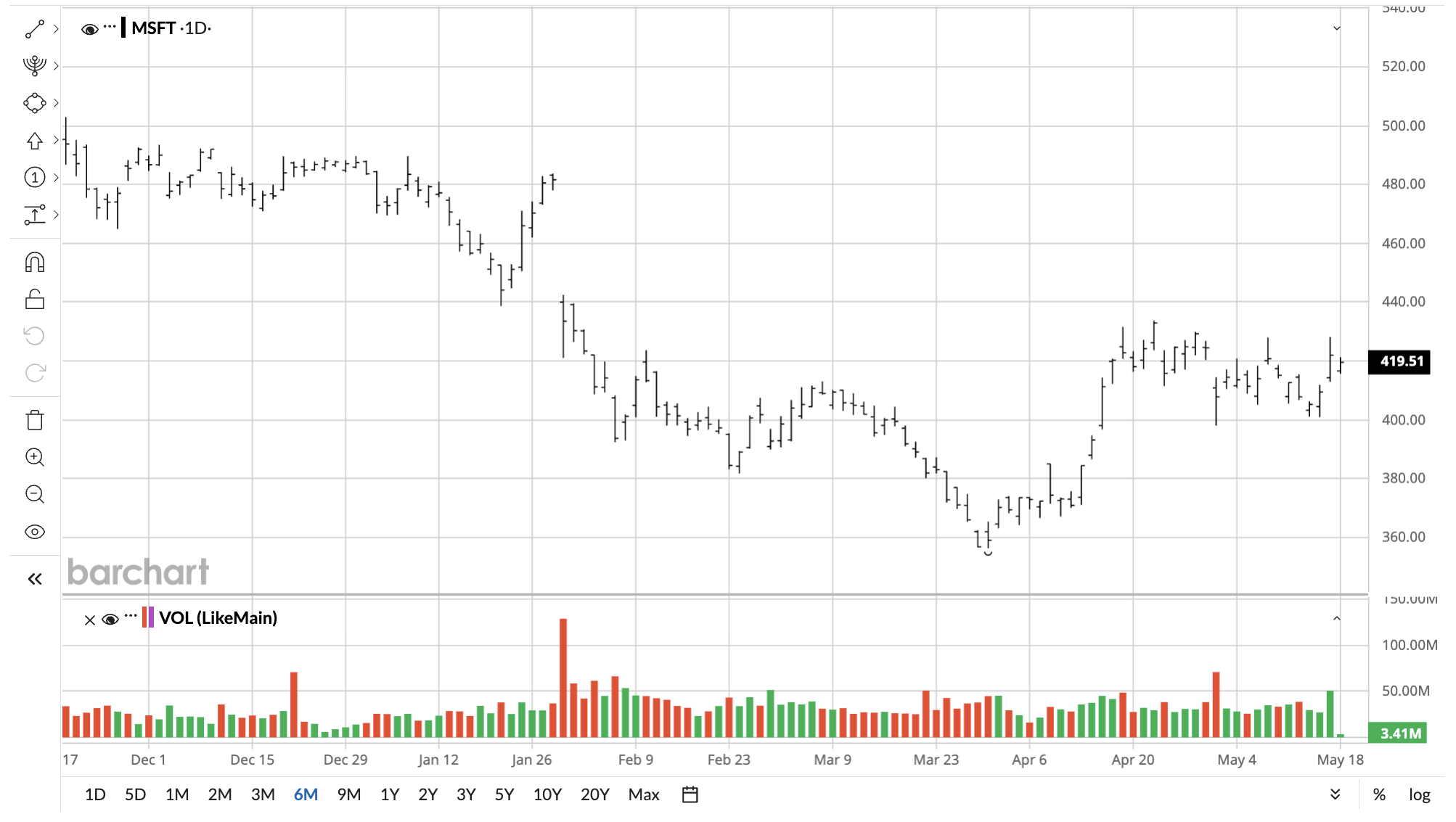

I see MSFT stock recovering substantially from here, especially if it keeps spending less on labor and more on AI. The stock has fallen by over 11% year-to-date and trades at just 25 times earnings.

Most analysts like it here and are confident it will bounce back due to Azure gaining ground.

www.barchart.com

www.barchart.comShould You Buy the Dip on MSFT Stock?

Microsoft is shifting from a bet on software-as-a-service to a bet on AI. AI is moving at such speed that even tools like Excel are being increasingly automated, and you may no longer see enterprises send checks to Microsoft for their subscriptions.

However, these enterprises will still have to pay for AI. In turn, an AI provider will have to buy compute. Microsoft is trying to build the infrastructure for that compute so it can counterbalance anything it loses on the software side, and this is more or less what it boils down to at this stage.

I would expect this buildout stage to last longer as hyperscalers still have cash. Their software arms are generating enough cash flow to fund hundreds of billions for data center projects, which in turn is driving sales growth.

In a few years, you will either see those data centers start churning out cash or leave Microsoft with net debt and bad return on investment metrics. Either way, I expect tremendous gains in a few years. No one knows where all of this data center spending will take Microsoft in 2030, but even if it turns out to be a disaster, you don't want to miss out on the gains in between.

MSFT stock is a “Buy.”

On the date of publication, Omor Ibne Ehsan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Dear Intuit Stock Fans, Mark Your Calendars for May 20 Wall Street Is Loving the Layoffs at Microsoft. Buy the Dip. 3G Capital Exits Microsoft Stock in Major Portfolio Shift. MSFT Is Still One of the Best AI Plays Now. Dear Google Stock Fans, Mark Your Calendars for May 19