Shares of Snowflake (SNOW) are having a difficult year, with the cloud data platform provider sliding firmly into negative territory amid a sharp sell-off across the enterprise software sector. Much of the pressure stemmed from a broader market repricing fueled by growing fears that the rise of agentic AI technologies from companies like Anthropic and OpenAI could disrupt the traditional Software-as-a-Service (SaaS) model.

At the same time, intensifying competition in the cloud analytics space and lingering concerns over whether Snowflake can monetize generative artificial intelligence (AI) quickly enough to support its premium valuation further weighed on investor sentiment. Still, the mood around the stock appears to be shifting. Shares rebounded roughly 4.3% on Monday as investors began dialing back fears that AI poses an immediate existential threat to established software companies.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Market experts pointed out that firms like Snowflake still hold major competitive advantages, including deeply embedded enterprise relationships, enormous pools of proprietary data, and mission-critical integration within customer workflows, strengths that AI is unlikely to replace anytime soon. With sentiment beginning to stabilize, attention is now turning toward Snowflake’s fiscal 2027 first-quarter earnings report, scheduled for release after the close of U.S. markets on Wednesday, May 27. Ahead of the highly anticipated event, let’s take a closer look at SNOW.

About Snowflake Stock

Founded in 2012, Snowflake has evolved into one of the most influential names in cloud data and analytics. The company built its reputation by helping enterprises break down data silos and unify massive amounts of information across multiple cloud environments through its AI Data Cloud platform. Its technology enables businesses to store, process, analyze, and share data seamlessly across leading cloud providers such as Amazon (AMZN) Web Services (AWS), Microsoft (MSFT) Azure, and Alphabet (GOOG) (GOOGL) Google Cloud.

Beyond traditional data warehousing, Snowflake has aggressively expanded into AI, machine learning, cybersecurity, and real-time analytics tools, positioning itself at the center of the enterprise AI race. Products like Cortex AI, Snowpark, and its native app ecosystem are designed to help organizations build AI-powered applications directly on top of their data without moving it across systems.

As companies increasingly look to turn data into competitive advantage, Snowflake has become a critical infrastructure layer powering everything from customer analytics and cybersecurity monitoring to financial forecasting and generative AI applications. The company’s market capitalization currently stands at $56.78 billion.

Today, more than 12,000 customers worldwide rely on Snowflake to break down data silos, run complex workloads, and unlock deeper insights from their information, while the platform handles an astonishing average of more than 6.3 billion queries every single day, underscoring the enormous scale and growing importance of its ecosystem.

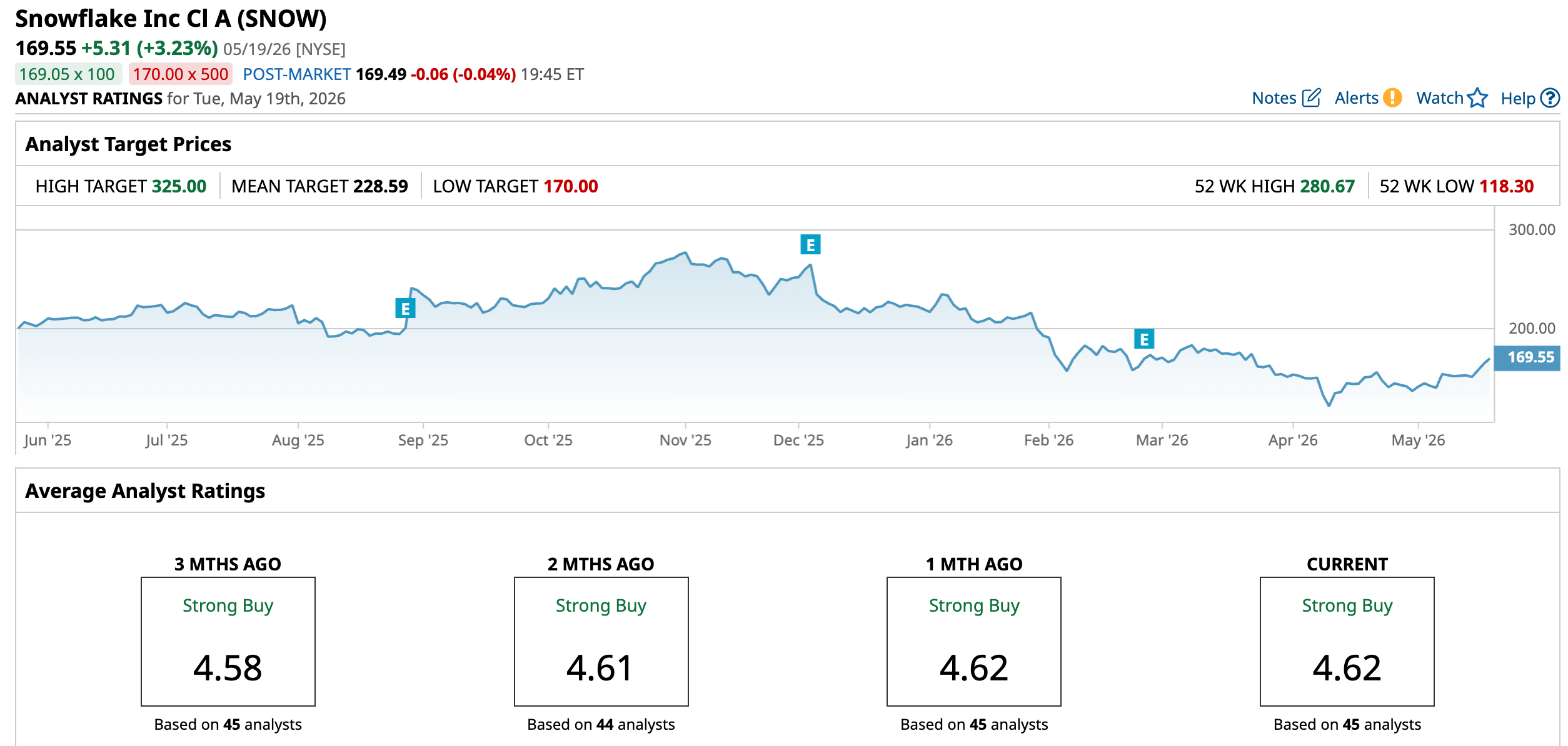

However, despite Snowflake continuing to expand its presence in the enterprise AI and cloud data markets, the stock’s performance has remained underwhelming. Shares are down 6.87% over the past year, dramatically trailing the broader S&P 500 Index ($SPX), which has rallied 23.31% during the same period. Although the stock has staged a modest rebound of 17.76% over the past month, the bigger picture remains challenging.

In 2026 alone, Snowflake shares are still down approximately 22.71% year-to-date (YTD), a sharp contrast to the broader market’s 7.42% gain so far this year. The decline becomes even more striking when viewed from its 52-week high of $280.67 reached last November, with the stock having plunged nearly 39.6% since that peak. Despite the sharp pullback so far in 2026, Snowflake still commands a rich valuations in the software space. The stock is currently trading at roughly 11.62 times sales, a massive premium compared to the sector median of just 3.26 times.

www.barchart.com

www.barchart.com Snowflake’s Q4 Earnings Snapshot

Snowflake delivered an impressive performance in its fiscal 2026 fourth-quarter earnings report released on Feb. 25, posting a strong double-beat on both revenue and earnings that provided a much-needed boost to investor confidence. Total revenue climbed 30.1% year-over-year (YOY) to $1.28 billion, comfortably topping Wall Street’s expectations of $1.26 billion. The strong showing was largely fueled by product revenue, which surged to $1.23 billion during the quarter, also marking a robust 30% annual increase.

Enterprise demand remained a major bright spot. Snowflake recorded its strongest-ever quarter for net new customer additions, adding 740 net new customers during the period, an impressive 40% jump from a year ago. The company achieved a record number of customers surpassing $10 million in trailing 12-month spending, highlighting the growing strategic importance of its platform among large enterprises.

In addition, Snowflake ended the quarter with 733 customers generating more than $1 million in trailing 12-month product revenue, representing 27% YOY growth. At the same time, the company’s Net Revenue Retention (NRR) rate remained strong at 125%, underscoring that existing customers continue expanding their data and AI workloads on the platform.

One of the most closely watched metrics in the report was Snowflake’s Remaining Performance Obligations (RPO), which reflects future contracted revenue. That figure surged 42% YOY to $9.77 billion, signaling strong long-term commitments from enterprise customers and reinforcing confidence in the company’s future growth pipeline.

However, profitability remains a work in progress. On a GAAP basis, Snowflake reported a steep net operating loss of $318 million for the quarter, translating to a per-share loss of $0.90, as heavy research-and-development spending and sizable stock-based compensation expenses continued to weigh on earnings. Still, the company delivered far stronger results on an adjusted basis. Non-GAAP earnings came in at $0.32 per share, up from $0.30 in the year-ago quarter and well ahead of Wall Street’s estimate of $0.27 per share.

Looking ahead, management expects product revenue for the upcoming quarter to range between $1.262 billion and $1.267 billion, representing approximately 27% YOY growth at the midpoint. Snowflake guided for fiscal 2027 product revenue of $5.66 billion. While that outlook still reflects a healthy 27% pace of expansion, it also points to a modest slowdown compared to the 29% product revenue growth the company delivered during full-year fiscal 2026.

What Do Analysts Think About Snowflake Stock?

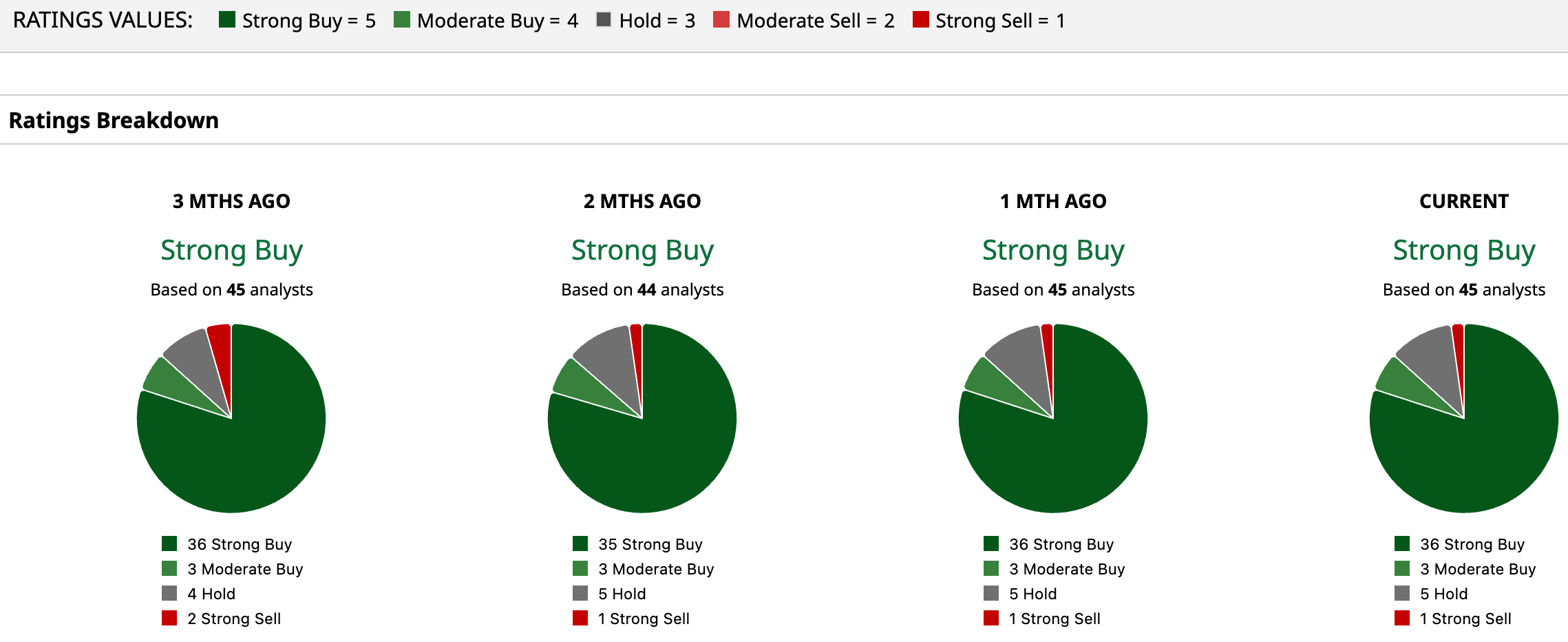

Even amid the stock’s turbulent performance so far in 2026, Wall Street continues to show remarkable confidence in Snowflake and its long-term growth trajectory. The company currently holds a consensus “Strong Buy” rating, underscoring analysts’ belief that Snowflake remains one of the most compelling players in the rapidly expanding AI-driven data infrastructure market.

Out of the 45 analysts covering the stock, a dominant 36 have assigned “Strong Buy” ratings, while three additional analysts recommend “Moderate Buy.” Only five analysts remain cautious with “Hold” ratings, and just one analyst on Wall Street has issued a “Strong Sell” recommendation, a clear sign that bullish sentiment continues to outweigh skepticism despite the stock’s recent struggles. Price targets further highlight the optimism surrounding the company’s future potential.

The average analyst target of $228.59 suggests that SNOW could climb approximately 34.8% from current levels. Even more striking, the Street-high target of $325 implies that some analysts believe the stock could nearly double from here, representing a potential upside of as much as 91.7% if Snowflake successfully strengthens its position in AI, cloud analytics, and enterprise data management.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com On the date of publication, Anushka Mukherji did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Dear Snowflake Stock Fans, Mark Your Calendars for May 27 Palo Alto Networks Just Got a New Street-High Price Target. Analysts Are Betting Big on PANW Stock Before June 2. GameStop Wants to Buy eBay. It Could Collapse Its Credit Rating and Valuation in the Process. Why Bill Ackman Thinks the Selloff in Microsoft Stock Is Misguided