Toll Brothers, Inc. TOL reported second-quarter fiscal 2026 (ended April 30) results, with earnings and revenues beating the Zacks Consensus Estimate. However, both the top and bottom lines declined on a year-over-year basis.

TOL’s top-line beat was underpinned by steady demand across its footprint and a favorable mix that lifted delivered pricing. The company’s average price on home deliveries rose meaningfully from last year, helping cushion the impact of lower unit volume.

On a macro level, the company navigated a challenging housing market characterized by pressures such as volatile mortgage rates, elevated inflation and fluctuations in luxury home demand.

Following the announcement, shares of TOL gained 2.3% in the after-hours trading session yesterday.

TOL’s Quarterly Earnings & Revenue Discussion

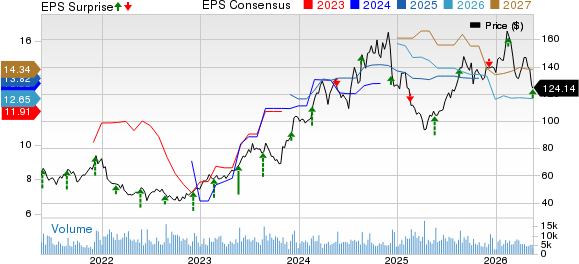

The company reported adjusted earnings per share (EPS) of $2.72, which beat the Zacks Consensus Estimate of $2.58 by 5.4% but declined 22.3% year over year.

Toll Brothers Inc. Price, Consensus and EPS Surprise

Toll Brothers Inc. price-consensus-eps-surprise-chart | Toll Brothers Inc. Quote

In the fiscal second quarter, total revenues of $2.53 billion surpassed the consensus mark of $2.41 billion by 5.1% but fell 7.6% from the year-ago quarter.

Inside Toll Brothers’ Q2 Results

For the quarter under review, Toll Brothers’ total home sales revenues decreased 7.2% (down from our projection of a 11.5% year-over-year decline) year over year to $2.51 billion from $2.71 billion. Home deliveries declined 14.1% to 2,491 units from 2,899 units in the year-ago quarter (down from our expectation of a 15.4% decline year over year).

Despite the lower volume, the average delivered price increased 8% year over year to about $1,008,600 from $933,600, highlighting a favorable pricing and mix backdrop in the luxury segment. Our model had expected ASP to be up 4.5% year over year to $975,900.

Toll Brothers’ Orders Grow While Backlog Stays Solid

Order momentum remained a constructive signal for a builder operating in a rate-sensitive environment. Net signed contracts increased 6.9% year over year to 2,834 homes, and contract value rose 8.1% to $2.81 billion, reflecting steady demand from higher-income buyers despite broader affordability pressures. We had projected net-signed contracts to be up 4% in units and 5.1% in value for the quarter.

Backlog ended the quarter at 5,394 homes valued at $6.32 billion, down 11% and 7.6%, respectively, from the prior-year period. Even so, the average price of homes in the backlog was $1,171,800, up from $1,128,100 a year ago. Cancellations were controlled, with quarterly cancellations at 4.8% of signed contracts, improving from 6.2% a year ago.

TOL Faces Margin Pressure From Write-Downs and Costs

While operations were strong enough to drive a revenue beat, profitability was pressured by lower margins and higher costs. Home sales gross margin fell to 23.9% from 26% a year ago, and adjusted home sales gross margin declined to 26.2% from 27.5%, reflecting a less favorable margin environment.

A key drag came from higher inventory impairments and write-offs embedded in home sales cost of revenues. SG&A also moved higher as a percentage of home sales revenues to 10.3% from 9.5%, further constraining year-over-year earnings performance.

Toll Brothers’ Capital Position Supports Shareholder Returns

Toll Brothers continued returning capital while maintaining a strong liquidity position. The company repurchased about 1.2 million shares during the quarter for $175.4 million at an average price of $143.72, and it increased its quarterly dividend to 26 cents per share.

Liquidity remained substantial, with cash and cash equivalents of $1.11 billion at quarter-end, down from $1.26 billion as of Oct. 31, 2025. Available liquidity under the senior unsecured revolving credit facility was $2.24 billion, reflecting strong capacity under the expanded $2.38 billion facility. Leverage stayed conservative, with the debt-to-capital at 24.7% at quarter-end (down from 26% at fiscal 2025 year-end). Net debt-to-capital was 15.4%, slightly above 15.3% at fiscal 2025 year-end, indicating only a modest uptick in net leverage while the company continued investing for growth.

TOL Updates Q3 & FY26 Targets

Management raised full-year guidance across key homebuilding metrics based on year-to-date performance. For the third quarter, TOL expects deliveries of 2,600-2,700 units (compared with 2,959 units delivered in the prior-year quarter) and an average delivered price of $965,000-$985,000 (compared with $973,600 in the year-ago quarter). Adjusted home sales gross margin is projected at 25.25%, implying a decline from 25.6% in the year-ago period. SG&A is estimated at 10.0% of home sales revenues and a tax rate of 26%.

For full-year fiscal 2026, TOL forecasts deliveries of 10,400-10,700 units. The estimated range reflects a decline from the fiscal 2025 level of 11,292. Average delivered price of $985,000-$1,000,000, indicating growth from $960,200 in fiscal 2025. The company now sees adjusted home sales gross margin at 26.10% (a decline from the 27.3% reported in fiscal 2025) and SG&A at 10.10% of home sales revenues, with period-end community count projected at 480-490.

TOL’s Zacks Rank & Recent Construction Releases

Toll Brothers currently has a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Vulcan Materials Company VMC posted exceptional first-quarter 2026 results with adjusted earnings and total revenues beating the Zacks Consensus Estimate and increasing year over year. The quarter’s results reflect benefits realized from the aggregates-led business and consistent focus on its strategic disciplines. Besides, efforts to incorporate top-tier innovation and technology advancements also aided the quarter’s financial performance.

Vulcan reiterated its full-year adjusted EBITDA outlook of $2.4-$2.6 billion and cited a healthy backlog supported by large projects and public construction activity.

EMCOR Group, Inc. EME reported impressive first-quarter 2026 results, with earnings and revenues topping the Zacks Consensus Estimate and increasing year over year on strong demand across its core markets.

The company’s quarterly results reflect continued momentum across key end markets and customers’ confidence in its ability to execute complex and mission-critical projects. Strong activity in sectors like Network and Communications, Institutional, Healthcare, and Water and Wastewater supported growth and drove higher remaining performance obligations. EMCOR now expects revenues between $18.50 billion and $19.25 billion, and diluted earnings per share are projected in the range of $28.25 to $29.75.

Comfort Systems USA, Inc. FIX delivered a sharp first quarter of 2026, with earnings and revenues topping the Zacks Consensus Estimate and increasing year over year. The quarter reflected strong market conditions, led by heavier technology-sector activity, particularly for data centers.

Comfort Systems also highlighted that recent bookings and underlying persistent demand supported a higher backlog even with increased project burn rates, an important indicator that volume remains strong across key end markets. The backlog as of March 31, 2026, totaled $12.45 billion, increasing 4.3% from $11.94 billion on Dec. 31, 2025, and jumping 80.8% from $6.89 billion reported a year ago.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power .

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Vulcan Materials Company (VMC): Free Stock Analysis Report

Toll Brothers Inc. (TOL): Free Stock Analysis Report

EMCOR Group, Inc. (EME): Free Stock Analysis Report

Comfort Systems USA, Inc. (FIX): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).