Tesla (TSLA) is one of the hardest stocks to judge in the market. The company still sells electric cars, but the bigger debate is about what it could become. That is why a fresh report that Tesla is ramping up “urgent” hiring for Full Self-Driving (FSD) work in China matters so much. It tells investors the company is still leaning hard into autonomy, even as the electric vehicle (EV) market remains choppy and competition stays intense.

China is the key piece here. It is the world’s biggest auto market, and Tesla has been losing ground there to local players. At the same time, TSLA stock has continued drawing buyers because the market is still willing to pay for the robotaxi, software, and AI story. That keeps Tesla in a strange spot. The near-term business looks uneven, but the long-term pitch still has a lot of power.

Don’t Miss a Day: From crude oil to coffee, sign up free for Barchart’s best-in-class commodity analysis.

Tesla Stock Still Has Momentum, But It's Not Cheap

Tesla shares have climbed about 25% over the past year, helped by investor excitement around autonomy and AI. TSLA stock stumbled earlier in 2026, then bounced back from its April lows. The stock has also stayed above its 200-day moving average, which suggests the long-term trend remains intact even after some short-term weakness.

The valuation is still rich, however. Tesla trades at a price-to-earnings (P/E) ratio of about 346.7 times, which is far above the sector median of roughly 15 times. Its price-to-book ratio is around 18.4 times, compared to a sector median near 2 times.

That is a big premium. Bulls say Tesla deserves it because of its growth optionality and cash generation. Bears say TSLA stock already prices in a lot of success that has not shown up yet.

www.barchart.com

www.barchart.com China Hiring Adds to the FSD Story

The latest China hiring push gives Tesla another reason to stay in focus. The company is posting “urgent” job openings tied to FSD testing, data work, and driver-assistance roles across major Chinese cities. That matters because Tesla has been trying to catch up in a market where local rivals are moving fast on smart-driving features.

Investors generally like the signal. It shows Tesla is not slowing down on autonomy and is still trying to build a global FSD business. But it also shows the challenge. China is not an easy rollout. Regulation is still a hurdle, and Tesla will need execution to turn this hiring push into real progress.

For TSLA stock, the news is supportive because it keeps the long-term growth story alive.

Tesla Q1 Earnings Showed Progress, But Spending Is Rising Fast

Tesla’s March quarter gave bulls and bears something to point to. Revenue came in at $22.39 billion, up 16% from a year earlier. Automotive revenue was $16.23 billion, energy generation and storage brought in $2.41 billion, and services and other revenue reached $3.75 billion. That mix matters because it shows Tesla is getting more out of software and services, not just car deliveries.

Net income attributable to common stockholders was $477 million, up from $409 million a year ago. Adjusted earnings were about $0.41 per share. Free cash flow came in at $1.44 billion, and Tesla ended the quarter with $44.74 billion in cash, cash equivalents, and short-term investments. That gives the company a cushion.

There was also a useful sign on autonomy. Tesla said paid robotaxi miles nearly doubled sequentially in the quarter. CEO Elon Musk said that kind of growth supports the idea that autonomy is moving from theory to real usage.

The catch is spending. Tesla now expects capital spending to top $25 billion in 2026. That is a huge figure, and it raises the risk of negative free cash flow later this year. So, the quarter was solid, but it also showed how expensive the next phase could be.

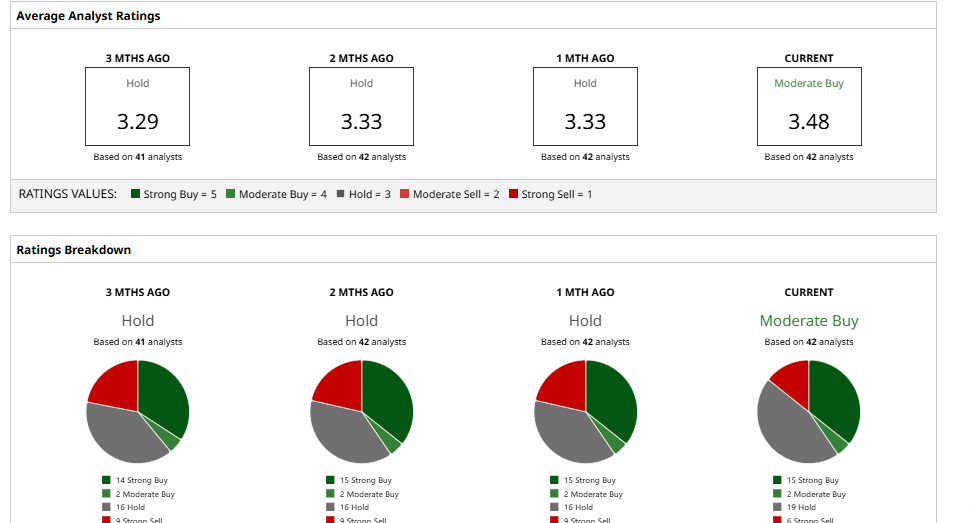

What Do Analysts Think of Tesla Stock?

Wall Street still cannot agree on Tesla. Morgan Stanley has a neutral view and a target of around $415, saying the company’s spending plans and execution risk still matter. Goldman Sachs is also cautious on TSLA stock with a “Neutral” rating and a $375 target. Analysts point to Tesla’s heavy capex and the chance that free cash flow could turn negative for the rest of 2026.

TD Cowen is more upbeat. The firm recently kept a “Buy” rating and a $490 target, arguing that autonomy and robotics could unlock more value over time. Barclays remains more cautious with a target near $360.

Overall, the consensus is a “Moderate Buy” rating with a mean price target of $401.77. Tesla stock has already surpassed that target and is currently moving toward its Street-high target of $600.

That split tells the story. Tesla is still expensive, still controversial, and still tied to a future that is not yet here. For now, though, the market is willing to pay for the China FSD push, the robotaxi dream, and the chance that Musk can turn those bets into something bigger.

www.barchart.com

www.barchart.com On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Tesla Is Chasing the Future of Driving. Its Stock Is Stuck in a 350x Earnings Trap How High Can Gasoline Rise During the 2026 Driving Season? BE Stock Alert: Bloom Energy, Nebius Enter Into $2.6 Billion Agreement Grains, Livestock, and Geopolitics: How to Read What the Ag Markets Are Actually Telling Us