Meta Platforms (META) has quietly added a new reason for investors to pay attention. Just a few days ago, the company launched Forum, a stand-alone app for Facebook Groups that looks a lot like Reddit (RDDT), while Meta’s app ecosystem still reaches 3.56 billion daily active users.

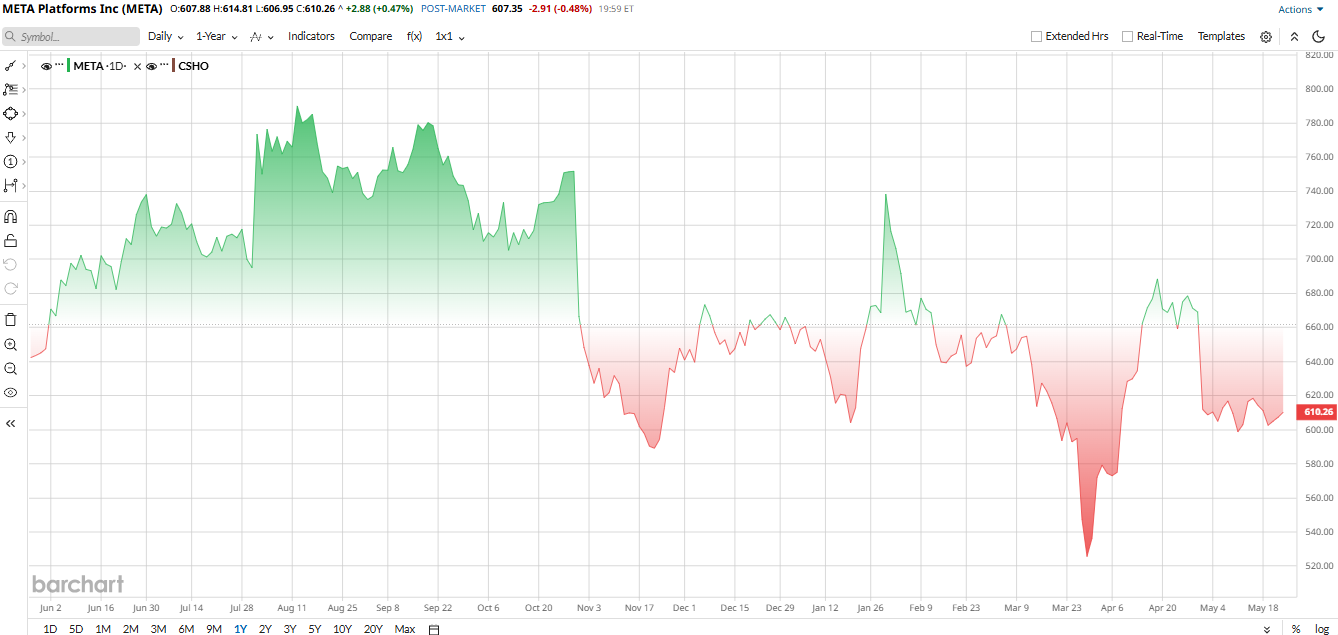

The stock, meanwhile, has been choppy. META is down more than 7% year-to-date, underperforming the broader market index as worries over AI spending and legal risk persist.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

www.barchart.com

www.barchart.com Meta Is Taking Another Shot at Community Apps

Forum is a small product launch on paper, but it fits a bigger strategy. Meta describes Forum as a “dedicated space for deeper discussions, real answers, and the communities you care about” with feeds built around group conversations and an AI-powered “Ask” tab. It is also not Meta’s first try at a standalone Groups product, which makes the company’s willingness to revisit the idea notable. If Forum gains traction, it could create another layer of sticky engagement and ad inventory; if it does not, it becomes another experiment in a long list of Meta side bets.

AI Spending Is Still Pressuring the Stock

The bigger stock story, though, has been Meta’s capital-spending spree. In late April, the company raised its 2026 capex outlook to $125 billion to $145 billion, up from $115 billion to $135 billion, and shares dropped more than 6% in extended trading as investors absorbed the scale of the AI bill.

Meta also said it expects full-year expenses of $162 billion to $169 billion and warned that legal and regulatory issues in the U.S. and Europe could materially affect results. The market’s message has been clear: Strong growth is no longer enough on its own if the payoff from AI still looks far away.

On valuation terms, Meta is not cheap in absolute terms, but it is also not priced like a runaway AI darling. The stock trades at about 22.2 times earnings, and its price-to-sales ratio is around 7.2.

At the same time, Meta is still delivering fast growth, so the multiple is being anchored more by confidence in future profits than by today’s revenue alone. That is why the stock can look expensive on sales and reasonable on earnings at the same time.

Meta’s Latest Quarter Was Strong

The latest quarter was strong enough to make that tension harder to ignore. Meta said first-quarter revenue rose 33% year-over-year to $56.31 billion, while advertising revenue also came in at $55.02 billion.

Diluted EPS jumped to $10.44 from $6.43 a year earlier, though that included an $8.03 billion tax benefit. Free cash flow was $12.39 billion, operating cash flow was $32.23 billion, and Meta ended the quarter with $81.18 billion in cash, cash equivalents, and marketable securities. Management also guided for second-quarter revenue of $58 billion to $61 billion, with full-year expenses still expected at $162 billion to $169 billion.

The core business is still doing the heavy lifting. Family of Apps revenue totaled $55.91 billion, while Reality Labs brought in just $402 million and posted a $4.03 billion operating loss. Ad impressions rose 19%, and average price per ad climbed 12%, a useful reminder that Meta is still proving it can grow both volume and pricing at the same time. That is the kind of operating backdrop that can eventually pull a stock out of the penalty box, even if the market is not ready to reward it yet.

What Wall Street Thinks About Meta Stock

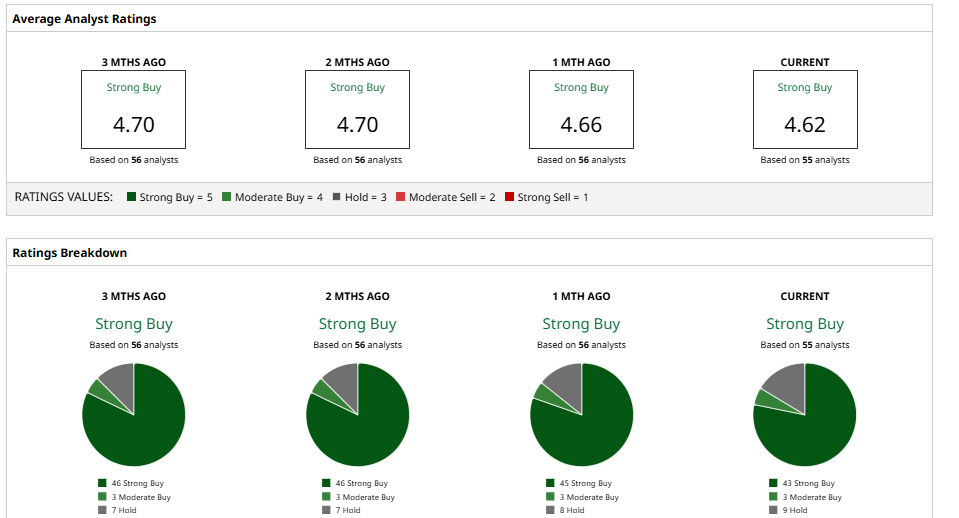

Even after a rough year for the stock, most analysts are pounding the table. The consensus rating remains a “Strong Buy,” with an average 12-month price target sitting right around $823, implying a 35% upside from current levels.

Separately, BofA analyst Justin Post recently boosted his target to $835 and kept a “Buy” rating, pointing to a massive runway for AI-driven ad tools.

Moreover, Mizuho’s Lloyd Walmsley, while trimming his target slightly to $835, remains firmly bullish, predicting new consumer AI products will unlock fresh monetization opportunities.

Not everyone is fearless. Jefferies recently lowered its price target to $825. Wells Fargo’s Ken Gawrelski nudged his target down to $765, acknowledging that the sheer size of the capex budget is a risk that can’t be ignored.

www.barchart.com

www.barchart.com On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Oklo Stock Gets a New ‘Buy’ Rating from Bank of America: It’s an ‘Early Leader’ 1 Mega-Cap Tech Stock With 35% Upside Just Dropped a Reddit-Like App BlackBerry Just Hit a New 52-Week High. Here's Why Walmart Is Supposed to Be a Safe-Haven Stock. High Gas Prices Are Hitting Its Shares Instead.