Beneath Amazon’s (AMZN) retail and cloud business, a much bigger story is unfolding. Amazon is approaching AI very differently from its rivals, and this difference could eventually become its biggest competitive advantage. AMZN stock is up 17% year-to-date (YTD), outperforming the broader market gain of 9.6%.

Is AMZN stock a good buy now?

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

www.barchart.com

www.barchart.com Amazon Is Playing Both Sides of the AI Chip Race

Many investors may not be aware that Amazon, renowned mostly for its retail and e-commerce business, has quietly built a massive AI chip business. In the first quarter, its chips division grew nearly 40% sequentially and now exceeds a $20 billion annual revenue run rate. Its Trainium AI chips, in particular, have already secured more than $225 billion in revenue commitments, with most of them from leading AI labs including Anthropic and OpenAI. Amazon claims that its “custom silicon business” is now likely one of the three largest data center chip businesses globally. This is impressive given that Amazon entered the custom AI chip race much later than other competitors. Meanwhile, Amazon believes that its Graviton CPU processors will play an essential role as AI workloads progress beyond simple inference to agentic AI.

While Amazon is aggressively expanding its chip business, it still continues to deepen its relationship with Nvidia Corporation (NVDA). CEO Andrew R. Jassy made it clear that Amazon has no intention of abandoning Nvidia hardware. In fact, he believes that many enterprises will continue choosing Nvidia chips, while others may prioritize Trainium’s lower cost structure and performance advantages.

This is probably true because while Amazon’s chips are substantially cheaper, they lack Nvidia’s state-of-the-art and mature ecosystem. Nvidia chips still remain the industry standard for their highest processing speeds.

Amazon’s dual approach is an advantage for the company, as it can save huge amounts of money every year by using its own chips instead of purchasing as many third-party GPUs. This could help the company ultimately boost its profit margins, as expenditures to gain an AI advantage keep rising each year. Notably, Amazon’s capital expenditures surged to $43.2 billion during the quarter, largely driven by AWS and generative AI infrastructure investments. Amazon believes these investments will generate huge long-term returns as data centers can operate for more than 30 years, while servers and chips often remain productive for five to six years.

Amazon’s AI Ambitions Go Far Beyond the Cloud

Thanks to AI, Amazon Web Services (AWS) had one of its strongest quarters in years, with a 28% increase in revenue to $37.6 billion. It is now operating at a staggering $150 billion annualized revenue run rate. However, Amazon’s long-term AI strategy now stretches beyond traditional cloud computing entirely. Most AI companies focus primarily on the software side. But Amazon, with its massive retail and logistics networks, has the opportunity to test and deploy AI at enormous scale across its physical operations.

Amazon has already integrated AI across warehouse automation, robotics, inventory forecasting, delivery optimization, advertising, customer recommendations, and supply chain management. This massive amount of operational data allows Amazon to continuously improve its systems.

Moreover, Amazon believes the biggest long-term opportunity lies in “agentic AI.” Customer spending for its Bedrock platform, which allows customers to access and build AI applications using multiple foundation models, jumped 170% sequentially. In just one quarter, Bedrock handled more tokens than all its earlier years combined. The company now also has OpenAI models available through Bedrock.

Furthermore, its Zoox autonomous driving business will soon integrate with Uber (UBER). Meanwhile, Amazon LEO satellite services are nearing commercial launch, with commitments from companies and governments including Delta Air Lines (DAL), AT&T (T), Vodafone (VOD), NASA, and others. Amazon has partnered with Apple (AAPL) to help power satellite connectivity services for iPhones and Apple Watches.

One of the biggest advantages of Amazon’s AI strategy is diversification. Amazon is embedding AI into infrastructure, commerce, logistics, healthcare, media, transportation, devices, and communications simultaneously. This strategy makes Amazon’s AI game look completely different from every other tech giant.

In the first quarter, Amazon’s total revenue increased by 17% year-over-year (YOY) to $181.5 billion, while adjusted earnings rose 75% to $2.80 per share. Analysts predict Amazon’s earnings to increase by 20.9% in 2026, followed by another 14% in 2027. These projections suggest Wall Street largely believes Amazon’s aggressive AI strategy, cloud dominance, and custom chip investments could drive another major growth cycle over the next several years.

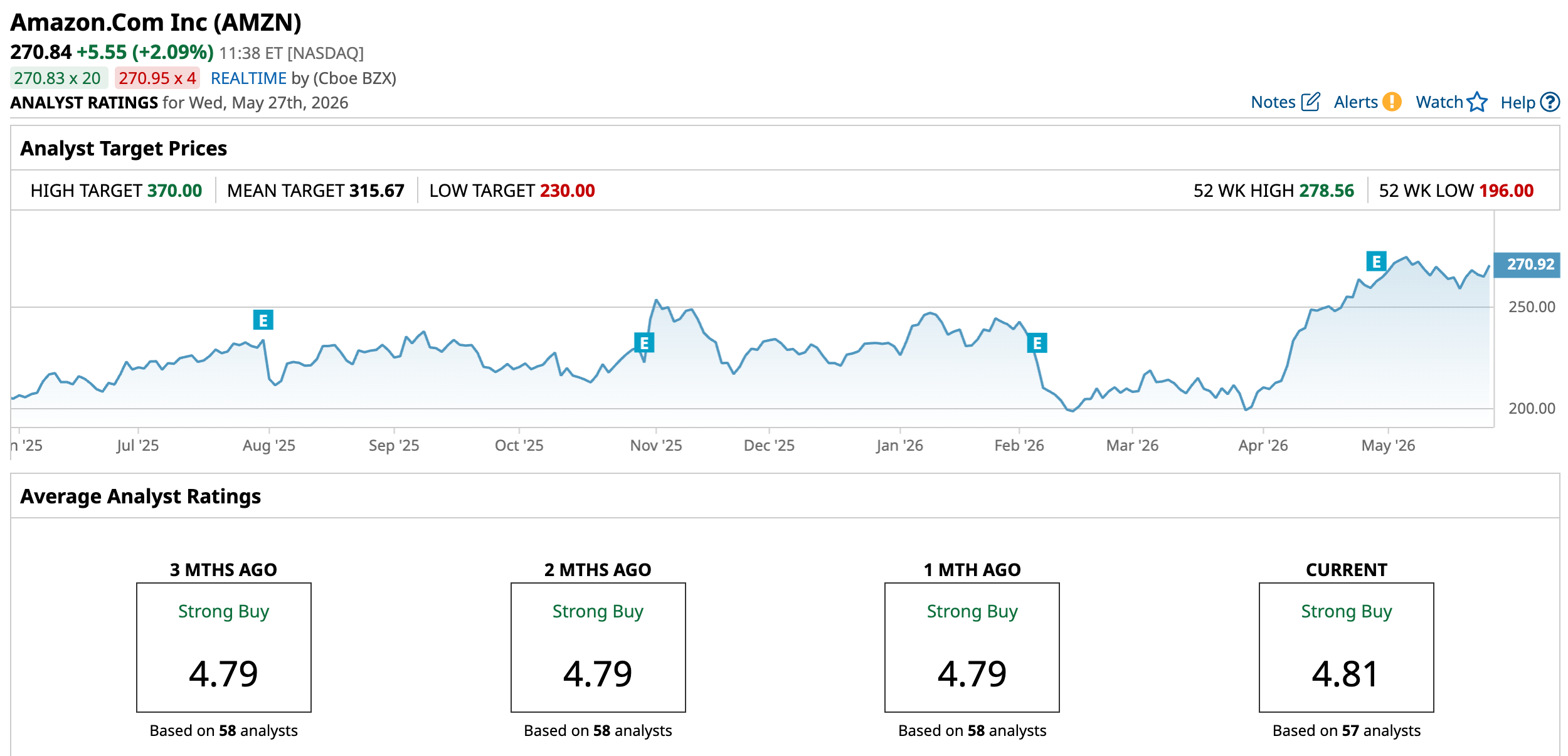

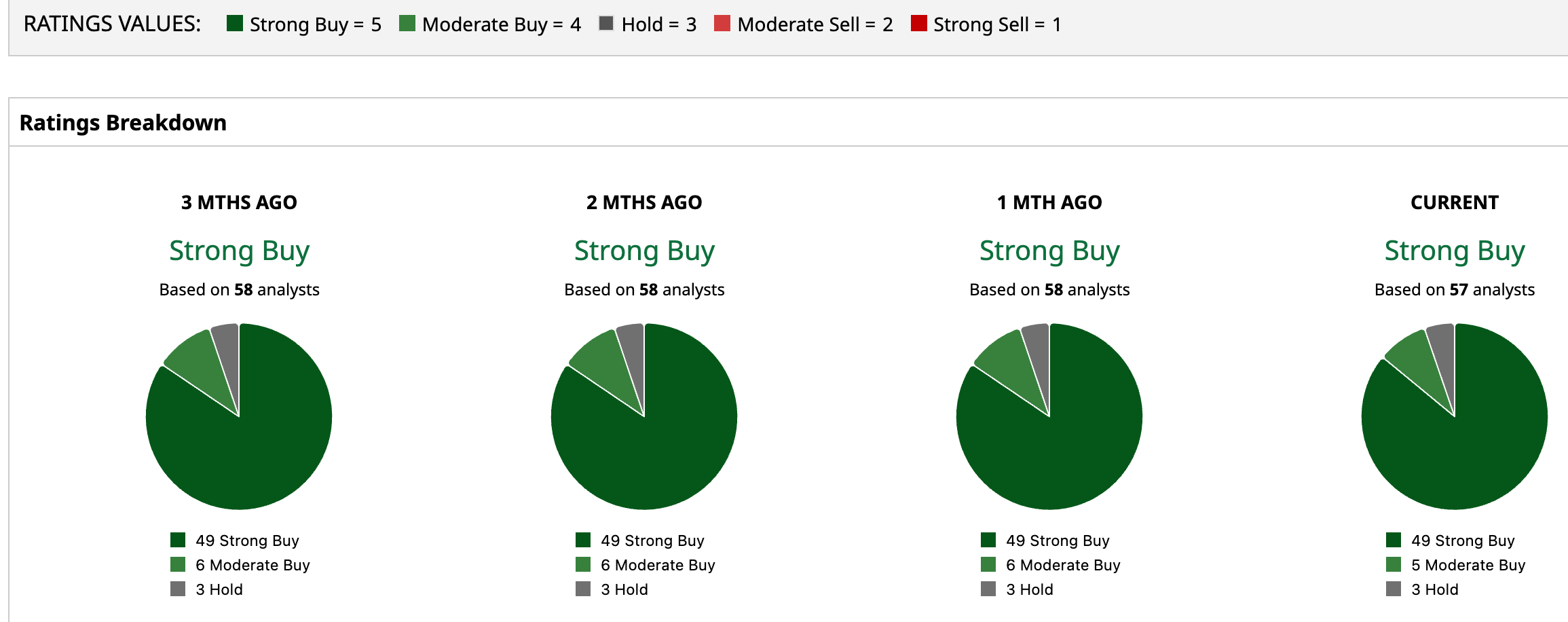

Overall, on Wall Street, AMZN stock has earned a consensus “Strong Buy.” Of the 57 analysts covering the stock, 49 have a “Strong Buy,” five have a "Moderate Buy" rating, and three analysts rate the stock as a “Hold.” The stock’s mean target price of $315.67 implies 16.55% potential upside from current levels. Plus, the high target price of $370 suggests that shares could climb as much as 36.6% over the next year.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Bank of America Says Nvidia Is Still the Top AI Compute Stock to Buy Despite YTD Underperformance. Here’s Why. Why Amazon’s AI Game Looks Completely Different Than Every Other Tech Giant Tesla Has a SpaceX Stake and $890 Million in Related Revenue. The Upcoming SpaceX IPO Could Be a Major Win for TSLA Stock. As Micron Heeds Trump’s Call for Domestic DRAM Manufacturing, MU Stock Is Still Undervalued