NeuroPace, Inc. NPCE is moving through a clean strategic reset in 2026. The company is exiting the DIXI Medical distribution business and leaning fully into its core responsive neurostimulation franchise, where reimbursement and pricing actions are improving unit economics.

At the same time, management is still funding growth. Commercial and research and development spending remain elevated, and procedure timing can swing quarterly results even when demand signals look strong.

NPCE Beats Q1 Estimates, Raises Outlook

First-quarter 2026 revenues were $22.1 million, down 2% year over year, but the mix mattered. Core RNS System revenues were $21.7 million, up 19.5% year over year, while service revenues were $314,000 and DIXI Medical contributed just $0.1 million during the wind-down.

Losses also improved. Adjusted loss per share narrowed to 13 cents from 18 cents a year ago, and adjusted operating loss improved to $3.3 million from $4.1 million.

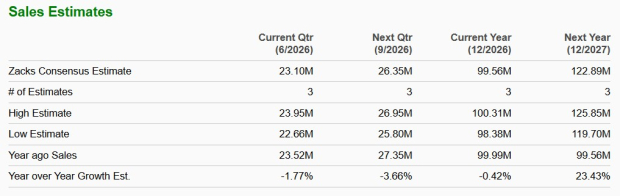

Management raised full-year 2026 revenue guidance to $99 million-$101 million (up from $98 million-$100 million) on a continuing-operations basis. The margin commentary was equally important: first-quarter adjusted gross margin was 82.5%, and management attributed underlying year-over-year gains, excluding one-time items, to manufacturing efficiency and a higher average selling price from pricing conversion.

NeuroPace, Inc. Price and EPS Surprise

NeuroPace, Inc. price-eps-surprise | NeuroPace, Inc. Quote

NeuroPace Margin Setup After Medicare Rate Changes

A key 2026 tailwind is the Medicare reimbursement uplift effective Jan. 1, 2026, which increases hospital replacement payments and physician fees. That changes the economics of both doing and supporting procedures, which can reinforce a hospital’s and physicians' willingness to adopt the system and replace it over time as volume builds.

Those reimbursement dynamics also support pricing discipline. Management continues low- to mid-single-digit price increases, and these levers are already showing through in core results as the business mix shifts fully to RNS.

Against that backdrop, management reiterated the adjusted gross margin of 81.5% to 82.5% for 2026. The guidance frames the margin setup as sustainable, not a one-quarter artifact.

NPCE Sales Spend vs. Operating Leverage Timeline

Even with improving unit economics, 2026 still implies adjusted EBITDA losses. Management guided adjusted EBITDA to a loss of approximately $8.5 million-$9.5 million, reflecting continued commercial and research and development investment to expand channels and advance the platform roadmap.

The timing element matters. Management expects revenue growth to be stronger in the second half of 2026 due to procedural seasonality and ramping productivity from commercial investments. That seasonality can make early-year expense intensity look worse before the revenue curve catches up.

For operating leverage to show up, NeuroPace needs multiple gears to engage at once: higher procedure consistency, improving throughput at existing centers, and commercial productivity gains that translate into sustained conversion rather than just pipeline expansion. Management’s narrative depends on those operational steps arriving faster than expense growth over time.

NeuroPace Patient Funnel and Community Referral Risk

NeuroPace is expanding beyond Level 4 comprehensive epilepsy centers while still relying on those centers for concentrated procedure volume. The conversion path is multi-step: patient identification, referral coordination, epilepsy center workflow, and then implant scheduling and execution.

Management is attempting to reduce friction in that chain through targeted sales representative additions, incentive structure updates, and added patient-navigation resources intended to help patients move from identification to implant.

That plan can widen the funnel, but it also raises the execution bar. Community referral relationships can be durable, yet if referral behavior and cross-site coordination do not translate into sustained conversion gains, growth could run below the RNS outlook embedded in guidance.

Image Source: Zacks Investment Research

NPCE IGE Expansion Optionality Not in 2026 Numbers

Idiopathic generalized epilepsy (IGE) remains a meaningful upside lever, but it is not part of management’s 2026 numbers. Management has been explicit that the 2026 guidance excludes any IGE revenue contribution.

Regulatory timing is still fluid. The premarket approval supplement was submitted on Dec. 15, 2025. The FDA paused the review clock to request follow-up information, and management said a midyear determination is still viewed as on track after responding.

Even with approval, monetization may not be immediate. Management has highlighted uncertainty around payer coverage timing and suggested it would update guidance only after gaining visibility into timing and reimbursement dynamics. In other words, approval alone may not translate into near-term revenue until coverage and workflow readiness mature.

NeuroPace Balance Sheet and Cash Burn Snapshot

NeuroPace ended the first quarter with $53.9 million in cash, cash equivalents and short-term investments, down from $61.1 million at the end of the fourth quarter of 2025.

Operating cash use in the first quarter was $5.9 million, improved from $7.5 million a year ago.

In a year when management is still guiding to adjusted EBITDA losses, those figures put the spotlight on runway and funding flexibility through the 2026 investment cycle. Progress on procedure consistency and margin durability can matter not just for valuation, but also for how comfortably the company can sustain commercial build and platform development at the current pace.

NPCE: How Rating Signals Fit the Setup

Zacks Rank is designed as a short-term signal that reflects earnings estimate revisions. NPCE currently carries a Zacks Rank #2 (Buy). It also shows Style Scores of F for Value, A for Growth, F for Momentum and C for VGM. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

A practical framework is to let the fundamental drivers shape your thesis, then use the rating signal to calibrate timing. The fundamentals here center on reimbursement and pricing tailwinds, funnel conversion execution, AI and cloud milestones that aim to improve clinician throughput, and IGE timing uncertainty.

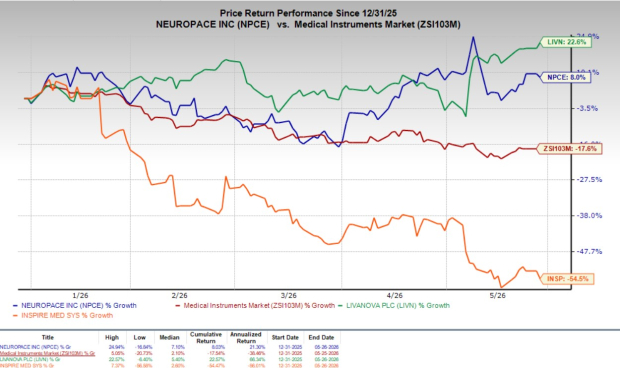

For context, LivaNova PLC LIVN currently has a Zacks Rank #3 (Hold), while Inspire Medical Systems, Inc. INSP carries a Zacks Rank #5 (Strong Sell). Those contrasts can help investors decide whether they want a steadier setup or a higher-variance execution story like NPCE.

In the year-to-date period, shares of NPCE have gained 8% against the industry’s decline of 17.6%. In the same time frame, the company’s peers, shares of LIVN, have jumped 22.6%, while shares of INSP have plunged 54.5%.

Image Source: Zacks Investment Research

NeuroPace: Bull and Bear Checklist for Investors

Bull case confirmation: sustained RNS growth consistent with management’s 21%-23% underlying growth assumption, better conversion and throughput as commercial productivity ramps, and a clean DIXI exit that reduces noise as the company resets to a pure-play RNS base.

Bear case validation: slower community conversion that keeps procedures concentrated and inconsistent, delays in the AI rollout or cloud transition that push out workflow efficiency benefits, and IGE slipping on regulatory timing or payer coverage, leaving growth dependent on the adult focal indication through 2026.

The 2026 debate comes down to whether margin lift and reimbursement support can outweigh the execution demands of scaling the funnel while still investing aggressively. If the operational pieces connect in the back half, the setup improves quickly. If they do not, the loss profile and timing risk can linger longer than investors want.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

LivaNova PLC (LIVN): Free Stock Analysis Report

Inspire Medical Systems, Inc. (INSP): Free Stock Analysis Report

NeuroPace, Inc. (NPCE): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).