NeuroPace, Inc. NPCE is tightening its focus around one thing: the RNS System, a closed-loop implant built for drug-resistant epilepsy. The setup is designed to generate recurring procedure-driven revenues, supported by reimbursement tailwinds, disciplined pricing and a growing prescriber footprint.

The story for investors is less about a single quarter and more about durability. As the company exits a non-core distribution business and leans harder into workflow tools and cloud infrastructure, the debate shifts to how reliably NeuroPace can convert demand into procedures while still operating at a loss in 2026.

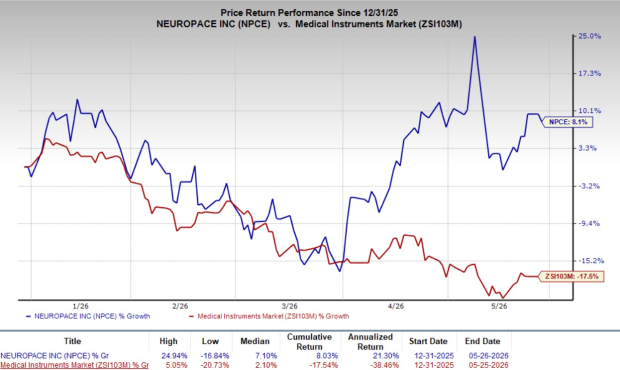

In the year-to-date period, shares of NeuroPace have gained 8.1% against the industry’s 17.5% decline.

Image Source: Zacks Investment Research

NPCE in Epilepsy Neuromodulation

NeuroPace develops and commercializes neuromodulation technology for epilepsy. Its core product, the RNS System, is a brain-responsive implant that monitors intracranial electroencephalography, detects patient-specific abnormal electrical patterns and delivers targeted stimulation intended to help prevent seizures.

The platform includes an implantable neurostimulator placed within the skull, depth and cortical strip leads placed based on clinical need, and a patient remote monitor. It also includes non-implantable tools, including a physician tablet and a patient data management system.

U.S. commercialization began in 2014 following Food and Drug Administration premarket approval in late 2013. As of Dec. 31, 2025, more than 8,000 patients had received the RNS System, and commercial activity remains focused primarily on Level 4 comprehensive epilepsy centers in the United States.

NeuroPace's RNS System and Recurring Procedure Flow

NeuroPace’s economic engine starts with selling RNS System devices to hospitals for initial implants. That same hospital channel also drives the next layer of revenue: replacement implants, which create a repeat procedure cycle over time.

The revenue model is reinforced by the programming and monitoring framework around the implant. The RNS System is programmed by clinicians, and it enables remote review of continuous brain activity data to support ongoing therapy adjustments, linking clinical follow-up with an ecosystem that includes the physician tablet and patient data management.

That is why replacement cadence and center utilization matter. High-utilizing centers can compound value by steadily moving identified patients through implant and follow-up workflows, which supports longer-term revenue durability even when quarter-to-quarter procedure timing swings.

NPCE's Reimbursement Uplift and Pricing Discipline

Unit economics are getting help from two levers that tend to matter most in procedure-heavy medtech: payor rates and pricing. Medicare reimbursement uplifts effective Jan. 1, 2026, increased hospital replacement payments and physician fees, and management has continued low- to mid-single-digit pricing increases.

Those supports are already visible in the margin structure. First-quarter 2026 adjusted gross margin printed at 82.5%, and management reiterated a full-year adjusted gross margin range of 81.5% to 82.5% as mix shifts fully to the core RNS business.

Management attributed underlying year-over-year gross margin gains, excluding one-time items, to manufacturing efficiency and a higher average selling price from pricing conversion. If volumes scale as expected, that combination can help protect profitability per unit even as the company invests in growth.

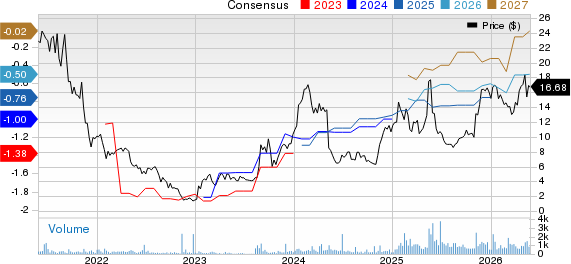

NeuroPace, Inc. Price and Consensus

NeuroPace, Inc. price-consensus-chart | NeuroPace, Inc. Quote

NeuroPace's Growth Signals in Prescribers and Pipeline

NeuroPace has flagged “all-time highs” in active prescribers, accounts, and the patient pipeline. For investors, that combination typically signals broadening awareness plus a deeper bench of potential procedures sitting upstream of implant volume.

Momentum has continued to be driven by Level 4 comprehensive epilepsy centers, which remain the company’s primary commercial focus. At the same time, community referral relationships have begun contributing to funnel expansion and patient identification, creating another path to feed specialty centers.

NPCE presently carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

In the broader neuromodulation landscape, LivaNova PLC LIVN and Medtronic plc MDT also sit in procedure-driven categories where utilization and reimbursement dynamics can shape results. LIVN currently carries a Zacks Rank #3 (Hold), while MDT has a Zacks Rank #4 (Sell).

NPCE DIXI Wind-Down and the Pure-Play Reset

A key strategic change is the exit from DIXI distribution. NeuroPace distributed DIXI Medical stereo electroencephalography products in the United States from 2022 through 2025, but that agreement ended Dec. 31, 2025.

The company expects to complete the remaining inventory return and exit activities by June 30, 2026, and DIXI is expected to be reported as discontinued operations beginning in the second quarter of 2026.

That reset can make comparisons look noisy. Investors should separate underlying RNS trends from transitional accounting and mix effects as the business becomes a cleaner pure-play RNS story.

NeuroPace's AI Suite and Cloud Migration Road Map

NeuroPace is positioning workflow software as a capacity unlock. Management rebranded Seizure ID as the ECoG Assistant and described it as the first step in a broader NeuroPace artificial intelligence suite aimed at helping clinicians analyze intracranial electroencephalography and identify likely electrographic seizures more efficiently.

The company expects ECoG Assistant approval in the second quarter of 2026. In parallel, NeuroPace is migrating the clinician platform to the cloud to improve scalability and speed software deployment.

The intended near-term payoff is practical: lower adoption friction for new physicians and higher throughput at existing high-utilizing centers by reducing workflow friction. If executed well, software can become a stickier layer on top of the implant base.

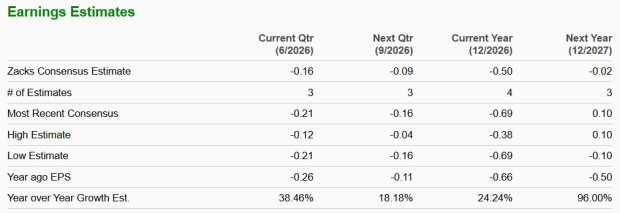

What NPCE's 2026 Guidance Says About Trajectory

Management raised full-year 2026 total revenue guidance to $99 million to $101 million on a continuing-operations basis, up from $98 million to $100 million previously.

Embedded in that outlook is an assumption of 21% to 23% underlying growth in core RNS revenue, still excluding any contribution from idiopathic generalized epilepsy.

Investors should also focus on cadence. Management expects seasonality to favor the second half of 2026, which can amplify quarterly variability even when the full-year setup remains intact.

Image Source: Zacks Investment Research

NeuroPace's Key Risks and What to Watch Next

The watch list starts with losses. Adjusted EBITDA is guided to a loss of roughly $8.5 million to $9.5 million in 2026, even as the company continues commercial and research and development investments.

Procedure timing is another swing factor. Revenue growth is expected to be stronger in the second half, which raises the risk that quarter-to-quarter implant volatility can distort near-term sentiment.

Execution around software and community conversion also matters. Any delay in ECoG Assistant clearance, cloud implementation, or field adoption could push out workflow benefits, while slower community funnel conversion could leave growth overly dependent on Level 4 centers. The single biggest swing factor remains idiopathic generalized epilepsy progress: the premarket approval supplement was submitted on Dec. 15, 2025, and remains under the FDA review, but timing and payer coverage dynamics can still reshape the opportunity without a clear assumed schedule.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Medtronic PLC (MDT): Free Stock Analysis Report

LivaNova PLC (LIVN): Free Stock Analysis Report

NeuroPace, Inc. (NPCE): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).