Biogen BIIB stock has risen 11.5% in 2026 so far. A key reason for the stock price increase was Biogen’s robust first-quarter 2026 results, as it beat estimates for both earnings and sales. While earnings rose 18%, revenues declined 2% on a constant currency basis as lower sales of key drugs, Tecfidera and Spinraza, were partially offset by higher revenues from new drugs, Skyclarys, Qalsody and Zurzuvae. Investor confidence seems to be on the rise as Biogen’s newer products are beginning to offset declines in its legacy multiple sclerosis (MS) franchise.

After several difficult years marked by declining MS revenues, concerns about Alzheimer’s commercialization and pipeline skepticism, sentiment has improved due to stronger earnings, a more diversified growth portfolio, major M&A activity and growing confidence in late-stage pipeline assets. Investors are also encouraged by the company’s multiyear turnaround gaining traction.

Let’s understand Biogen’s strengths and weaknesses to better analyze how to play the stock in such a scenario.

Generic Pressure on BIIB’s MS Drugs & Spinraza

Biogen’s global MS revenues declined 3% on a constant-currency basis in the first quarter, with Tecfidera down 47% and Tysabri up 15.7%. MS sales are declining due to generic competition for Tecfidera globally, biosimilar competition for Tysabri in Europe and rising competitive pressure in the MS market.

Multiple generic versions of Tecfidera have now been launched in North America, Brazil and certain European countries. In November 2025, the Technical Boards of Appeal of the European Patent Office revoked a Tecfidera patent, which was one of the main pieces of protection Biogen used to delay generic competition in Europe. The revocation opened the door for earlier generic launches throughout Europe.

Regulatory applications seeking approval for a biosimilar referencing Tysabri have been approved in both the United States and Europe. A Tysabri biosimilar is now available in some European countries, with a biosimilar entry in the United States expected soon.

In 2026, Biogen expects revenues for MS products, excluding Vumerity, to decline by a mid-teen percentage versus 2025 due to increased competitive pressure on the ex-U.S. MS business, particularly accelerating generic competition for Tecfidera in Europe.

Spinraza’s sales are also declining due to lower demand. Sales of Spinraza declined around 12% in the first quarter. Nonetheless, a higher dose regimen of Spinraza, which reduces the dosing frequency, was recently approved in the United States, Japan and the EU. The high-dose Spinraza improves Biogen’s competitiveness in a highly competitive area.

BIIB’s New Drug Contributing to Top-Line Growth: Is it Enough?

Amid declining demand for MS drugs and Spinraza, Biogen believes its new products, Leqembi (partnered with Eisai) for Alzheimer’s disease, Skyclarys for Friedreich’s ataxia and Zurzuvae for depression, have the potential to revive growth.

Leqembi/lecanemab gained approval for early Alzheimer’s disease in the United States in 2023. Though the Leqembi launch was slow, it picked up in 2024 and 2025. Leqembi has also been launched in Japan, China, the EU and some other countries. Leqembi commands over 60% of the anti-amyloid therapy market share in the United States.

A less frequent maintenance intravenous dosing version of Leqembi was approved by the FDA in January 2025. A subcutaneous autoinjector for maintenance dosing called Leqembi Iqlik was launched in October 2025, while a supplemental filing seeking approval of the Leqembi Iqlik subcutaneous autoinjector for initiation dosing has been granted priority review by the FDA, with a decision expected in August. Biogen and Eisai believe that the introduction of blood-based diagnostics (which can help earlier detection of Alzheimer’s) and the subcutaneous autoinjector for maintenance and initiation should drive Leqembi’s growth from 2027 onward.

Other new products, Qalsody, for amyotrophic lateral sclerosis, Biogen and partner Supernus Pharmaceuticals’ SUPN Zurzuvae for treating postpartum depression (PPD) and Skyclarys for treating Friedreich’s ataxia (added from 2023’s acquisition of Reata Pharmaceuticals) are also seeing strong demand trends in the United States.

Biogen’s growth products (Skyclarys, Qalsody, Zurzuvae, Vumerity and Spinraza plus Alzheimer’s revenues from the Leqembi collaboration) generated sales of $851 million in the first quarter, rising 12% year over year.

However, though all these new drugs are showing signs of growth, they are not yet generating enough sales to fully offset the declining revenues of MS drugs and Spinraza.

Robust M&A Activity Has Strengthened BIIB’s R&D Pipeline

With competition in the MS market intensifying, Biogen has successfully diversified its pipeline across areas like Alzheimer's, immunology and rare disease. Biogen has strengthened its mid-to-late-stage neurology and immunology pipeline with M&A deals. Among some recent deals, in April 2026, Biogen closed its acquisition of Apellis Pharmaceuticals, adding the commercialized medicines Empaveli and Syfovre for immune-mediated retinal disease and nephrology to its commercial portfolio. Biogen expects the Apellis acquisition to be accretive to earnings in 2027 and boost the adjusted EPS growth rate over the remainder of the decade.

Also, in May, Biogen acquired exclusive rights to felzartamab in China from TJ Biopharma. With this deal, Biogen now holds exclusive worldwide rights to felzartamab, which was earlier acquired from the 2024 HI-Bio acquisition. Felzartamab is a key pipeline candidate for Biogen, currently being evaluated in phase III studies for multiple immune-mediated diseases.

Several data readouts are expected over the next 18 months, including systemic lupus erythematosus and cutaneous lupus erythematosus data from phase III studies of litifilimab, as well as readouts from the first phase III study of felzartamab in antibody-mediated rejection and the phase III study for zorevunersen in Dravet syndrome.

However, regular pipeline setbacks are a concern. Among some recent setbacks, in May 2026, Biogen and partner Denali Therapeutics DNLI discontinued the development of BIIB122 in idiopathic Parkinson’s disease as a mid-stage study failed to meet its primary or secondary endpoints. The drug failed to slow the progression of Parkinson’s disease in patients.

BIIB’s Price, Valuation & Estimates

Biogen’s shares have risen 51.3% over the past year compared with an increase of 25.8% for the industry. The stock has also outperformed the sector and S&P 500 index, as seen in the chart below.

BIIB Stock Outperforms Industry, Sector & S&P 500

From a valuation standpoint, Biogen is reasonably priced. Going by the price/earnings ratio, the company’s shares currently trade at 12.93 forward earnings, which is lower than 17.42 for the industry. The stock is also trading below its five-year mean of 13.27.

BIIB Stock Valuation

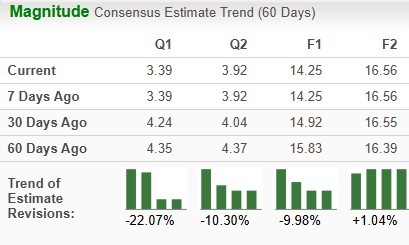

The Zacks Consensus Estimate for earnings has declined from $15.83 per share to $14.25 per share for 2026 over the past 60 days. For 2027, the consensus mark for earnings has increased from $16.39 to $16.56 per share over the same time frame.

BIIB’s Estimate Movement

Stay Invested in BIIB Stock

After declining for several years, Biogen’s revenues have somewhat stabilized since 2024 due to contributions from newer products and pipeline progress. However, its newer drugs, Leqembi, Skyclarys, Qalsody and Zurzuvae are currently insufficient to offset the near-term top-line decline of the MS franchise. Other risks also remain. MS drug sales continue to decline because of generic competition. Leqembi’s long-term commercial trajectory is not fully proven, and several pipeline programs still face clinical and regulatory uncertainty.

However, the Apellis deal could prove transformative for Biogen because it immediately adds commercial products and strengthens Biogen’s position in immunology and nephrology. Biogen expects the acquisition to boost its near-term growth and help offset the near-term top-line decline of the MS franchise.

Biogen’s rising price, reasonable valuation, an improving pipeline and better sales prospects of new drugs are good enough reasons for those who own this Zacks Rank #3 (Hold) stock to stay invested for now. Though estimates for 2026 have declined, it is due to costs related to M&A deals like Apellis, which eventually benefit the company in the long term. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Biogen Inc. (BIIB): Free Stock Analysis Report

Supernus Pharmaceuticals, Inc. (SUPN): Free Stock Analysis Report

Denali Therapeutics Inc. (DNLI): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).