Guidewire Software, Inc. GWRE is slated to report third-quarter fiscal 2026 results on June 4.

Management expects revenues to be between $352 million and $358 million. The Zacks Consensus Estimate is pinned at $356 million, up 21.3% from the same quarter last year.

The consensus estimate for the bottom line is pinned at 79 cents, unchanged over the past 60 days. GWRE reported earnings of 88 cents per share in the year-ago quarter.

The company’s earnings beat the Zacks Consensus Estimate in each of the trailing four quarters, with the average surprise being 44.68%.

Image Source: Zacks Investment Research

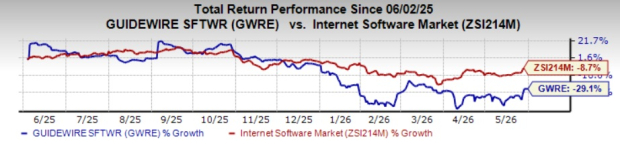

Shares of GWRE have lost 29.1% in the past year compared with the Internet-Software industry’s decline of 8.7%.

Factors at Play for GWRE’s Q3 Results

Guidewire is benefiting from strong demand for cloud-based core insurance software as property and casualty insurers accelerate modernization efforts. In the second quarter of fiscal 2026, the company’s ARR grew 22% year over year to $1.121 billion, supported by robust InsuranceSuite Cloud adoption, expanding customer commitments and increasing demand for cloud migrations. For the third quarter of fiscal 2026, Guidewire expects ending ARR to be between $1.144 billion and $1.150 billion. Management highlighted that generative AI is becoming a major catalyst for modernization, as insurers require modern core systems, real-time data access and cloud infrastructure to deploy AI-driven workflows effectively.

The company is benefiting from strong demand for cloud-based insurance software modernization, which continues to drive large customer wins and expansions. In the second quarter, Guidewire closed 15 InsuranceSuite Cloud deals and two InsuranceNow deals, including new customer additions, migrations and expansion agreements. The company is witnessing larger transactions, longer contract durations and rising commitments from Tier 1 and Tier 2 insurers. Management noted that fully ramped ARR growth continues to outpace reported ARR growth, supported by healthy demand across North America, Europe and the Asia-Pacific.

Guidewire is also gaining from the growing adoption of its newer products and AI-driven offerings. In the second quarter, Guidewire signed its first PricingCenter deal, closed 25 transactions involving data and analytics solutions, and secured nine ProNavigator AI deals. On the last earnings call, management stated that AI is helping accelerate customer demand, improve implementation velocity and drive additional product adoption opportunities across its customer base.

The company is also benefiting from improving cloud operating efficiency, which continues to support margin expansion. In the second quarter of fiscal 2026, non-GAAP gross margin increased to 67.6%, driven by stronger subscription and support margins. Reflecting this momentum, Guidewire raised its fiscal 2026 gross margin outlook to approximately 67%. For the fiscal third quarter, management expects subscription and support gross margins of around 74%, total gross margins of about 67% and non-GAAP operating income in the range of $59-$65 million.

We expect non-GAAP gross margin subscription and support to be 73.1% while our estimate for non-GAAP operating income is pegged at $61.1 million, up 32.7% year over year.

Guidewire Software, Inc. Price and EPS Surprise

Guidewire Software, Inc. price-eps-surprise | Guidewire Software, Inc. Quote

However, investors should monitor the timing of ARR conversion from backlog. Management stated that ARR realization is expected to be more heavily weighted toward the fiscal fourth quarter than the third quarter, which could limit near-term upside despite strong underlying demand.

On the last earnings call, management also highlighted that some of the recent growth benefited from stronger-than-expected true-up activity and large deal volume. Management expects true-up activity to moderate from prior highs over time, while newer products, such as PricingCenter, remain in relatively long sales cycles that may delay revenue contribution. Additionally, the company plans to increase investments and expenses to support growth initiatives, which might have negatively impacted the company’s third-quarter performance.

What Our Model Says About GWRE Stock

Our proven model does not predict an earnings beat for GWRE this time around. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the odds of an earnings beat. This is not the case here.

GWRE has an Earnings ESP of 0.00% and a Zacks Rank #2. You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

Stocks to Consider

Here are a few companies worth considering, as our model indicates that these possess the right combination to exceed earnings expectations in their upcoming releases:

Dollar General Corporation DG currently has an Earnings ESP of +0.82% and a Zacks Rank #3 at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for revenues and earnings is pegged at $10.82 billion and $1.89 per share, respectively. Dollar General is slated to report first-quarter 2026 results on June 2.

Five Below, Inc. FIVE has an Earnings ESP of +7.33% and a Zacks Rank #2 at present.

The Zacks Consensus Estimate for revenues and earnings is pegged at $1.20 billion and $1.70 per share, respectively. Five Below is slated to report first-quarter fiscal 2026 results on June 3.

Ciena Corporation CIEN currently has an Earnings ESP of +0.99% and a Zacks Rank #1.

The Zacks Consensus Estimate for revenues and earnings is pegged at $1.50 billion and $1.46 per share, respectively. CIEN is scheduled to report second-quarter fiscal 2026 results on June 4.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power .

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Dollar General Corporation (DG): Free Stock Analysis Report

Ciena Corporation (CIEN): Free Stock Analysis Report

Guidewire Software, Inc. (GWRE): Free Stock Analysis Report

Five Below, Inc. (FIVE): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).