Costco Wholesale Corporation’s COST comparable sales growth of 9.8% in the third quarter of fiscal 2026 has immediately grabbed investors’ attention, given the standout figure in today’s retail environment. The expansion was propelled by a 2.2% lift from fuel price inflation and a 1% tailwind from foreign exchange fluctuations. While these macroeconomic factors boosted reported comparable sales, the underlying performance suggests demand remained broad-based across the business.

Adjusted comparable sales, which exclude gasoline and foreign exchange impacts, rose 6.6%. The growth was supported by a healthy balance of traffic and spending. Comparable traffic increased 2.4%, indicating that more members visited Costco warehouses, while adjusted ticket growth reached 4.2%, reflecting larger baskets and stronger purchasing activity.

Management noted that the company has continued to generate adjusted comparable sales growth in the 6%-7% range despite lapping unusually strong categories from prior periods, including gift card promotions and elevated gold sales. The ability to maintain that pace suggests demand remains resilient.

Regionally, comparable sales increased 9.4% in the United States, 10.7% in Canada and 11.2% in Other International markets. Excluding gasoline and foreign exchange impacts, comparable sales rose 6.8%, 6.2%, and 5.9%, respectively, pointing to healthy demand across all major operating regions.

Membership dynamics support this trend. Costco ended the quarter with 82.9 million paid memberships, up 4.1% from the prior-year period, while total cardholders increased 4% to 148.5 million. Executive memberships rose 9.6% year over year to 41.2 million, reflecting continued member engagement and upgrades. Executive members accounted for approximately 75% of worldwide sales.

Costco’s comparable sales growth was more than a headline number. It reflected a business generating growth through increased member visits, larger baskets and stable demand across markets.

How Costco Compares With Walmart and Target

Among Costco’s major competitors, Walmart Inc. WMT and Target Corporation TGT also reported healthy comparable-sales growth in their latest quarters.

Walmart posted U.S. comparable sales growth of 4.1%, driven by higher customer transactions, increased unit volumes and strong e-commerce performance. Walmart continued to gain market share across income groups while benefiting from growth in advertising, marketplace sales and Walmart+ membership revenues. Walmart’s results reflected steady demand for both grocery and general merchandise offerings.

Meanwhile, Target delivered comparable sales growth of 5.6%, supported by a 4.4% increase in traffic and strength across both stores and digital channels. Target reported sales growth in all six core merchandise categories, with broad-based demand across guest demographics. Target also highlighted momentum in beauty, food and wellness categories. As Target executes its merchandising and store experience initiatives, the retailer remains focused on driving sustainable long-term growth.

What the Latest Metrics Say About Costco

Costco has seen its shares tumble 4.6% over the past three months compared with the industry’s decline of 2.2%.

Image Source: Zacks Investment Research

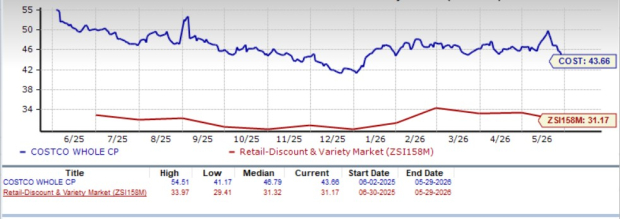

From a valuation standpoint, Costco's forward 12-month price-to-earnings ratio stands at 43.66, higher than the industry’s ratio of 31.17. However, it is trading below its 12-month median level of 46.79, indicating some moderation in valuation despite sustained investor confidence in the stock.

Image Source: Zacks Investment Research

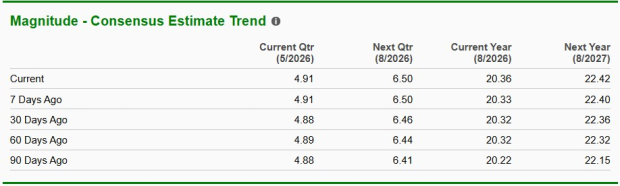

The Zacks Consensus Estimate for Costco’s current financial-year sales and earnings per share implies year-over-year growth of 9.2% and 13.2%, respectively. For the next fiscal year, the consensus estimate indicates a 7.7% rise in sales and 10.1% growth in earnings.

The consensus estimate for earnings per share for the current and next fiscal year has increased by 3 cents and 2 cents to $20.36 and $22.42, respectively.

Image Source: Zacks Investment Research

Costco currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power .

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Target Corporation (TGT): Free Stock Analysis Report

Walmart Inc. (WMT): Free Stock Analysis Report

Costco Wholesale Corporation (COST): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).