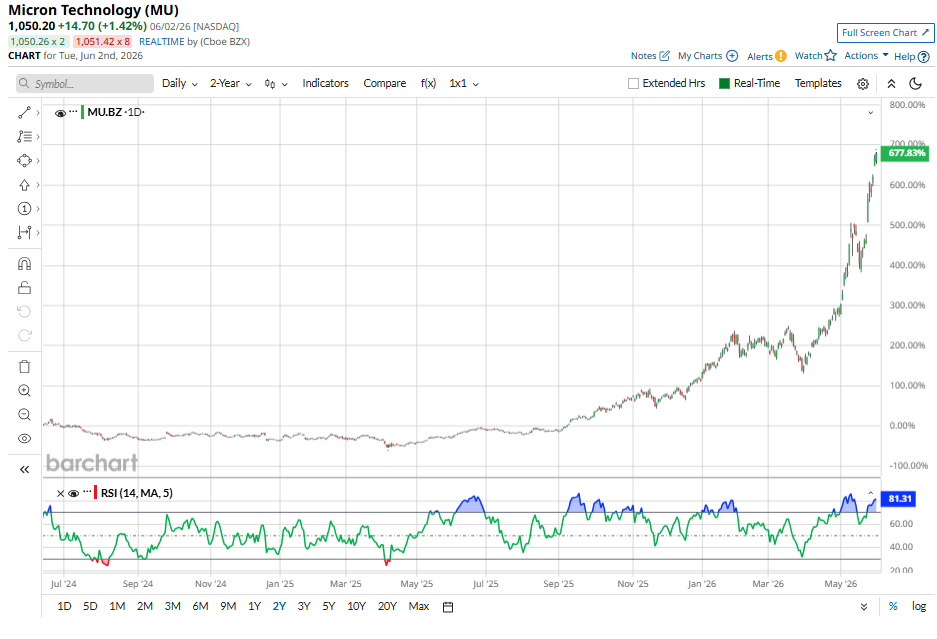

Micron Technology (MU) is one of the biggest winners from the artificial intelligence (AI) infrastructure boom. Thanks to the surging demand for AI infrastructure, the memory-chip maker has delivered eye-popping gains, climbing 965.6% over the past year and 266.6% year-to-date (YTD).

Despite this remarkable rally, analysts are bullish about Micron's prospects, and the run in MU stock may not be over. Strong AI-driven demand, favorable industry dynamics, improving profitability, and a compelling valuation indicate further upside for the stock over the next 12 months.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Into Micron Stock’s Rally

The rapid expansion of AI is creating massive demand for high-bandwidth memory (HBM) and high-performance storage to train and run increasingly complex workloads. This is working in Micron’s favor.

The company supplies ultra-fast, high-capacity memory to hyperscale data centers that power large language models, cloud AI platforms, and enterprise AI applications. As AI adoption accelerates, demand for Micron's memory products continues to rise.

At the same time, industry-wide supply conditions are supporting its growth. Notably, the global memory supply remains tight, driving prices higher as demand is accelerating. This combination has boosted Micron's margins, strengthened earnings growth, and increased investor confidence in the company's long-term outlook.

www.barchart.com

www.barchart.com MU Stock: Explosive Growth and Attractive Valuation Indicate Upside

Micron's stock has already delivered impressive gains, but the company's explosive earnings growth and surprisingly modest valuation suggest the rally will likely sustain. The rapid expansion of AI servers, hyperscale cloud platforms, and advanced data centers is creating significant demand for high-performance memory. Technologies such as HBM, advanced DRAM, and enterprise solid-state drives have become critical components of modern AI systems.

With AI infrastructure investments accelerating worldwide and compute architectures becoming more memory-intensive, Micron still has a massive opportunity for growth. At the same time, memory supply remains relatively constrained, indicating a favorable pricing environment that enables Micron to significantly expand revenue and profitability.

Micron guided for a solid quarterly performance. Management expects third-quarter revenue of $33.5 billion, representing a sequential increase of roughly 40% and nearly 300% year-over-year (YOY) growth. Profitability is improving even faster than revenue. Micron expects gross margins to reach approximately 81% in the third quarter, up from 39% a year ago and building on the already impressive 75% gross margin reported in the second quarter.

Earnings are projected to jump to roughly $19.15 per share, up from $1.91 per share in the same quarter last year. Higher memory prices, manufacturing efficiencies, and a growing mix of premium AI-focused products are driving this earnings explosion.

Adding to Micron’s investment appeal is its focus on adding stability and visibility to its earnings. Historically, memory-chip manufacturers have faced highly cyclical demand and volatile pricing, making earnings difficult to predict.

However, the AI era may be changing that dynamic. The world's largest technology companies are committing hundreds of billions of dollars to long-term AI infrastructure projects. In response, Micron is pursuing multi-year supply agreements that provide greater visibility into future demand. These strategic customer agreements will bring stronger pricing power, more stable revenue streams, and structurally higher margins.

Besides Micron’s solid growth and focus on strategic customer agreements, its valuation supports its bull case. Shares trade at 16.56 times forward earnings, a multiple that appears modest given the company's solid earnings growth outlook. Analysts expect Micron’s earnings to surge by more than 663% in fiscal 2026, followed by another solid growth rate of 74.5% in fiscal 2027.

With Micron expected to deliver solid growth and trading at a low-teens earnings multiple, the risk-reward profile is difficult to ignore.

How High Could MU Stock Rise?

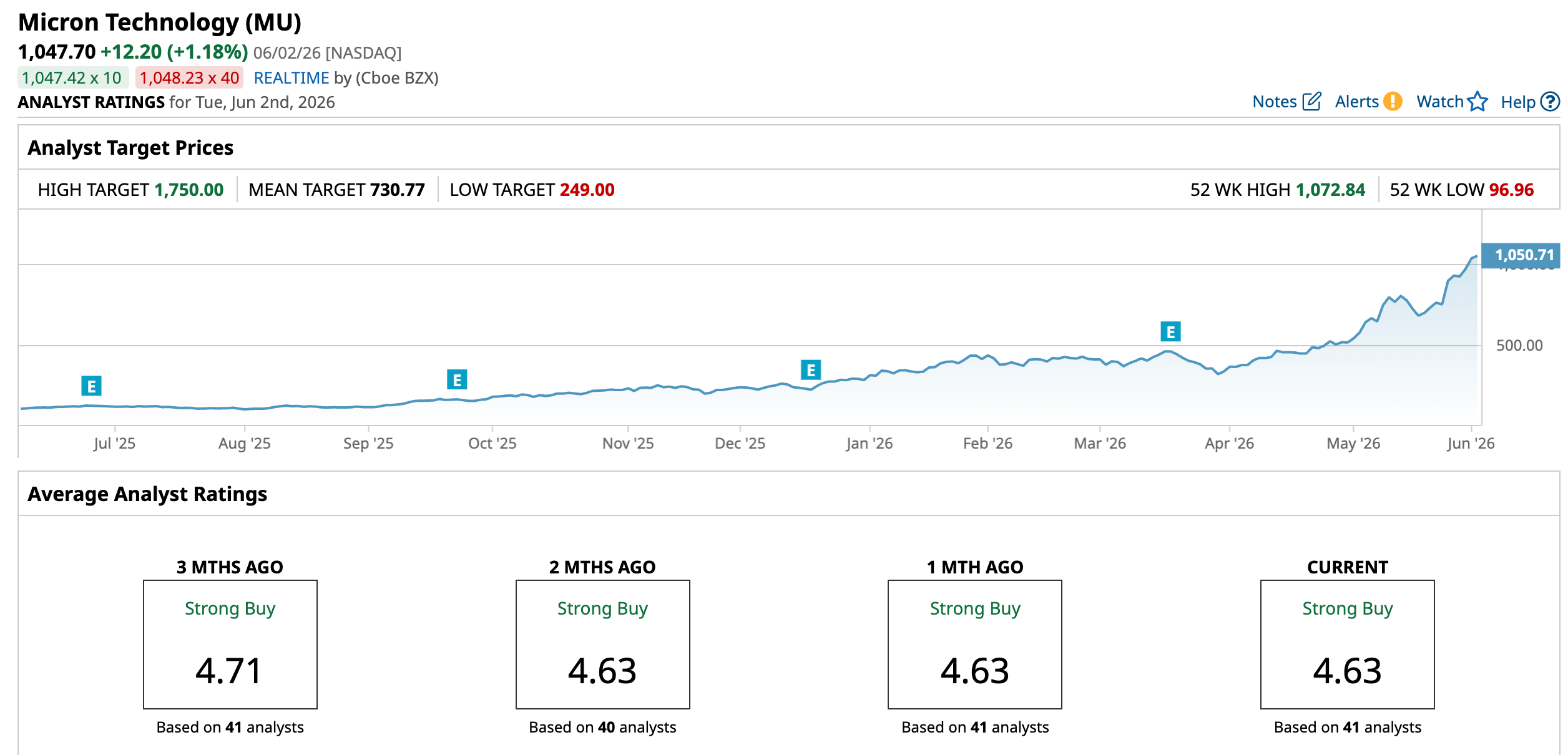

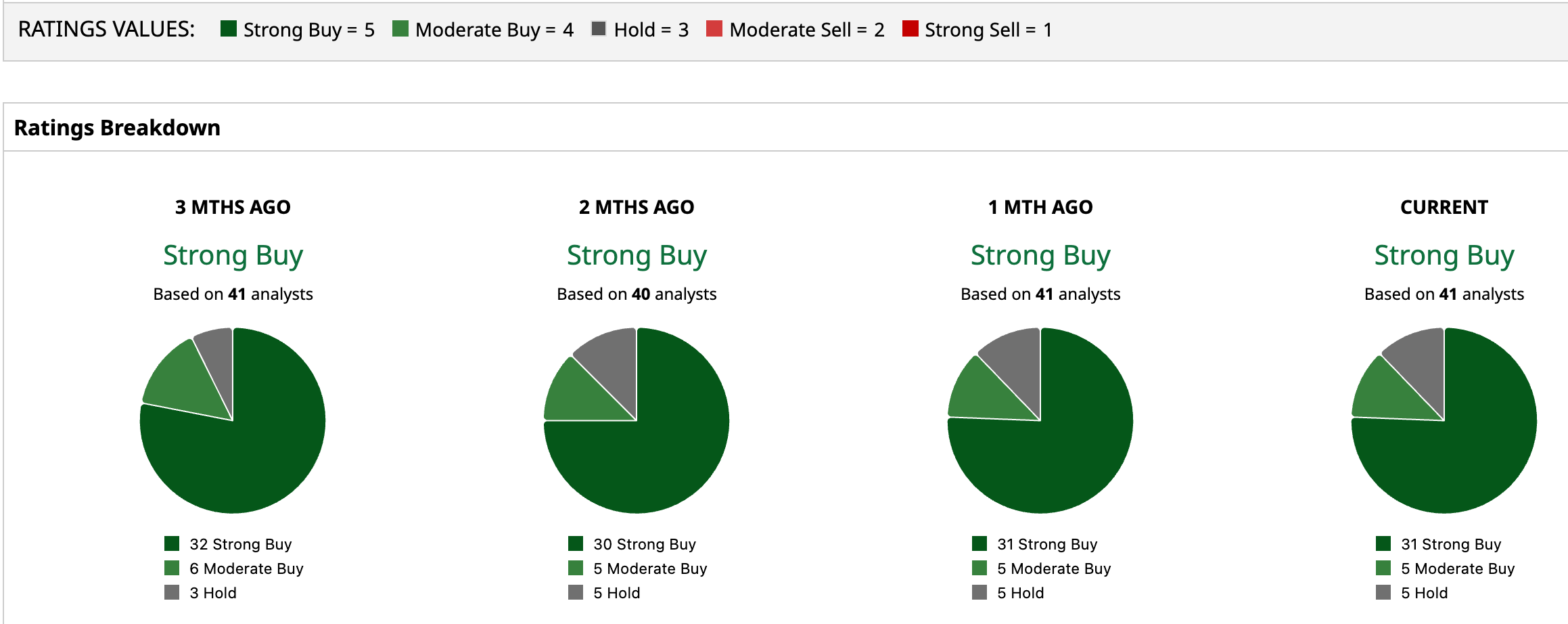

Analysts continue to back Micron stock and maintain a “Strong Buy” consensus rating. Meanwhile, the highest price target for MU stock is $1,750, implying 67% upside potential over the next 12 months.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Even If Eli Lilly Stock Continues to Shine, Stay Away from This Pharmaceutical ETF Micron Stock Could Still Have Nearly 70% Upside Potential Left in Its Tank Nvidia Launches AI Chip for Laptops. Count NVDA Stock Out at Your Own Peril. Greg Abel's Big Bet: Berkshire to Buy Taylor Morrison Homes in $6.8 Billion Deal