For a while now, the PC industry has been waiting for its next big moment. Faster processors and better battery life have helped, but they have not exactly sparked a major upgrade cycle. Microsoft Corporation (MSFT) and Nvidia Corporation (NVDA) seem to think artificial intelligence (AI) could change that.

Soon, the two companies are expected to pull back the curtain on the first Windows PCs powered by Nvidia chips as the main processor. The reveal is set to happen at Computex in Taiwan and Microsoft’s Build conference in San Francisco. These machines are expected to come not only from Microsoft’s Surface lineup but also from other PC manufacturers.

More Yield, Less Trap: Sign up free to get Barchart’s daily Dividend Investor newsletter straight to your inbox.

The hints have already started flying. Nvidia recently teased “a new era of PC,” while Microsoft’s Windows chief Pavan Davuluri alluded to something new coming in a post. The excitement is not just about hardware, either. Microsoft is reportedly preparing software that would allow AI agents to run tasks directly on Windows PCs, bringing more AI capabilities onto the device itself. If that vision catches on, it could give the PC market a fresh growth story and open another door for Microsoft’s AI ambitions.

Investors appear to be paying attention. MSFT stock recently climbed to a three-month high before easing slightly on June 2. If the new AI-powered PCs can spark a fresh upgrade cycle, investors may have another reason to stay bullish on the software giant.

About Microsoft Stock

Microsoft hardly needs an introduction. A core member of the Magnificent Seven, it has grown from a scrappy software pioneer into a technology titan, boasting a market capitalization of $3.4 trillion. Windows still commands more than 70% of the global PC operating system market, but that is just the starting point.

Today, Microsoft’s influence stretches across Azure cloud computing, Microsoft 365 productivity tools, developer platforms, enterprise solutions, and gaming. What truly defines the company is its evolution – from boxed software to subscription ecosystems, from on-premise servers to AI-powered cloud platforms. Whether in corporate boardrooms, university classrooms, or everyday households, Microsoft has woven itself into the digital fabric of modern life – steady, scalable, and constantly reinventing itself.

MSFT stock’s price performance over the longer term has been remarkable. Over the past decade, shares have climbed roughly 800%, turning the software giant into one of Wall Street’s biggest winners as it rode the cloud computing boom and, more recently, the AI wave. The shorter-term picture, however, has been far less smooth. Over the past 52 weeks, MSFT is down 4.38%, while the stock lost 9.85% over the last six months. Earlier this year, investors grew uneasy about Microsoft’s aggressive AI spending plans.

Following its Q3 report in April, MSFT stock slipped as the market questioned whether Microsoft’s massive AI spending would generate returns quickly enough, especially amid rising competition and uncertainty surrounding key AI partners. Management projects Q4 capital expenditures to reach $40 billion, with calendar 2026 capex projected at $190 billion.

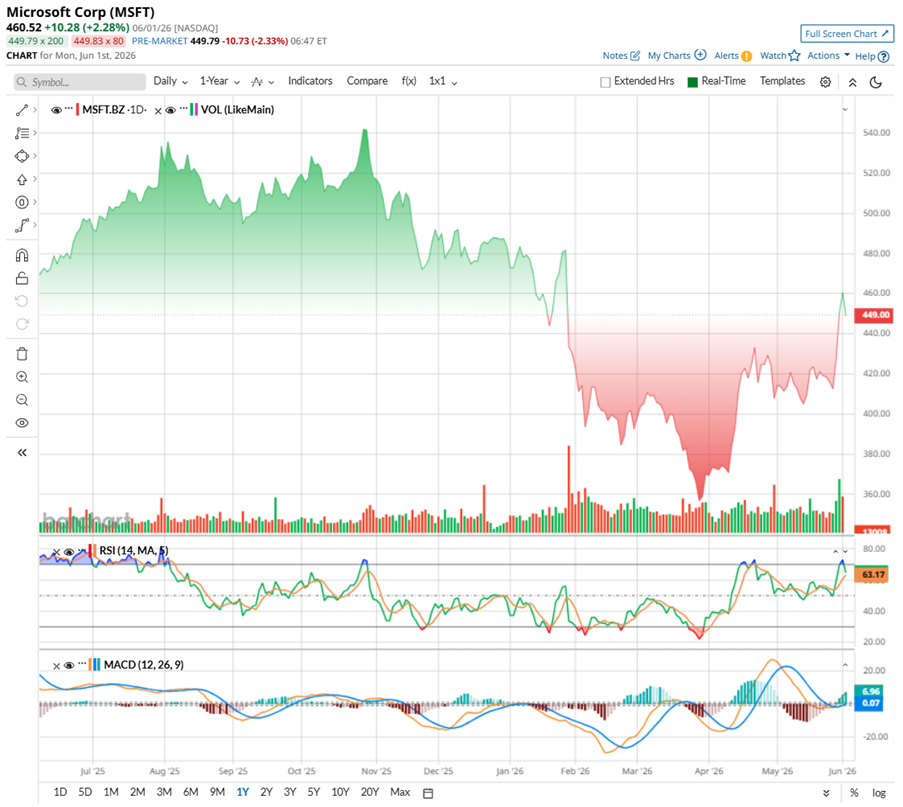

Yet, over the past three months, Microsoft’s shares have rallied 10.83%, touching a three-month high of $466.32 on June 1. The move has been fueled by improving sentiment around AI monetization and a series of bullish analyst calls. Just as importantly, the stock recently climbed back above its 200-day moving average – for the first time since January – a level many traders view as a sign that long-term momentum is turning positive again. Evercore ISI’s Kirk Materne called the recent software rally “durable,” suggesting investors may be looking beyond near-term AI spending concerns.

Technically, the picture remains steady but not without risks. Trading volume has been mixed, with recent sessions showing heavy selling activity. The 14-day RSI briefly entered overbought territory before easing back to 60.15, indicating momentum remains strong but no longer stretched. Meanwhile, the MACD oscillator shows bullishness, with the MACD line holding above the signal line and the histogram staying in positive territory, signaling that buyers still have the upper hand for now.

www.barchart.com

www.barchart.com Microsoft is not exactly a bargain-bin stock these days. The stock trades at 26.86 times forward adjusted earnings and 10.4 times forward sales, both above the broader tech sector. But that’s only part of the story. Compared with MSFT’s own historical valuation levels, the stock is actually trading a bit below where investors have often valued it in the past. That’s because investors are buying a business that sits at the center of cloud computing, enterprise software, and now the AI boom. With revenue growing and cash continuing to pile up, many see the premium price tag as justified.

Then there’s the shareholder-friendly side of the story. Microsoft has been raising its dividend since launching one in 2003. The company is scheduled to pay $0.91 per share on June 11, which brings its annualized payout to $3.64 per share. While the forward yield sits at a modest 0.79%, the payout ratio is only about 22%, giving Microsoft plenty of flexibility to keep increasing dividends for years to come. After more than two decades of steady dividend growth, Microsoft is steadily moving closer to earning the coveted ‘Dividend Aristocrat’ status.

Microsoft Beats Q3 Estimates

Microsoft’s earnings report for third quarter of fiscal 2026, released on April 29, showed that the company’s AI and cloud machine is solid. The company delivered revenue of $82.9 billion, up 18.3% year-over-year (YOY), while EPS jumped 23.4% annually to $4.27 – both surpassing analysts’ projections. Management called it a record quarter, and the growth was largely powered by the businesses at the center of today’s AI boom.

Microsoft Cloud generated $54.5 billion in revenue, climbing 29% YOY. Meanwhile, the company’s AI business continued to gain momentum, with its annual revenue run rate surpassing $37 billion after growing an impressive 123% annually.

Of course, building the infrastructure behind that growth is expensive. Microsoft has been spending aggressively to expand its AI footprint, and that showed up in the numbers. Gross margin edged down to 68% as the company invested heavily in data centers and absorbed higher costs from increased AI usage. Gains in efficiency across Azure and Microsoft 365 Commercial helped offset some of that pressure.

The spending was substantial. Capital expenditures, including finance leases, totaled $31.9 billion during the quarter. Even so, Microsoft’s balance sheet remained strong, with cash and cash equivalents rising to $32.1 billion at the end of March.

Looking ahead, management expects Q4 revenue between $86.7 billion and $87.8 billion, representing growth of roughly 13% to 15%. Microsoft also plans to keep spending aggressively, with additional AI capacity coming online and capex expected to remain elevated as demand for AI services continues to surge.

Meanwhile, analysts tracking Microsoft anticipate the company’s Q4 EPS to grow 15.3% YOY to $4.21. For fiscal 2026, EPS is expected to jump 22.9% annually to $16.76 per share, and then rise by another 15% YOY to $19.28 per share in fiscal 2027.

What Do Analysts Expect for Microsoft Stock?

Microsoft has been spending billions to build the backbone of the AI boom, and Morgan Stanley believes Wall Street still may not fully appreciate how big the payoff could eventually be. Analyst Keith Weiss maintained an “Overweight” rating on the stock and set a $650 price target, arguing that Microsoft’s expanding data center footprint could support far more revenue than current forecasts suggest.

While revenue generated per megawatt of capacity is expected to decline over the next few years, Weiss views that as a sign that Microsoft is building AI infrastructure ahead of demand rather than struggling to monetize it. He estimates the company's data center capacity could quadruple from about 5 gigawatts in fiscal 2024 to roughly 20 gigawatts by fiscal 2028. If AI adoption accelerates and products like Copilot, GitHub, Dynamics, and Microsoft 365 gain traction, Weiss believes Microsoft's existing infrastructure could unlock significant upside without requiring a matching jump in future spending.

Citizens analyst Patrick Walravens sees even more reasons to stay optimistic. He reiterated a “Market Outperform” rating on MSFT and kept his $550 price target, pointing to the company’s growing ambitions across the AI landscape. Beyond its cloud dominance, Microsoft is developing its own frontier AI models while also partnering with Nvidia on RTX Spark, a move that could strengthen its position in on-device AI.

Under CEO Satya Nadella’s vision of AI sovereignty, Microsoft is building a complete AI ecosystem spanning AI agents, an agent platform, and the cloud infrastructure powering them all. Walravens believes that strategy positions the company to tap into a massive $5.1 trillion market opportunity by 2030.

He also highlighted Microsoft’s strong execution, with revenue expected to grow 17% in fiscal 2026 and return on equity holding at an impressive 34%. While questions remain about Microsoft’s ability to build leading AI models independently and reduce reliance on third-party models, Walravens believes the company’s leadership and scale keep it firmly in the driver’s seat.

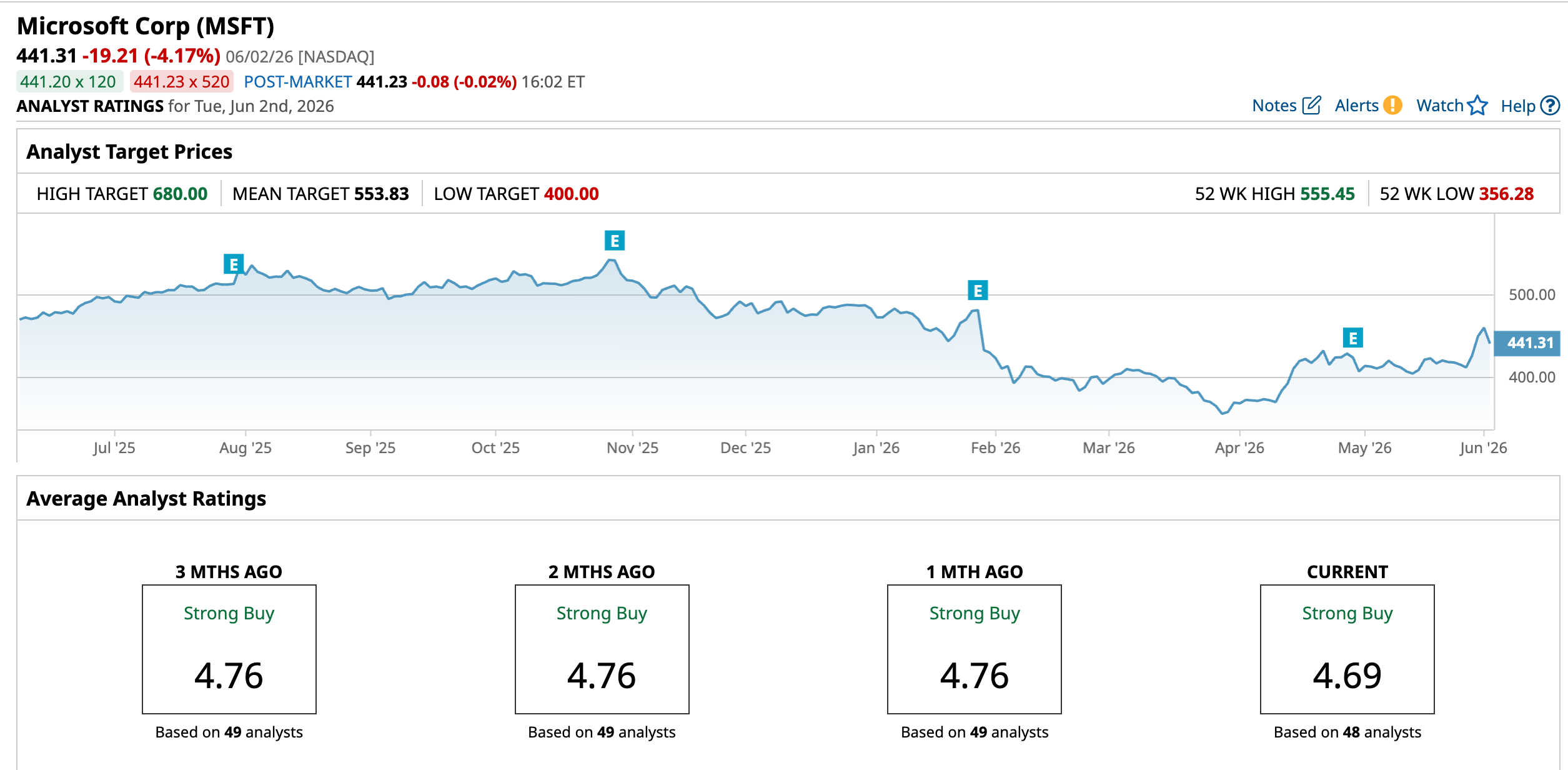

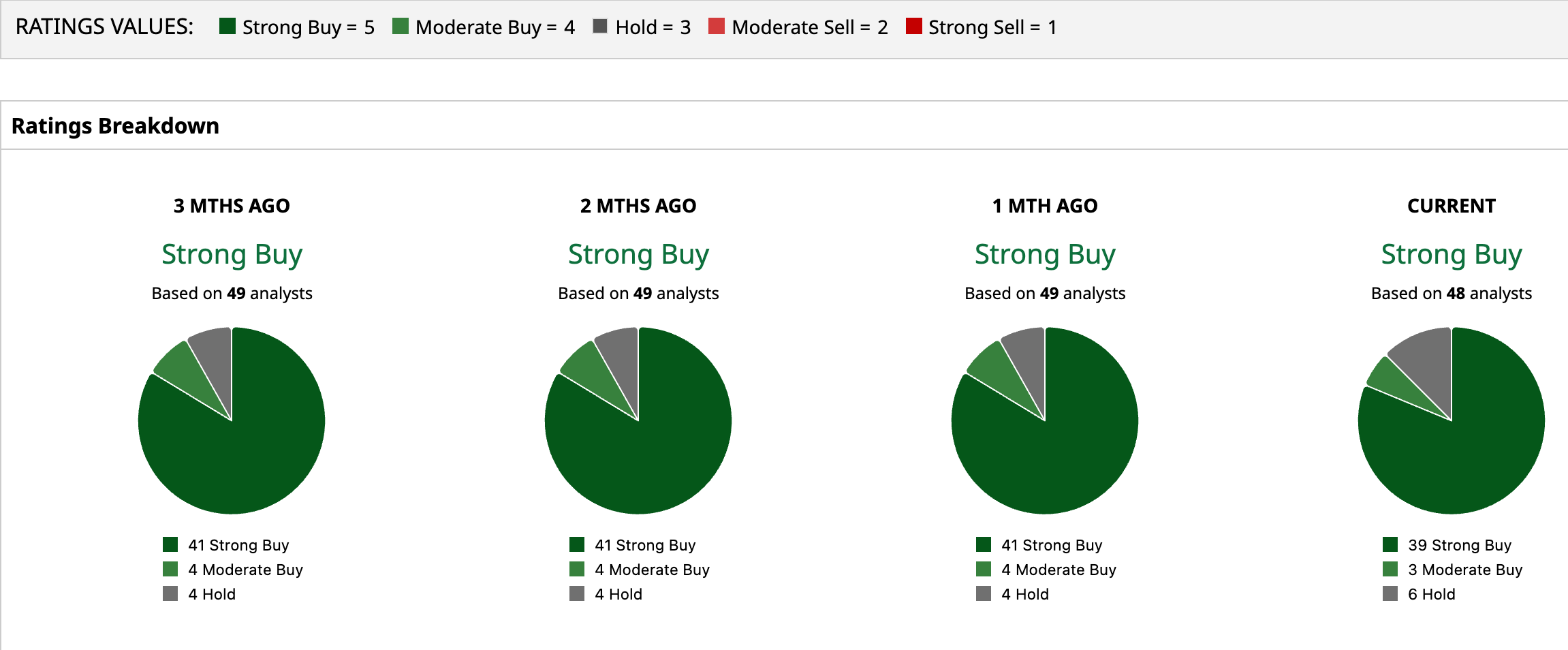

Analysts are upbeat on MSFT, with an overall “Strong Buy” consensus. Of the 48 analysts tracking the stock, 39 rate it a “Strong Buy,” three suggest a “Moderate Buy,” and the remaining six are on the sidelines with a “Hold” rating.

Microsoft’s rally may still have more fuel in the tank if we listen to the Wall Street. MSFT’s average price target of $553.83 suggests 25.5% upside potential from current levels. Some are even more optimistic. the Street-high target of $680, set by Tigress Financial, implies potential gains of 54.1%.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Despite Positive Developments, Rocket Lab Stock Is a High-Risk Name Fluence Energy Stock Is Soaring. Its Helping Nvidia Power a New Wave of Data Centers Ahead of Broadcom Earnings, Here’s What Barchart Data Says Comes Next for AVGO Stock Microsoft Stock Just Hit a 3-Month High. Investors Can Thank a ‘New Era of PC.’