Dell Technologies’ (DELL) investors had plenty to celebrate over the last few days. Shares jumped roughly 33% on Friday after a solid Q1 fiscal 2027 print, fueled by AI demand, increased infrastructure spending, and a stronger-than-expected outlook. The stock closed another 10% higher on Monday, touching a new all-time high of $469.47, as investors continued digesting these record-breaking results. Overall, just in the last five trading days, the stock has skyrocketed nearly 43%.

Behind this rally are three major reasons that suggest Dell’s best days may still be ahead.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

www.barchart.com

www.barchart.com The rally over the last few days has pushed Dell stock’s year-to-date gains up to 246%, enormously outperforming the trillion-dollar tech giants and the broader market. Dell crushed Wall Street’s expectations with massive AI demand, strong growth across its traditional businesses, and an outlook that suggests the momentum is far from over.

Reason No. 1: Dell's AI Gold Mine Just Got Even Bigger

With a market cap of $302.6 billion, Dell Technologies is a leading provider of AI servers, data storage solutions, networking equipment, and personal computers for businesses and consumers worldwide. The most obvious reason behind Dell’s stock rally was the explosive growth in its AI business. In the first quarter ended May 1, it generated an eye-popping $24.4 billion in AI orders and generated $16.1 billion in AI server revenue.

It ended the quarter with a $51.3 billion AI backlog, indicating future revenue growth. What’s more, management stressed that the company’s AI pipeline is multiple times bigger than the existing backlog. Plus, its AI demand is now coming from not just a select few hyperscalers but from over 5,000 organizations. Total revenue in the quarter surged to $43.8 billion, an increase of 88% year-over-year. The bottom-line growth was equally impressive. Adjusted earnings per share climbed 214% year-over-year to $4.86, beating consensus estimates by $1.90 per share.

Dell is expanding its AI ecosystem through partnerships with industry leaders such as Nvidia (NVDA), OpenAI, Alphabet (GOOG)(GOOGL), Palantir (PLTR), ServiceNow (NOW), CrowdStrike (CRWD), and Mistral AI. These partnerships boost Dell's AI Factory strategy and position as enterprise AI adoption rapidly scales. The message to investors this quarter was clear that Dell's AI opportunity is getting bigger, not smaller.

Reason No. 2: Core Business Is Booming Too

While AI stole the spotlight, its traditional businesses are performing exceptionally well. Notably, traditional server and networking revenue surged 92% YOY, as enterprise customers are aggressively refreshing aging infrastructure and expanding computing capacity. Interestingly, Dell emphasized that most of its installed server base is still operating on 14th-generation systems or older, which leaves plenty of room for future upgrades. Dell is modernizing its data centers and preparing for AI-driven workloads.

Additionally, storage revenue also surged 8% driven by the strong performance of its products, including the PowerStore, PowerMax, PowerScale, and ObjectScale. Meanwhile, Dell's Client Solutions Group revenue rose 17%, commercial sales increased 18%, and consumer revenue climbed 9%. Combined, these results showed that Dell's success extends far beyond AI servers.

Encouragingly, Dell is also converting its growth into substantial cash generation. It generated $3.16 billion in free cash flow and returned $2.1 billion to shareholders through dividends and stock repurchases.

Reason No. 3: Dell's Best Days May Still Be Ahead

These growth numbers alone would have impressed investors, but management's confidence that the company's momentum would continue throughout the rest of fiscal 2027 and beyond is what piqued their interest. For the second quarter, management expects total revenue between $44 billion and $45 billion, representing 49% growth at the midpoint. AI server revenue could be around $15.5 billion.

Looking ahead for the full fiscal 2027, management expects revenue to increase by 47% YOY at the mid-point to $167 billion. The company expects roughly $60 billion in AI server revenue for fiscal 2027, which could imply a growth of roughly 2.4 times fiscal 2026 figures.

Management believes demand will remain strong throughout the year as customers invest in AI infrastructure, modernize data centers, expand storage capacity, and refresh aging PCs. If these trends continue, Dell might be one of the biggest winners of the next wave of the enterprise AI boom. The good news is, despite the upbeat outlook, the stock is attractively priced at 25x forward estimated 2027 earnings, which are expected to increase by 79% YOY.

How High Does Wall Street Expect Dell Stock to Soar?

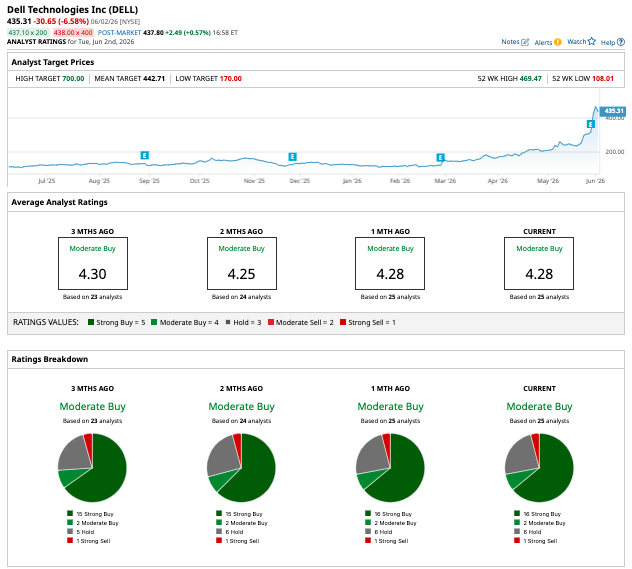

Wall Street knew Dell was benefiting from the AI spending boom, which is probably why a majority of analysts covering the stock rate it a “Strong Buy.” But what analysts didn't realize was just how fast that opportunity was growing. Overall, DELL holds a consensus “Moderate Buy” rating. Of the 25 analysts covering the stock, 16 rate it a “Strong Buy,” two say it is a “Moderate Buy,” six rate it a “Hold,” and one says it is a “Strong Sell.”

The stock has surpassed both its former mean target price and its high estimate of $350, with many analysts raised the target price for the stock to around $500 following the outstanding quarter. Barclays assigned a new high price estimate of $550 and the high target is now $700, which suggests the stock can climb another 61% from current levels.

www.barchart.com

www.barchart.com On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Texas Instruments Is a Major Winner of the AI Power Bottleneck, Investors Just Aren’t Seeing It Yet Dell’s Bull Rally Will Continue. Don’t Fall Into the Trap of Thinking It’s Just a Low-Margin Hardware Assembler. A $2 Billion Reason to Buy Little-Known Gorilla Technology Stock Right Now Cadence Design Is Cementing Its Place in the 2nm AI Chip Race By Solving the Die Size Limit in Partnership With a Major Chipmaker