Envista Corporation NVST is set up for steady value creation as it executes across growth, operational excellence, and people priorities. The company is using a productivity playbook to protect margins while spending more on innovation to support consistent product launches.

At $22.94 as of 06/02/2026, the shares sit below a 6–12 month price target of $24, framing a balanced risk-reward profile. NVST carries a Zacks Rank #3 (Hold).

NVST Snapshot and What the Report Says Now

Envista’s near-term setup is built around repeatable execution rather than a single standout quarter. The strategy centers on driving growth in core dental categories, tightening operations through a structured system, and strengthening talent development to support continuous improvement.

That positioning supports a measured upside case. The 6–12 month target of $24 versus the $22.94 stock price as of 06/02/2026 points to incremental appreciation potential, while macro volatility, tariffs, and competition keep the stance balanced.

In the past year, NVST shares have gained 22.4% against the industry’s 30.9% decline.

Image Source: Zacks Investment Research

Envista Business Mix That Investors Are Actually Buying

Envista operates through two segments that map cleanly to demand across the dental workflow. Specialty Products and Technologies generated 64.4% of 2025 revenue and includes implants, regenerative solutions, prosthetics, and associated treatment software, along with orthodontic brackets, aligners, and lab products.

Equipment and Consumables represented 35.6% of 2025 revenue and spans digital imaging systems, software and visualization solutions, endodontic systems, restorative materials, rotary burs, impression and bonding materials, cements, and infection prevention products. The breadth across implants, orthodontics, imaging, consumables, and software helps diversify demand drivers.

NVST Demand Signals From Q1 2026

Management described the dental market as stable to slightly improving in the first quarter of 2026, and category performance supported that view. Orthodontics, consumables, and diagnostics each delivered double-digit growth in the quarter, while implants grew at a mid-single-digit rate excluding China.

Growth was broad-based across both segments and most regions, with volume expansion and pricing both contributing. Developed markets led, with North America and Europe posting double-digit gains, while developing markets grew at a high-single-digit pace excluding China-related softness.

Envista Execution Engine Behind Margin Improvement

The Envista Business System is the core lever behind productivity and margin discipline, and it showed up in profitability metrics in the first quarter. Envista delivered 100 basis points of gross margin expansion and 120 basis points of adjusted EBITDA margin improvement, reflecting better operating leverage and execution.

At the same time, the company is spending more to sustain innovation, with research and development up 18.6% year over year to $30.0 million in the first quarter. Tariff costs rose $11 million year over year, but supply chain actions, selling, general and administrative discipline, and pricing initiatives helped offset the headwind.

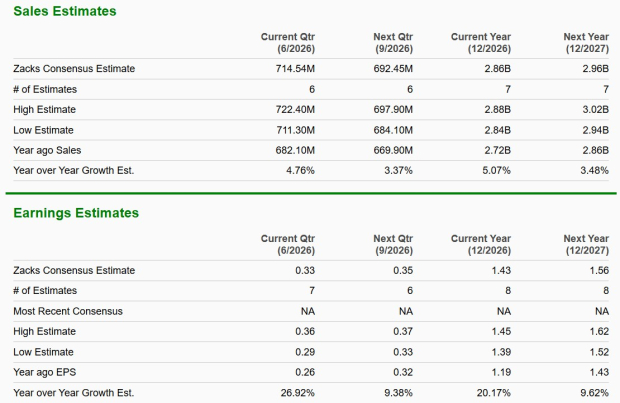

The Zacks Consensus Estimate for NVST’s 2026 sales and loss per share implies a year-over-year improvement of 5.1% and 20.2%, respectively. The bottom-line estimates have moved north in the past 60 days.

Image Source: Zacks Investment Research

Envista Financial Profile and Shareholder Moves

Envista ended the first quarter with $1.08 billion in cash and cash equivalents, no current debt, and $1.44 billion of long-term debt, down slightly from $1.45 billion in the prior quarter. Management continues to target approximately 100% free-cash-flow conversion for 2026, even as cash flow remains seasonally weakest early in the year.

Capital return is also part of the plan. Envista repurchased about $42.6 million of stock in the first quarter, and the board authorized an incremental $300 million addition to the repurchase authorization.

NVST The Big Risks to Monitor Into 2H 2026

First, macro uncertainty and geopolitics can pressure dental utilization and purchasing cycles, especially for equipment decisions that are easier to defer. China is a specific swing factor for implants as channel partners adjust inventories ahead of anticipated volume-based procurement, which management expects to begin between the second and third quarters.

Second, tariffs remain an ongoing cost headwind, with similar quarterly levels anticipated through 2026, and competition is intense in markets shaped by rapid technological change and pricing pressure. Consistent new-product traction is essential to sustain growth while Envista reinvests at double-digit rates in sales, marketing, and research and development. Foreign exchange is another variable given that 52.7% of first-quarter 2026 revenue came from outside the United States.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Envista Holdings Corporation (NVST): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).