Medtronic plc MDT used its fourth-quarter earnings call to press a forward-looking message rather than dwell on the quarter itself. Management framed fiscal 2026 as a turning point, with the strongest annual revenue growth in a decade and a broader set of growth platforms beginning to contribute.

That tone mattered because fiscal 2027 guidance kept growth expectations elevated even as investors pressed on structural heart, tariffs, margins and the pending Diabetes separation. The company’s answers suggested confidence in both portfolio depth and execution.

Medtronic Leans on Its Growth Engines

Chairman and CEO Geoff Martha centered the call on a handful of businesses he said are building durable momentum. Cardiac Ablation Solutions remained the clearest example, with 78% growth in the quarter, while newer platforms such as Symplicity, Hugo, Altaviva and Stealth AXiS also received outsized attention.

Martha argued the company is still in the early innings with Affera, pointing to a 40% sequential increase in the U.S. installed base and continued expansion of the electrophysiology ecosystem. He also highlighted growing procedure volumes for Hugo and stronger physician uptake for Altaviva.

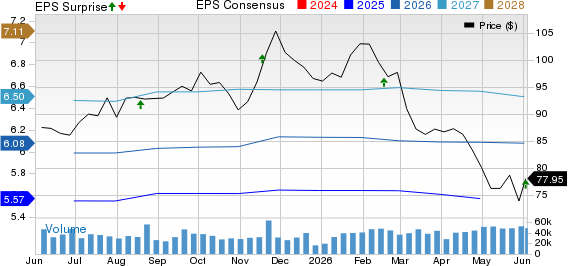

That framing helped explain why the quarter’s financial beats were treated more as validation than the main story. Adjusted earnings of $1.55 per share beat the Zacks Consensus Estimate of $1.54 by 0.58%, while revenues of $9.81 billion topped the $9.66 billion estimate by 1.48%.

Medtronic PLC Price, Consensus and EPS Surprise

Medtronic PLC price-consensus-eps-surprise-chart | Medtronic PLC Quote

MDT Guidance Keeps the Bar High

Chief financial officer Thierry Piéton guided to fiscal 2027 organic revenue growth of 6.75% to 7.25% and non-GAAP earnings per share of $5.90 to $6.00. The setup includes the extra selling week, continued consolidation of the Diabetes business and added contributions from recently announced deals.

Piéton said first-quarter organic revenue growth should run about 11.5% to 12%, with 500 to 600 basis points coming from the additional week. First-quarter adjusted earnings are expected at $1.38 to $1.40.

The outlook also carried explicit assumptions on headwinds. Management embedded about $250 million of tariff impact, roughly 2% dilution from M&A, higher interest and tax expense, and a roughly 1-point headwind from fuel and transportation costs tied to conflict in the Middle East.

Medtronic Uses M&A to Sharpen Focus

Management spent meaningful time on capital deployment, underscoring that Medtronic is using tuck-in acquisitions, venture investments and partnerships to deepen positions in faster-growing markets. In the quarter, the company closed the CathWorks acquisition and announced plans to acquire Scientia Vascular and SPR Therapeutics.

Martha described those moves as tightly aligned with a strategy of reinforcing leadership positions and expanding into adjacent markets where the company already has scale. He also pointed to investments in ICE catheter technologies and Pulnovo Medical, plus the ViaVerte distribution agreement with Merit Medical.

That message was paired with continued emphasis on portfolio focus. Management reiterated that the Diabetes separation is about strategic fit and capital allocation, not a lack of confidence in MiniMed’s outlook.

MDT Faces Questions on TAVR and Margins

Analyst questions quickly turned to areas of investor concern. A Wells Fargo analyst asked about TAVR after attention on long-term Evolut data, and Martha acknowledged that U.S. performance had softened, though he said weekly procedure volumes had stabilized over the last eight to 10 weeks.

Piéton said that stabilization is what Medtronic built into fiscal 2027 guidance. The response was notably measured, with management neither dismissing the issue nor suggesting a rapid rebound.

Margin questions were similarly direct. Piéton said gross margin should be roughly flat excluding tariffs, with pricing and cost savings offsetting mix pressure. He added that the second half should look better than the first, helped by lapping tariff effects and improving mix in Cardiac Ablation Solutions.

Medtronic Sees Broader Strength Beyond CAS

One of the more important messages from the call was that management wants investors to see growth as wider than one franchise. Piéton said Cardiovascular should perform in fiscal 2027 broadly in line with fiscal 2026, with Cardiac Rhythm Management and renal denervation adding support alongside CAS.

He was even more explicit on Neuroscience, where he said every franchise is positioned to accelerate. Stealth AXiS, Neurovascular innovation and Altaviva were all cited as contributors, while Martha also praised the underlying strength of CST, Surgery and CRM.

That breadth matters because it addresses the concern that Medtronic’s recent acceleration could narrow as CAS matures. Management’s position was that CAS remains powerful, but the next year should also benefit from several businesses moving higher at once.

MDT Enters FY27 With Confident Tone

The overall tone of the call was assertive but disciplined. Management repeatedly returned to execution, portfolio quality and innovation cadence rather than relying on macro relief or one-time factors to support the fiscal 2027 story.

Martha also used the session to emphasize leadership transition planning in Neuroscience and to reinforce that Medtronic views medtech demand as structurally resilient. The takeaway from the call was a company trying to show that fiscal 2026 momentum is broad enough to carry forward.

Zacks Signals on MDT

MDT currently carries a Zacks Rank #4 (Sell), along with a Value Score of B, Growth Score of D, Momentum Score of A and VGM Score of B. In Zacks terms, the rank remains the primary signal, while the Style Scores are meant to refine stock selection within that framework. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

The stronger Momentum and VGM profiles point to favorable style characteristics, but the Zacks Rank #4 tempers that setup. As with any post-earnings period, the rank can change as analysts revise estimates after the reported results and updated guidance.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Medtronic PLC (MDT): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).