Enova International ENVA has put up a strong run over the past year, supported by steady execution and a business mix that is tilting toward faster-growing small business lending. The stock’s consistent earnings outperformance has reinforced that narrative.

At the same time, investors are weighing real offsets. Expense pressure, credit normalization and a balance sheet with meaningful debt keep the risk profile elevated, even as growth drivers remain intact.

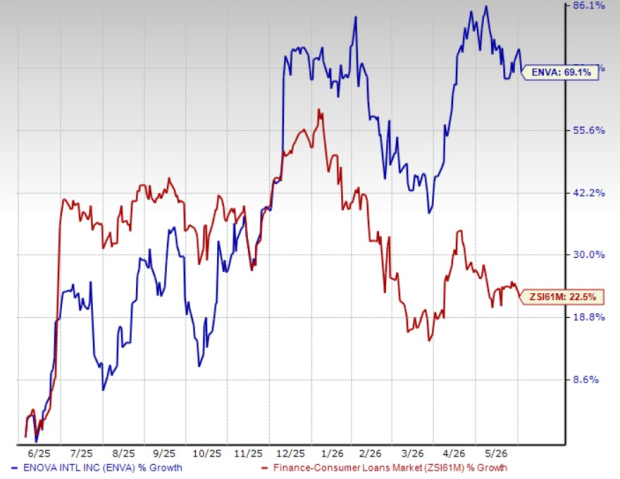

ENVA’s One-Year Run vs. Industry

ENVA has outperformed its industry over the past year, helped by a backdrop of solid operating momentum and repeated earnings outperformance.

Price Performance

Image Source: Zacks Investment Research

The company has topped the Zacks Consensus Estimate in each of the last four quarters, a pattern that has helped keep sentiment constructive. Another supportive signal is estimate stability. ENVA’s 2026 earnings estimates have been unchanged over the past month, which aligns with the view that fundamentals remain durable despite the risks investors are monitoring.

Estimate Revision Trend

Image Source: Zacks Investment Research

Enova’s SMB Shift Is Reshaping the Portfolio

The portfolio mix continues to move toward small business lending. As of March 31, 2026, small business loans represented 70% of the portfolio, while consumer loans accounted for 30%.

That shift is being driven by origination strength. In the first quarter of 2026, small business originations rose 42% year over year, extending a streak of nine straight quarters with more than 20% originations growth.

ENVA’s Q1 Results Shows Momentum

Revenue execution has been a clear pillar of the story. Net revenues increased 19.7% in 2025 versus 2024, and the rising trend continued into the first quarter of 2026.

Margin performance adds an important layer. Net revenue margin was around 60% by the end of the first quarter of 2026, pointing to scaling progress while maintaining disciplined pricing.

The trade-off was costs. Operating expenses jumped 26.6% year over year to $321.8 million, and results included $2.7 million of acquisition-related expenses tied to the pending Grasshopper Bancorp transaction.

Credit trends were mixed. In the first quarter, the consolidated net charge-off ratio improved to 7.6% from 8.6% a year earlier, and the 30-plus-day delinquency ratio eased to 7.4% from 7.7%.

But broader pressure is still part of the setup. Net charge-offs rose 14.6% year over year in 2025, and delinquencies increased 11.5% over the same period. The near-term outlook still calls for continued pressure, even with improvement expected over time.

Enova’s Debt and Liquidity Put Flexibility in Focus

Balance sheet flexibility remains a key debate. As of March 31, 2026, liquidity was $1.1 billion, including cash and marketable securities plus available facility capacity, while long-term debt stood at $4.83 billion.

That combination heightens sensitivity if conditions weaken, because higher leverage can limit room to maneuver. It also raises the bar for consistent credit execution and expense control as the business scales.

Capital return is another area investors are watching closely. ENVA announced a $400 million share repurchase program in November 2025 that runs through June 30, 2027.

In the first quarter, the company repurchased $16 million of common stock. As of March 31, 2026, $32.2 million remained available under the authorization, and the buyback has been flagged as potentially unsustainable given the liquidity profile and debt level.

Enova’s Key Watch List for the Next 2 Quarters

The next two quarters should clarify whether SMB momentum can stay strong without giving back operating leverage. Investors can track the pace of small business originations and whether the multi-quarter streak of strong growth remains intact.

Expense ratios are equally important. For the second quarter of 2026, management expects marketing at 20% of revenues, operations and technology at 8%-8.5%, and general and administrative expense around 5% excluding one-time items.

Credit performance and the Grasshopper timeline round out the checklist. Watch delinquency and net charge-off trends alongside progress toward an expected second-half 2026 close. Enova peers, Capital One COF and Ally Financial ALLY are also facing asset quality pressure. Both COF and ALLY’s provision for credit losses rose year over year in the first quarter of 2026 and expected to remain elevated in the near term given persistent inflationary pressure.

ENVA carries a Zacks Rank of 2 (Buy) at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Capital One Financial Corporation (COF): Free Stock Analysis Report

Ally Financial Inc. (ALLY): Free Stock Analysis Report

Enova International, Inc. (ENVA): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).