Grocery Outlet Holding Corp. GO is trading at a discounted valuation despite efforts to stabilize sales and improve profitability. The investment case hinges on whether the company can convert improving traffic trends, store optimization efforts, and a rebuilding opportunistic product mix into a sustainable earnings recovery.

The setup is attractive on price, but the next leg depends on execution. It is about whether near-term pressure on comparable sales, baskets, and margins can ease fast enough to support a cleaner recovery.

GO’s Neutral Setup: Upside Levers vs. Execution Risk

Grocery Outlet’s differentiated model is still a clear draw. Opportunistic sourcing, deep discounts on rotating “WOW!” deals, and an Independent Operator structure support a compelling customer value proposition and localized execution.

Management is also pushing initiatives that can improve consistency over time. Merchandising upgrades and store refreshes are designed to strengthen engagement and drive trip frequency.

The trade-off is that near-term results remain uneven. Comparable sales are still negative, basket size is soft, promotional intensity is elevated, and operating costs are rising. Those factors have kept pressure on margins and made the recovery look gradual rather than immediate.

Image Source: Zacks Investment Research

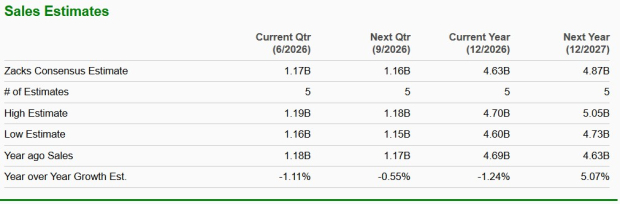

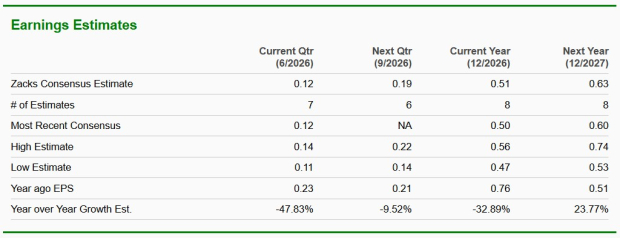

Grocery Outlet’s Earnings Bridge: What Must Improve

The latest quarter highlighted the checklist investors should watch. Comparable-store sales fell 1%, reflecting a 3.1% decline in average transaction size that more than offset a 2.1% increase in transactions. That mix signals improving traffic, but a basket that still needs rebuilding.

Margins are the next swing factor. Gross margin was 29.6%, down 80 basis points year over year, with part of the decline tied to markdowns and write-offs connected to optimization actions and the rest pressured by promotions used to bridge gaps in opportunistic supply.

Finally, expense leverage has to return for adjusted EBITDA to recover. Selling, general and administrative expenses rose to 29.8% of sales, and adjusted EBITDA fell to $43.1 million, with margin down to 3.7%. Management’s outlook keeps the near-term bar clear: second-quarter comparable sales are expected to decline 1.5% to 2%, while adjusted EBITDA is projected at $55 million to $58 million.

Image Source: Zacks Investment Research

GO’s Optimization Plan Aims To Lift EBITDA Quality

A key element of the strategy is pruning weaker assets. Grocery Outlet is closing 36 underperforming stores, with 27 closures completed in the first quarter and the remaining nine completed in April.

Management expects these optimization and restructuring actions to produce about $12 million of annualized adjusted EBITDA improvement once completed. The goal is a cleaner fleet mix with less operational drag and more resources concentrated in higher-return locations.

This matters because it links portfolio actions directly to earnings quality. If the company can remove low-return stores while tightening underwriting for new units, the path to more stable profitability becomes clearer.

Grocery Outlet’s Expansion Gets More Disciplined

Expansion is shifting toward returns-focused growth. Management is applying more rigorous site selection, higher return thresholds, and clustered expansion in core markets to improve supply chain efficiency, brand awareness, and operating leverage.

New store underwriting standards are also rising. The company is targeting stores capable of generating returns above 25%, with an ambition to approach 30% over time, and it is prioritizing higher-volume locations with stronger long-term economics.

For the current fiscal year, the plan calls for 30-33 net new store openings, excluding closures tied to optimization actions. That approach is meant to balance growth with profitability and reduce the risk of adding lower-quality units.

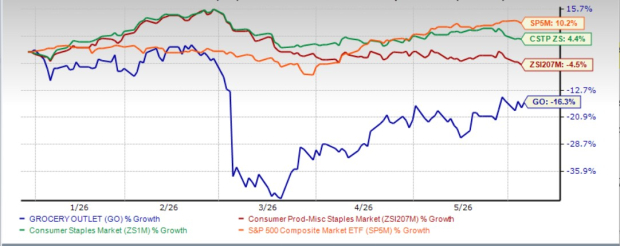

GO Valuation Context

The valuation case starts with what has already been discounted. GO shares are down 16.3% year to date, lagging both the Zacks Consumer Staples sector and the broader market.

Image Source: Zacks Investment Research

From a valuation standpoint, Grocery Outlet’s forward 12-month price-to-earnings ratio stands at 15.29, lower than the industry’s ratio of 17.07. It is also trading below its 12-month median level of 19.04, suggesting investors have yet to fully price in the company’s recovery potential.

In practical terms, the multiple has room to expand if comparable sales stabilize, margins stop sliding, and adjusted EBITDA begins to rebuild on cleaner fundamentals.

Image Source: Zacks Investment Research

A Practical Playbook for GO Investors

For now, the stock carries a Zacks Rank #3 (Hold), which supports a “monitor” posture while investors track whether the company can convert traffic gains into healthier baskets and better profit flow-through. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Signals that fundamentals are improving would include a better comparable-sales trajectory than current guidance, a stabilization in average transaction size, and evidence that margin pressure is easing as promotions normalize. Delivery of the expected annualized adjusted EBITDA uplift from optimization actions would also reinforce the earnings-quality angle.

What would undermine the thesis is a prolonged basket decline, margin pressure that lasts longer than expected, or a weaker comparable-sales trend that keeps leverage out of the model. Competition remains intense, with larger players such as Walmart Inc. WMT and Costco Wholesale Corporation COST able to pressure pricing and promotional activity, which can make GO’s margin stabilization harder to achieve.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Walmart Inc. (WMT): Free Stock Analysis Report

Costco Wholesale Corporation (COST): Free Stock Analysis Report

Grocery Outlet Holding Corp. (GO): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).