Zscaler, Inc. ZS is positioning itself to benefit from the next wave of artificial intelligence (AI) adoption by expanding its security platform to protect AI agents. As businesses increasingly deploy AI-powered tools and autonomous agents to access applications and data, the company believes that this emerging market could become a meaningful growth driver.

The strategy comes at a time when Zscaler is already seeing strong business momentum. In the third quarter of fiscal 2026, the company’s annual recurring revenues (ARR) rose 25% year over year to $3.53 billion. Revenues increased 25% to $850 million, while remaining performance obligations climbed roughly 30% to $6.5 billion, highlighting strong demand for its cybersecurity offerings.

AI-related products are becoming an important part of the recent growth momentum. Zscaler’s AI Protect solution, which helps customers discover AI assets, enforce security controls and prevent data leaks, generated more than $100 million in bookings over the past 12 months. Management noted that customer interest continues to grow as organizations seek ways to secure both public AI applications and internally developed AI models.

The company is also strengthening its capabilities through partnerships and acquisitions. Its planned acquisition of Symmetry Systems is expected to improve visibility into how users, applications, data and AI agents interact across enterprise environments. This should help Zscaler deliver stronger security controls for agentic AI deployments.

With AI adoption accelerating and cyber threats becoming more sophisticated, Zscaler’s expanding AI security portfolio could create a significant long-term growth opportunity. If enterprises increasingly rely on AI agents, the company may be well-positioned to capture a larger share of cybersecurity spending. The Zacks Consensus Estimate for Zscaler’s fiscal 2026 revenues is pegged at $3.33 billion, indicating 24.5% year-over-year growth.

How Do Zscaler’s Rivals Fare in the AI Security Race?

Zscaler competes with Palo Alto Networks, Inc. PANW and CrowdStrike Holdings, Inc. CRWD in the AI security space.

Palo Alto Networks is aggressively expanding its AI-driven security offerings through its platformization strategy. In the third quarter of fiscal 2026, the company’s revenues rose 31% year over year to $3 billion, while its next-generation security ARR exceeded $8 billion. Palo Alto Networks is integrating AI capabilities across network, cloud and security operations products, helping customers manage growing risks from AI applications and automated agents. Its broad product portfolio and large enterprise customer base make it a formidable rival to Zscaler.

CrowdStrike is another important competitor as enterprises look to secure AI-powered workloads and identities. In the first quarter of fiscal 2027, CrowdStrike’s revenues grew 26% year over year to $1.39 billion, whereas ARR jumped 24% to $5.51 billion. The company continues to enhance its Falcon platform with AI-native threat detection, identity protection and cloud security features. CrowdStrike’s strength in endpoint security gives it a strong position as AI agents increasingly interact with corporate devices, applications and data.

While both companies are investing heavily in AI security, Zscaler is differentiating itself through its Zero Trust architecture and its growing focus on securing AI agents, AI applications and machine-to-machine interactions across enterprise networks.

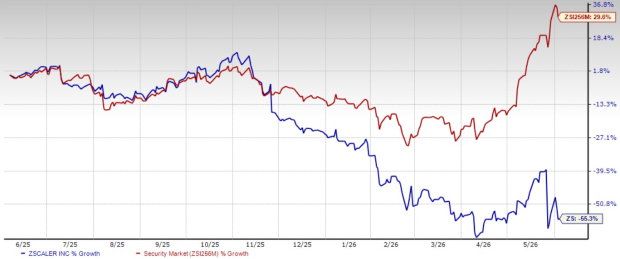

Zscaler’s Price Performance, Valuation & Estimates

ZS shares have plunged 55.3% over the past year against the Zacks Security industry’s rise of 29.6%.

Zscaler 1-Year Price Return Performance

Image Source: Zacks Investment Research

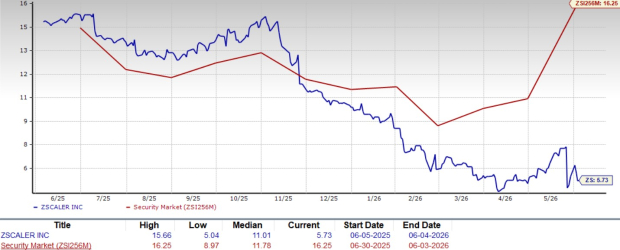

From a valuation standpoint, ZS trades at a forward price-to-sales ratio of 5.73, significantly below the industry’s average of 16.25.

Zscaler Forward 12-Month P/S Ratio

Image Source: Zacks Investment Research

The Zacks Consensus Estimate for Zscaler’s fiscal 2026 and 2027 earnings implies year-over-year increases of 23.2% and 12.1%, respectively. Estimates for fiscal 2026 have been revised upward over the past 30 days, while being revised downward for fiscal 2027.

Image Source: Zacks Investment Research

Zscaler currently carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power .

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Palo Alto Networks, Inc. (PANW): Free Stock Analysis Report

Zscaler, Inc. (ZS): Free Stock Analysis Report

CrowdStrike (CRWD): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).