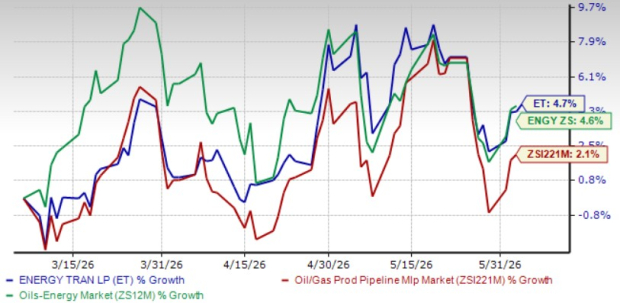

Units of Energy Transfer LP ET have rallied 4.7% in the past three months compared with the Zacks Oil and Gas - Production Pipeline - MLB industry’s growth of 2.1% and the Zacks Oil-Energy sector’s rally of 4.6%. This oil and gas midstream firm owns a wide network of pipelines across the United States and is pursuing opportunities to serve growing power loads from new demand centers across its network.

The midstream energy company benefits from its fee-based contract structure, which provides stable cash flows. As a leading exporter of liquefied petroleum gas, ET is also expanding its natural gas liquids (“NGL”) export infrastructure to meet growing global demand. However, higher operating costs and lower NGL and natural gas prices are offsetting some positives.

Price Performance (Three Months)

Image Source: Zacks Investment Research

Another company having extensive midstream operations in the United States is Kinder Morgan KMI. Kinder Morgan is poised to benefit from rising U.S. natural gas demand, supported by its extensive pipeline and storage assets serving key LNG export hubs along the Gulf Coast. In the past three months, KMI’s shares have plunged 5.6%, underperforming its industry and sector.

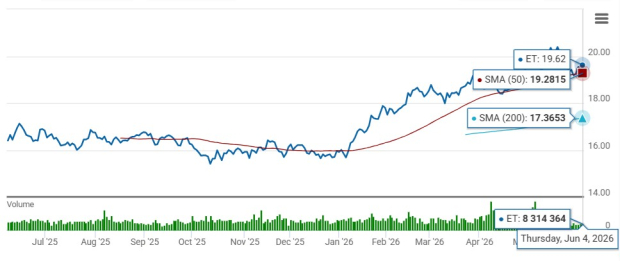

Energy Transfer’s units have been trading above both 50 and 200-day simple moving averages (SMAs), signaling a short-term bearish trend.

The 50 and 200-day SMAs are key indicators for traders and analysts to identify support and resistance levels. It is considered particularly important as this is the first marker of an uptrend or downtrend.

ET’s 50 Day and 200 Day SMA

Image Source: Zacks Investment Research

Should investors add Energy Transfer to their portfolios based solely on its recent share price gains? A closer look at the company’s fundamentals can help determine whether ET presents an attractive entry opportunity.

Factors Fueling Energy Transfer’s Operational Growth

Energy Transfer operates one of the largest midstream networks in the United States, with more than 140,000 miles of pipelines and related infrastructure across 44 states. Its diverse asset base includes crude oil and natural gas pipelines, gathering and processing facilities, and storage assets strategically located in major production regions and high-demand markets. This broad footprint supports stable and resilient earnings.

The firm’s extensive network allows it to efficiently serve a wide range of customers and end markets. Supported by a strong customer base and a predominantly fee-based business model, nearly 90% of Energy Transfer’s revenues are generated from transportation and storage services. This structure helps shield cash flows from commodity price volatility and provides greater earnings stability.

Energy Transfer continues to grow through organic expansion projects, strategic acquisitions and partnerships. The company has NGL export capacity of more than 1.4 million barrels per day and is further enhancing its capabilities through expansion projects at the Marcus Hook and Nederland export terminals. With an estimated 20% share of global NGL exports, Energy Transfer is well-positioned to benefit from rising international demand and expanding LNG export opportunities, particularly amid ongoing geopolitical tensions in the Middle East.

Energy Transfer is expanding its infrastructure to support growing energy demand through targeted investments across its natural gas, NGL and crude oil networks. Recent initiatives include the startup of the Gateway NGL pipeline debottlenecking project, commissioning of the Mustang Draw I processing plant, ongoing fractionation and ethane storage expansions at Mont Belvieu, and the Bayou Bridge pipeline expansion. These projects are expected to enhance capacity, improve operational efficiency and position the company to meet rising customer demand.

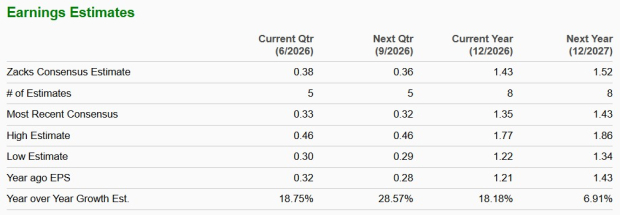

ET’s Earnings Estimates Moving North

The Zacks Consensus Estimate for Energy Transfer’s 2026 and 2027 earnings per unit indicates year-over-year growth of 18.18% and 6.91%, respectively.

Image Source: Zacks Investment Research

Another firm operating in the same space, Enterprise Products Partners EPD, also registered a year-over-year increase in earnings per unit estimates. The 2026 and 2027 earnings estimates of EPD indicate a year-over-year increase of 12.03% and 10.55%, respectively.

ET Shares More With Unitholders

In the first quarter of 2026, the partnership raised the quarterly cash distribution to 33.75 cents per unit, more than 3% higher than the prior-year period. Management has raised distribution rates 18 times in the past five years, and the current yield is 6.88% better than its industry’s yield of 5.36%.

Enterprise Products Partners has raised cash distribution rates nine times in the past five years. The current yield of EPD is pegged at 5.76%.

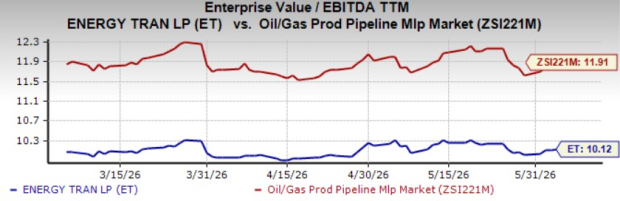

ET’s Units Are Trading at a Discount

ET’s current trailing 12-month Enterprise Value/Earnings before Interest Tax Depreciation and Amortization (EV/EBITDA) is 10.12X compared with the industry average of 11.91X. This indicates that the firm is presently undervalued compared with its industry.

Image Source: Zacks Investment Research

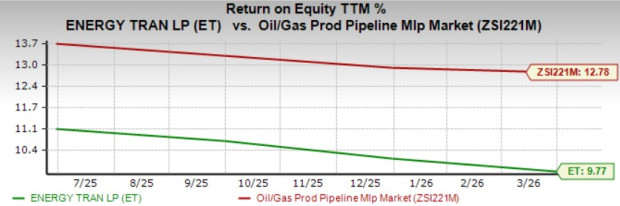

ET Stock’s ROE Is Lower Than the Industry

Return on equity (“ROE”) is a financial ratio that measures how well a company uses its shareholders’ equity to generate profits. The current ROE of the company indicates that it is using shareholders’ funds more efficiently than peers.

Energy Transfer’s trailing 12-month ROE is 9.77%, lower than the industry’s 12.78%.

Image Source: Zacks Investment Research

Rounding Up

Backed by more than 140,000 miles of pipelines and related infrastructure, Energy Transfer is well positioned to benefit from continued growth in U.S. oil, natural gas and NGL production. Its predominantly fee-based business model provides stable cash flows and supports the partnership’s ability to create long-term value for unitholders.

The stock appears attractive due to its improving earnings outlook and discounted valuation. Existing investors may consider holding this Zacks Rank #3 (Hold) stock to continue benefiting from its consistent cash distributions. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

However, with return on equity currently trailing the industry average, prospective investors may want to wait for a more favorable entry opportunity before initiating a position.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power .

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Enterprise Products Partners L.P. (EPD): Free Stock Analysis Report

Kinder Morgan, Inc. (KMI): Free Stock Analysis Report

Energy Transfer LP (ET): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).