Dell Technologies (DELL) is still looking like one of the cleaner ways to play the AI hardware boom, and the market is paying up for that story. On June 1, DELL stock jumped about 11% and reached a new high of $469.47 after Morgan Stanley raised its price target to $448 from $170, adding another layer to a rally already built on blowout earnings and a fast-rising AI server business.

Morgan Stanley’s upgrade matters because it came after Dell already delivered a massive quarter. Analysts moved the stock to an “Equal-Weight” rating from “Underweight” and said that Dell has handled supply-chain pressure and memory shortages better than rivals.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

With shares now trading near the $400 mark, the call looks less like a bargain hunt and more like a nod that the market has started to catch up with Dell’s execution.

Why Dell Keeps Stock Hitting New Highs?

DELL stock has been on a tear since its latest earnings result. Shares are up 84% for the past one month and have climbed about 216% so far in 2026. Dell shares keep reaching new highs because investors are rewarding the company's explosive AI server growth, massive earnings beats, and higher guidance.

Dell reported AI server revenue growth of 757% in the first quarter of fiscal 2027, raised its full-year outlook, and continues to receive major Wall Street target hikes, including Morgan Stanley's recent increase. Strong AI demand and a growing backlog remain key drivers.

However, the valuation is where the debate gets interesting. Dell’s forward price-to-earnings (P/E) ratio is at 32.5 times, while the tech sector trades around 28 times forward earnings. Using rough math, Dell’s market value of about $272.5 billion against estimated fiscal 2027 revenue of $167 billion at the midpoint works out to about 1.6 times sales. That is not cheap for a hardware company, but it is not crazy for a business growing this fast, either.

www.barchart.com

www.barchart.com Dell Tops Q1 Earnings Estimate

The Q1 report was the real catalyst. Revenue rose 88% to $43.84 billion, adjusted earnings climbed 214% to $4.86 per share from $1.55 a year earlier, and GAAP profit was $3.44 billion, or $5.24 per share. Infrastructure Solutions Group revenue jumped 181% year-over-year (YOY) to $29 billion, while AI-optimized server revenue exploded 757% to $16.1 billion. Client Solutions Group sales also rose 17% YOY to $14.6 billion.

Cash generation was strong as well. Dell said operating cash flow hit $4.1 billion, and the company returned $2.1 billion to shareholders in the quarter. Management raised full-year revenue guidance to a range of $165 billion to $169 billion from $138 billion to $142 billion, lifted adjusted EPS guidance to $17.90, and expects Q2 revenue of $44 billion to $45 billion as well as adjusted EPS of about $4.80. Dell also expects AI server revenue for full-year fiscal 2027 to reach about $60 billion.

Dell Expands Beyond the AI Boom

Dell is not just leaning on one big quarter. For example, the company just rolled out a new XPS 13 laptop starting at $699 — its cheapest XPS ever — aiming to grab market share from Apple’s (AAPL) new MacBook Neo.

On the enterprise side, Dell also recently won a huge U.S. defense contract; the U.S. Department of Defense has awarded Dell a $9.7 billion agreement to consolidate Microsoft (MSFT) services across the military. That win underlines Dell’s deepening presence in government and enterprise IT.

What Do Analysts Think of DELL Stock?

Morgan Stanley isn’t alone in pushing its target for DELL stock higher. Susquehanna recently raised its rating to “Positive” with a massive $700 target, saying AI-driven server demand can scale without hurting margins. Similarly, Barclays pointed to strong segment performance and lifted Dell’s AI sales forecast to $60 billion. JPMorgan, Piper Sandler, and others have likewise bumped their targets near $500 on booming data‑center growth. Even Goldman Sachs recently lifted its target to $500 while keeping a “Buy.”

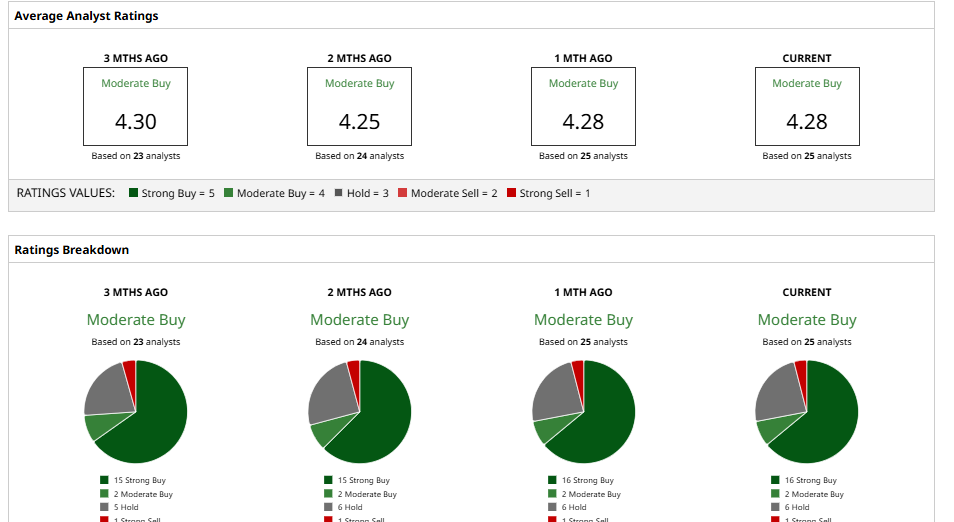

Based on 25 analysts with coverage, DELL stock has a consensus “Moderate Buy” rating overall. The average target of $485.95 points to potential upside of 22% from current levels.

www.barchart.com

www.barchart.com On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Morgan Stanley Revamps Its Dell Stock Price Target After Blowout Earnings. Dell Is Expanding Beyond the AI Boom. Subdued Put Activity Signals Opportunity in 4 Cash-Secured Puts for Income and Value Dell Stock Looks Poised to Keep Climbing. Here’s Why. How to Play QNT Stock After the Quantinuum IPO