AI and chip stocks tanked on Friday, sending the Nasdaq tumbling 4%. The bulls could dig their heels in again early next week. But there’s no doubt that a larger pullback will happen at some point to provide a healthy recalibration because stocks can only climb so high before the laws of market gravity take over.

This means investors should start buying tech stocks right now that haven’t rallied to new all-time highs alongside semiconductor and artificial intelligence stocks.

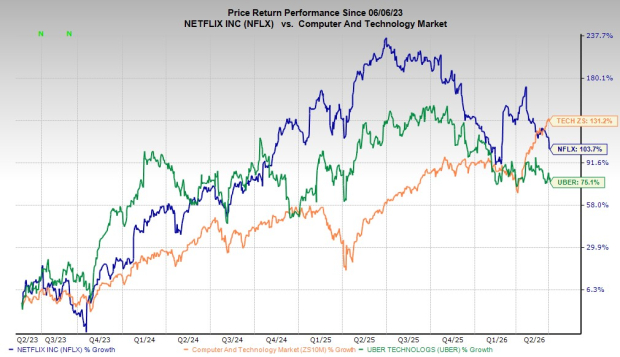

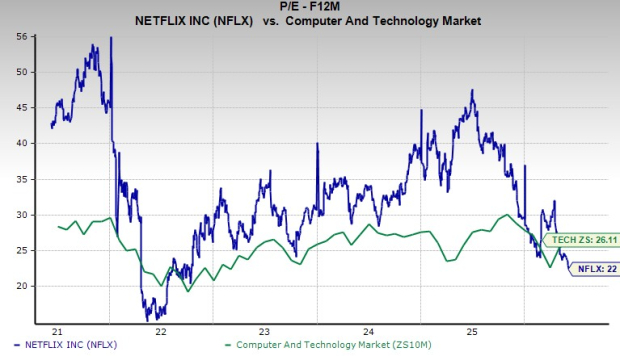

Netflix stock is down almost 40% from its 2025 highs to trade at a discount to the technology sector (22X forward earnings vs. 26.1X) despite crushing it over the last 10 and 20 years. The streaming entertainment giant is more resilient to AI threats than many technology firms, and Netflix is set to grow its earnings by 42% in 2026 on 14% higher sales.

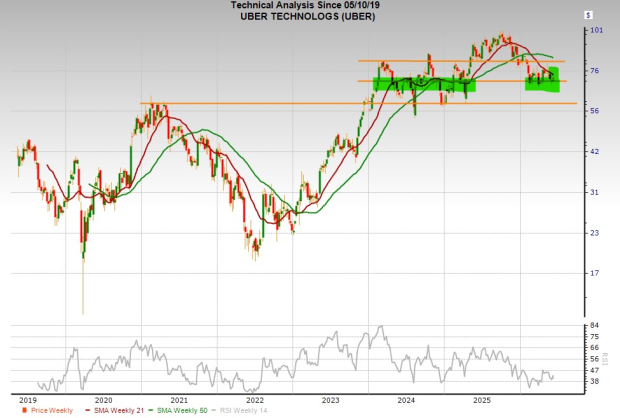

Meanwhile, Uber has fallen 30% since October, and its average Zacks price target offers 48% upside from its current levels. The ride-hailing company’s long-term upside remains in place even as it faces possible disruptions from tech firms looking to capture their share of a possible future full of robotaxis and autonomous delivery vehicles.

Image Source: Zacks Investment Research

Uber and Netflix are also looking to find support at some key technical ranges that might make them more enticing for long-term investors since they offer strong growth that’s not based on AI promises alongside solid value in an overheated market.

Portfolio Rotation: Buy Stocks Outside AI and Semiconductors

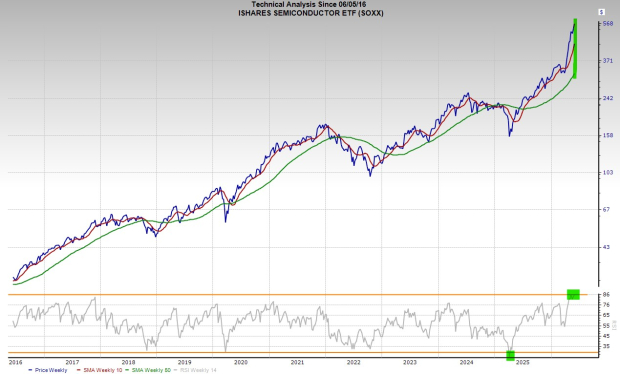

AI and chip stocks look overheated in the short run. For example, the iShares Semiconductor ETF SOXX soared 95% between March 30 and June 4, taking it miles above its 10-week moving average and to its most overbought RSI levels in over a decade.

Some investors might not want to chase AI and chip stocks that have soared 50%, 100%, or 200% YTD (including the huge fall on Friday).

Image Source: Zacks Investment Research

The next pullback to a key technical level might be scooped up rather quickly considering that the long-term AI outlook is bullish. It is just hard to try to chase stocks here, especially if Friday’s selling triggers the start of a near-term selloff.

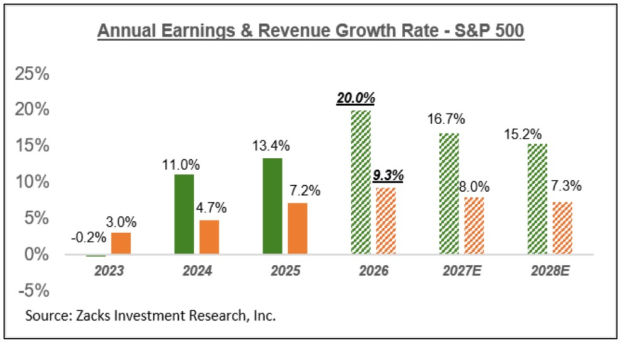

Thankfully, the long-term bull case for the stock market remains firmly intact. Total annual S&P 500 earnings are projected to grow 20% in 2026 on 9.3% higher sales, blowing away 2024 and 2025’s growth rates. The benchmark is projected to follow this up with 16.7% EPS expansion next year and 15.2% higher in 2028.

Image Source: Zacks Investment Research

More importantly, all 16 Zacks sectors are projected to report YoY earnings growth in 2026, highlighting impressive expansion and economic resilience despite fears.

Buy Tech Stock Uber Now for Value, Growth & 40% Upside

Uber Technologies, Inc.’s UBER core ride-hailing and delivery businesses are more popular than ever, particularly among higher-income consumers who are less impacted by inflation and economic cycles. The company is also running a physical business that’s not going to be disrupted by AI. Uber is poised to thrive in the potential driverless vehicle era through numerous partnerships and beyond.

Uber’s gross bookings are projected to jump 21% in 2026, based on our Zacks Key Company Metrics data. Its monthly active platform customers (MAPCs) are projected to climb 9% to 219.9 million in 2026, up from 202 million last year, 171 million in 2024 (vs. 118 million in 2021).

Image Source: Zacks Investment Research

The firm has exploded in popularity as it delivery business and ride-hailing units gain steam in the U.S. and globally. It grew its revenue 300% from the pre-Covid 2019 period’s $13 billion to $52 billion in 2025. Looking ahead, Uber is projected to grow its revenue by 11% in 2026 and over 15% next year to $66.6 billion.

The firm’s Uber One paid membership surpassed 50 million members globally in the first quarter of 2026, with “50% of Mobility and Delivery Gross Bookings now generated by members.” Uber is expanding its business via deals with Expedia to capture more “everyday consumer intent” across mobility, local commerce, and travel.

Image Source: Zacks Investment Research

It has also turned into a profitable company by taking a larger percentage of each ride/delivery fare while optimizing pricing and driver payments, alongside other profitability efforts. Uber posted GAAP earnings per share of $4.73 a share in FY25 vs. a loss of -$4.69 a share in 2022.

That said, its EPS growth is projected to take a hit in 2026 due to a ramp-up in investments across autonomous vehicles/robotaxis, international delivery expansion, AI efforts, and a key accounting change due to a business model change in the UK. Thankfully, it’s projected to bounce back and return to YoY growth in FY27 and beyond.

Image Source: Zacks Investment Research

Uber stock has dropped 30% from its October 2025 highs. The stock has climbed 70% since going public in May 2019. It is trying to hold its ground at the key technical range above, while trying to finally climb back above its 21-week moving average.

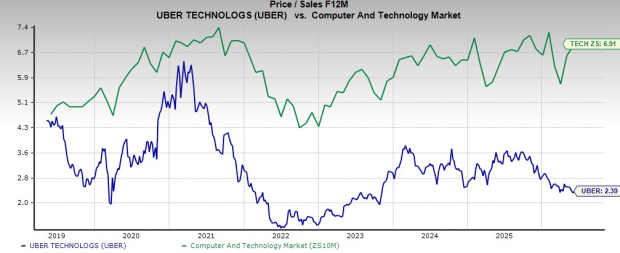

Uber is trading 95% below its highs and 22% below Tech at 20.2X forward earnings. It also trades at a 65% discount to Tech and 60% against its peaks at 2.4X forward sales. Uber’s average Zacks price target offers 48% upside from its current $70.71 a share.

NFLX: Buy This Tech Stock Now and Hold Forever?

Netflix, Inc. NFLX stock has fallen ~40% from its summer 2025 highs, providing investors with a great chance to buy a proven tech giant that's growth isn’t tied to lofty AI goals.

Plus, NFLX’s at-home entertainment model isn’t easily disrupted by AI, and it’s one of the last small luxuries that people cut back on.

Image Source: Zacks Investment Research

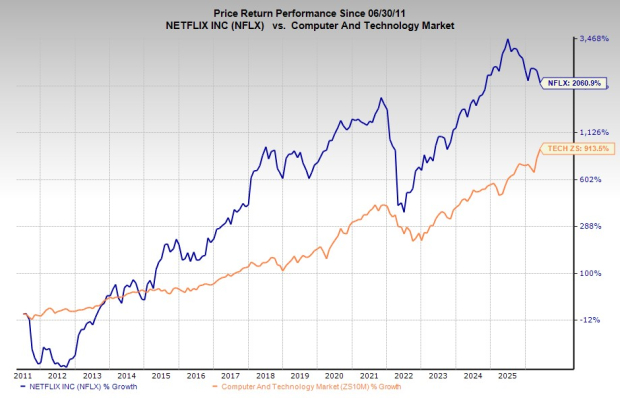

NFLX stock has skyrocketed ~20,700% in the past 20 years and 750% in the past decade, to blow away tech during both periods.

Yet, its recent fall, coupled with its strong earnings growth outlook, has it trading at a 60% discount to its highs and 15% below Tech at 22.0X forward 12-month earnings. Netflix is trading at some of its most oversold RSI levels in the last 10 years and attempting to hold its ground at a key 2024 breakout range.

NFLX’s average Zacks price target marks 42% upside from its current levels, and it would have to jump nearly 65% to return to its all-time highs.

Image Source: Zacks Investment Research

Netflix’s balance sheet is strong, greatly expanding its shareholders' equity in the past five-plus years. It is also now churning out strong free cash flow growth, boosted by its ability to raise prices, streamline operations, and more. And it isn’t caught up in the AI arms race that’s starting to drain the Mag 7’s cash reserves.

NFLX formally dropped out of the bidding war to buy Warner Bros. Discovery. The move will turn out to be a win in the long run since it preserved its core business model and balance sheet. Netflix said it crossed the 325 million paid memberships milestone in the final quarter of 2025, up from 302 million in 2024.

Image Source: Zacks Investment Research

The streaming TV giant Netflix rolled out a lower-cost, ad-supported subscription plan in the fall of 2022. The ad-based tier has gained a ton of momentum since then, helping it compete in a highly competitive streaming marketplace.

On top of that, Netflix's expansion into live sports (deals with the NFL, WWE, and much more), reality TV, podcasts, and more has helped it retain and attract subscribers. It is even rolling out video game content.

Image Source: Zacks Investment Research

The company is projected to grow its revenue by 14% in 2026 and 12% next year to reach $57.47 billion. This YoY growth is roughly in line with its 12.7% average sales expansion in the trailing five years.

NFLX is projected to grow its earnings by 42% in 2026 and 7% in FY27, following 28% growth last year and 65% in 2024.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power .

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Netflix, Inc. (NFLX): Free Stock Analysis Report

iShares Semiconductor ETF (SOXX): ETF Research Reports

Uber Technologies, Inc. (UBER): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).