AppFolio, Inc. APPF has spent much of 2026 under pressure, with the stock giving back a significant portion of the gains it delivered over the last few years. The pullback has shifted investor attention away from momentum and toward fundamentals. At current levels, the debate is less about how fast the stock can rise and more about whether the company can continue executing on the operating model that has supported its premium valuation.

For investors evaluating the stock today, the key question is straightforward: Can AppFolio continue increasing revenue per unit through AI-driven workflow adoption, premium-tier upgrades and usage-based services while maintaining margin expansion and healthy cash generation?

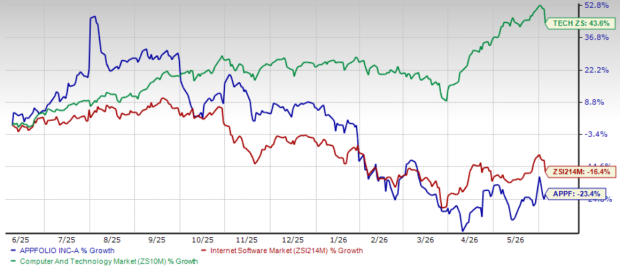

APPF's Setup After the Drawdown

APPF shares have declined 28.3% year to date and 23.4% over the past 12 months. While the selloff has reduced valuation pressure, it has also raised expectations around execution.

APPF One-Year Price Return Performance

Image Source: Zacks Investment Research

Unlike earlier stages of growth when customer and unit additions were the primary focus, AppFolio's growth story is increasingly tied to monetization. The company is generating more revenue from existing customers through premium-tier upgrades, AI-powered workflow tools, resident services and transaction-based offerings.

As a result, investors are now watching less for explosive footprint expansion and more for evidence that customers are adopting higher-value products. The market is effectively betting that AppFolio's AI-native platform, growing resident-services ecosystem and usage-based revenue streams can continue driving revenue growth even as customer and unit growth remain in the high-single-digit range.

AppFolio's recent results suggest this strategy is working, but sustaining that momentum will remain critical for the stock.

AppFolio's Price Target and What It Implies

APPF’s 6-to-12-month price target stands at $172, based on a forward 12-month sales multiple of 5.08x, slightly above the stock's current trading multiple of 4.84x. While that does not imply dramatic upside from current levels, it does suggest confidence that AppFolio can continue executing against its growth and profitability objectives.

To justify that valuation, investors will likely want to see continued momentum in several areas. These include premium-tier upgrades to Plus and Max plans, deeper adoption of Realm-X AI solutions, higher attachment of Resident Onboarding Lift and sustained growth in payments, screening and risk-mitigation services.

In other words, the valuation assumes AppFolio can continue turning customer activity into higher revenue per unit while maintaining the operating discipline that has supported recent margin expansion.

APPF's Relative Valuation Versus Software Peers

APPF currently trades at approximately 4.84x forward 12-month sales.

That compares with 3.79x for the Zacks Internet Software industry, 6.91x for the broader Computer & Technology sector and 5.21x for the S&P 500.

APPF Forward 12-Month Price-To-Sales (P/S) Ratio

Image Source: Zacks Investment Research

AppFolio trades above its immediate software peer group but below many higher-growth software names. This suggests investors recognize the company's attractive business model and expanding profitability but remain cautious about some of the risks embedded in the story.

Those concerns primarily center around the company's payments-heavy revenue mix, the impact of AI infrastructure investments on margins and the increasing dependence on product attachment and upselling rather than accelerating customer growth.

The stock is no longer being valued as a pure high-growth software name. Instead, investors appear to be assigning value to AppFolio's ability to monetize transactions and workflows at scale while continuing to improve profitability over time.

AppFolio's Growth and Profitability Signals

The company's latest results reinforced the strength of the underlying business.

First-quarter 2026 revenues increased 20% year over year to $262 million. Subscription Services revenue rose 18% to $58.2 million, while Value-Added Services revenue grew 22% to $201.4 million.

The growth drivers remain consistent. Higher usage of electronic payments, tenant screening, FolioGuard risk mitigation products and resident services contributed meaningfully to results. At the same time, premium-tier upgrades and AI-powered solutions such as Realm-X Performers are becoming larger contributors to revenue growth.

Profitability also continued to improve. Non-GAAP operating margin expanded to 27.3% in the first quarter of 2026, up from 24.3% in the prior-year period. Research and development expenses and general and administrative expenses both declined as a percentage of revenue, demonstrating the benefits of scale and improving operational efficiency.

Management has also highlighted that AI is helping accelerate internal product development, allowing engineering teams to build and deploy new capabilities more efficiently. This is creating operating leverage beyond what investors would typically expect from a growing software company.

That said, margin expansion is not without challenges. Cost of revenues stood at roughly 36% of revenues and is expected to stay relatively stable throughout 2026. The company's rapidly growing payments business carries higher third-party processing costs, while increasing AI adoption requires additional data-center and infrastructure spending. The result is a business that continues to expand margins, but likely at a measured pace rather than through dramatic gross-margin improvement.

APPF's Near-Term Rating and Style Profile

APPF currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

The stock also holds a VGM Score of B, supported by a Growth Score of A and Momentum Score of B, while its Value Score sits at D.

These ratings tell an important story.

Growth-oriented investors may find the company attractive because of its ability to drive higher revenue per unit through AI adoption, premium subscriptions and expanding value-added services.

Investors focused on valuation may be more cautious. The D Value score reflects a business that still trades at a premium relative to many software peers and therefore requires continued execution to justify its multiple.

Momentum investors face a more balanced picture. The recent share-price decline has reduced enthusiasm around the stock, but operating performance remains strong enough to support future recovery if execution continues.

AppFolio's Bull Case Drivers

The bullish thesis centers on AppFolio's increasing role as the operating system for property managers.

AI adoption remains one of the strongest indicators supporting that view. Management disclosed that more than 99% of customers now use some form of AI-powered functionality. AI actions increased sevenfold year over year, while Performer adoption climbed nearly 500% quarter over quarter.

Those numbers suggest AI is becoming embedded in everyday workflows rather than remaining a niche feature.

The company is also benefiting from strong attachment rates for resident services and workflow automation products. Resident Onboarding Lift, Realm-X Leasing Performer and Maintenance Performer are helping customers automate tasks, improve resident experiences and increase operational efficiency.

Meanwhile, AppFolio continues to generate operating leverage. Management raised its 2026 non-GAAP operating margin outlook to 26%-28%, reflecting confidence in the company's ability to balance growth investments with profitability.

Capital allocation remains another positive. During the first quarter, AppFolio repurchased approximately $125 million of stock and still has $125 million remaining under its authorization. Combined with a debt-free balance sheet, this provides additional flexibility to support shareholder value.

APPF's Key Risks That Can Break the Thesis

Despite the strong operating performance, several risks remain.

The biggest challenge is the company's revenue mix. Value-Added Services, particularly payments, continue to grow faster than subscription revenue. While this supports overall revenue growth, payments carry higher third-party costs, limiting the amount of gross-margin expansion investors might otherwise expect.

Cash conversion is another area to monitor. During the first quarter, operating cash flow was impacted by working-capital movements and higher accounts receivable balances. At the same time, AI-related infrastructure spending continues to increase.

While management views these investments as necessary to support future growth, they can create volatility in cash generation from quarter to quarter.

Finally, customer growth and unit growth remain relatively modest. Units under management grew 8% year over year and customer growth was 7%. This means the company's growth increasingly depends on premium-tier upgrades, AI adoption and greater use of value-added services.

If attachment rates slow or customers become more selective about adopting new products, revenue growth could moderate from the high-teens and low-twenties range seen recently.

AppFolio's Practical Decision Framework

For investors evaluating APPF today, the investment case can be simplified into four key operating metrics. First, watch product attachment and upsell trends. Continued adoption of Plus and Max plans, Realm-X Performers and Resident Onboarding Lift will be critical for sustaining revenue-per-unit growth.

Second, monitor cost-of-revenue trends. Investors will want confirmation that payment-processing costs and AI infrastructure investments remain manageable as a percentage of revenue. Third, focus on operating margins. Maintaining non-GAAP operating margins near the guided 26%-28% range would reinforce confidence in the company's ability to scale profitably.

Finally, watch cash generation. A return to stronger cash conversion after first-quarter working-capital pressures would strengthen the overall investment thesis.

At current levels, AppFolio appears less like a momentum story and more like an execution story. The company's AI-native platform, expanding value-added services and improving profitability provide a compelling long-term foundation. However, the stock's future performance will likely depend on management's ability to keep increasing monetization per customer while preserving margins and cash flow.

For investors comfortable with that balance of opportunity and risk, APPF remains a high-quality vertical software company worth watching closely as its AI-driven growth strategy continues to unfold.

For context, investors looking across software platforms may also track names like Paycom Software Inc. PAYC, which is a provider of cloud-based human capital management software as a service solution for integrated software for both employee records and talent management processes. BILL Holdings, Inc. BILL, which positions itself as a financial operations platform automating back-office workflows. Atlassian TEAM is another reference point in workflow software, with collaboration and project tools like Confluence and Jira aimed at embedding into daily work.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Paycom Software, Inc. (PAYC): Free Stock Analysis Report

AppFolio, Inc. (APPF): Free Stock Analysis Report

Atlassian Corporation PLC (TEAM): Free Stock Analysis Report

BILL Holdings, Inc. (BILL): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).