Fidelity National Information Services, Inc. FIS recently formed a strategic partnership with Fuse, a cloud-native loan origination platform, to build a modern end-to-end origination solution for indirect auto and equipment lenders across the United States and Canada.

The core problem they're solving is: lenders often get stuck on legacy systems, patching broken integrations, doing manual underwriting and losing deals because they simply couldn't move fast enough. Under the alliance, Fuse's platform integrates with FIS Asset Finance and FIS AutoSuite, while open API tools simplify connections to dealer systems and third-party data providers. Lenders can now change pricing and policies on their own, no hard-coding required.

Slower speed kills deals in lending. Many lenders face growing pressure to improve decision speed and dealer experience as competition across the lending market intensifies. This alliance gives them a credible path to modernization without ripping out everything they already have.

Financial Implications

The math is straightforward. Faster decisions mean more funded loans. Fewer manual steps mean lower operational costs. Built-in automation is designed to reduce manual underwriting activity, improve efficiency, and deliver quicker lending decisions. Stronger dealer relationships follow naturally when approvals stop stalling.

A stronger origination offering can make FIS more competitive when lenders evaluate technology vendors, helping the company attract new customers and deepen existing relationships. The partnership can also create opportunities to sell additional products across the lending workflow, increasing the value of each client relationship. Over time, broader adoption could support recurring software revenue, improve customer retention and strengthen FIS' standing in the market.

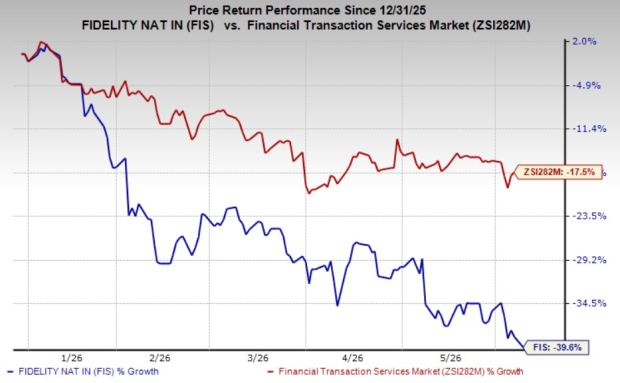

FIS’ Price Performance

Shares of Fidelity National have declined 39.6% year to date, underperforming the 17.5% fall of the industry.

Zacks Rank & Key Picks

FIS currently has a Zacks Rank #3 (Hold).

Some better-ranked stocks from the broader Business Services space are Klarna Group plc KLAR, Paymentus Holdings, Inc. PAY and Repay Holdings Corporation RPAY, each carrying a Zacks Rank #2 (Buy) at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

The Zacks Consensus Estimate for Klarna’s current-year earnings indicates a 105.1% year-over-year improvement. KLAR has witnessed four upward estimate revisions over the past month against no movement in the opposite direction. The consensus estimate for current-year revenues is pegged at $4.44 billion, indicating 26.5% year-over-year growth.

The Zacks Consensus Estimate for Paymentus’ current-year earnings indicates a 19.7% year-over-year jump. PAY beat earnings estimates in each of the trailing four quarters, with the average surprise being 12%. The consensus estimate for current-year revenues implies 19.9% year-over-year growth.

The consensus estimate for Repay Holdings’ current-year earnings indicates an 11% year-over-year increase. It has witnessed one upward estimate revision and no downward movement over the past 60 days. The consensus estimate for RPAY’s current-year revenues is pegged at $342.39 million, implying 10.7% year-over-year growth.

Beyond Nvidia: AI's Second Wave Is Here

The AI revolution has already minted millionaires. But the stocks everyone knows about aren't likely to keep delivering the biggest profits. AI’s second wave is moving from infrastructure to implementation and these companies are at the forefront of this transition, positioned to become what Amazon and Google were to the internet era.

See Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Paymentus Holdings, Inc. (PAY): Free Stock Analysis Report

Fidelity National Information Services, Inc. (FIS): Free Stock Analysis Report

Repay Holdings Corporation (RPAY): Free Stock Analysis Report

Klarna Group plc (KLAR): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).