Ciena Corporation CIEN stock has declined approximately 13% since its second-quarter fiscal 2026 results were reported on June 4, 2026.

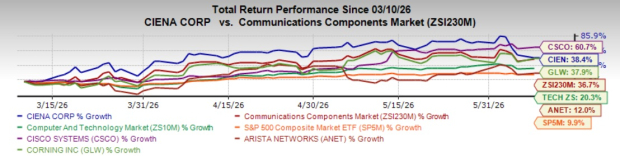

Shares of the company have declined 19.7% in the past month, underperforming the Zacks Computer & Technology sector and the Zacks Communication - Components industry, which decreased 0.2% and 14.9%, respectively. The S&P 500 composite is down 0.6% over the same time frame. The company’s shares have surged 38.4% in the past three months.

CIEN has outperformed its peers, Corning Incorporated GLW and Arista Networks, Inc. ANET but underperformed Cisco Systems, Inc. CSCO. GLW and ANET have climbed 37.9% and 12%, respectively, while CSCO has gained 60.7% in the past three months.

Image Source: Zacks Investment Research

Investors may wonder whether CIEN has further downside risk or if its underlying fundamentals can help stabilize the stock. Let’s examine the company’s strengths, operational challenges and growth outlook to determine the best course of action.

CIEN’s Q2 Earnings Snapshot

Ciena reported fiscal second-quarter 2026 adjusted earnings of $1.64 per share, surpassing the Zacks Consensus Estimate of $1.46. The bottom line soared 290% year over year, driven by accelerating AI-led network investments.

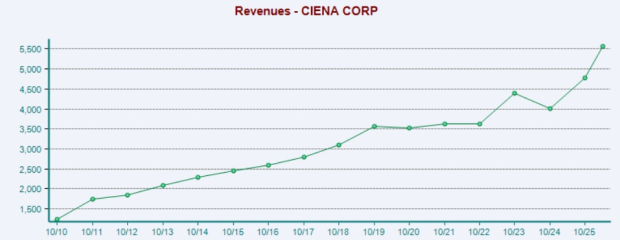

Quarterly revenues increased 39.5% from the year-ago quarter to $1.57 billion, topping the consensus estimate of $1.50 billion, supported by record sales, robust cloud demand and strong adoption of optical networking solutions.

Management expects fiscal third-quarter 2026 revenues of $1.625 billion (+/-$50 million). The company also raised its fiscal 2026 revenue guidance to $6.3 billion (+/-$100 million), implying approximately 32% year-over-year growth at the midpoint. Management attributed the improved outlook to continued AI infrastructure investments and sustained demand for its optical networking solutions.

Image Source: Zacks Investment Research

Key Factors to Consider

Ciena is benefiting from AI-led demand across cloud and service providers, its technology leadership, deep customer relationships and a broad portfolio spanning systems, interconnects, software and services. The company’s revenues grew in the second quarter, its adjusted gross margin expanded and adjusted earnings per share nearly quadrupled. Management stated that a strong and growing backlog, together with its leading technology portfolio, provides strong visibility and positions the company to capture long-term opportunities across WAN and data center networking.

The company is also gaining momentum from increasing investments by hyperscalers and service providers in network infrastructure. The company noted that all customers are prioritizing high-capacity, low-latency and high-speed connectivity to support AI model training, data ingestion and inference. Its addressable market is expected to nearly double to around $50 billion by 2029, supported by growth in both traditional WAN markets and high-growth data center opportunities. Service provider revenues increased 28% year over year, while India service provider revenues more than doubled, reflecting strong managed optical fiber network deployments.

Ciena continues to benefit from demand for its latest networking solutions and expanding customer engagements. Ciena announced the industry's first multi-rail order for its RLS Hyper-Rail platform from a leading hyperscaler and is engaged in discussions with multiple additional hyperscalers, neoscalers and service providers. Its DCOM solution contributed to 88% year-over-year growth in the Routing and Switching segment, while initial orders from a second hyperscaler and lab qualifications with a third customer further expanded its customer base. The company also secured a new hyperscaler win for its coherent modules and remains on track to more than double pluggable revenues compared with 2025.

Ciena is further advancing from customer co-creation initiatives and operational execution. Management stated that customers involve the company early in developing new architectures, helping improve road map decisions, increase win rates and provide greater demand visibility. In the second quarter of fiscal 2026, the company achieved free cash flow of $219 million and a cash balance of $1.4 billion, while adjusted gross margin improved through engineering cost reductions, product mix and pricing optimization. Backlog increased by more than $600 million sequentially to $7.7 billion, supported by strong order flows and customer collaboration, providing visibility into 2027.

However, Ciena continues to operate in a supply-constrained environment where demand is exceeding available supply, prompting the company to invest additional capital and operating expenses to secure future manufacturing capacity and supply security. Management also noted ongoing constraints in modem components and laser pumps used in amplifiers and line systems, while inflationary pressures and higher variable compensation tied to stronger performance are increasing operating expenses, leading the company to make additional investments to support future demand.

CIEN’s Valuation

CIEN trades at a forward 12-month price-to-earnings (P/E) of 67.87X, above the industry’s 50.96X. CSCO, GLW and ANET trade at a forward 12-month P/E of 32.09X, 51.75X and 43.8X, respectively.

Image Source: Zacks Investment Research

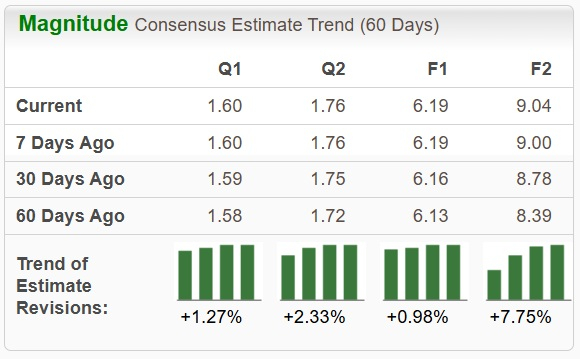

CIEN’s Upward Estimates

The Zacks Consensus Estimate for CIEN’s earnings for fiscal 2026 has been revised marginally upward over the past 30 days.

Image Source: Zacks Investment Research

What Should You Do With CIEN Stock Now?

Despite the recent pullback and a premium valuation, Ciena’s strong AI-driven demand, expanding backlog, improving profitability, raised fiscal 2026 outlook and growing opportunities across cloud and optical networking support its long-term prospects.

Existing investors should hold the stock, while new investors may wait for a better entry point before initiating a position.

CIEN currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power .

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Cisco Systems, Inc. (CSCO): Free Stock Analysis Report

Ciena Corporation (CIEN): Free Stock Analysis Report

Corning Incorporated (GLW): Free Stock Analysis Report

Arista Networks, Inc. (ANET): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).