Mission Produce Inc. AVO posted second-quarter fiscal 2026 results, wherein the bottom line missed the Zacks Consensus Estimate, but the top line surpassed the same. Meanwhile, earnings and revenues declined year over year.The company reported adjusted earnings of 1 cent compared with 12 cents in the year-ago quarter and missed the consensus estimate of 5 cents.Mission Produce, Inc. Price, Consensus and EPS Surprise

Mission Produce, Inc. price-consensus-eps-surprise-chart | Mission Produce, Inc. Quote

Results benefited from strong avocado volume growth and solid commercial execution in a low-price environment, which helped support customer demand and expand category consumption. However, profitability was pressured by a sharp decline in avocado pricing and a late-quarter mismatch in supply and demand for core fruit sizes that compressed per-unit margins, particularly in April. The quarter also reflected acquisition-related transaction advisory costs tied to the Calavo deal, while management noted pricing and margin conditions improved exiting the period.

Insight Into AVO’s Q2 Performance

Revenues of $290.9 million in second-quarter fiscal 2026 declined 24% year over year but surpassed the consensus estimate of $269 million. The decline was due to a 36% decline in average avocado pricing, partially offset by 15% higher avocado volumes.

In second-quarter fiscal 2026, the company’s adjusted EBITDA was $7.1 million, down 62.8% from $19.1 million in second-quarter fiscal 2025. Gross profit of $20.5 million declined 27.8% year over year. Gross margin decreased by 50 basis points year over year to 7.0% of revenues.

In the Marketing & Distribution segment, gross profit was adversely affected by historically low avocado prices and a supply-demand imbalance for core fruit sizes during April, which further compressed per-unit margins. Gross profit in the International Farming segment also declined, primarily due to lower volumes of blueberry packing and storage services resulting from reduced harvest yields, as well as higher per-unit mango production costs.

SG&A of $21.1 million (excluding transaction advisory costs) was essentially unchanged from the prior-year quarter. Transaction advisory costs totaled $6.4 million in the quarter and consisted mainly of third-party legal, due diligence and other fees related to the Calavo acquisition, which closed on May 28, 2026.

Avocado operating metrics: 191.5 million pounds sold (up 15% y/y) at an average sales price of $1.29 per pound (down 35.5% y/y from $2.00).

AVO’s Segment Mix Highlights

Marketing & Distribution: The segment sales were $277.2 million, down 23.5% from $362.5 million a year ago, reflecting a sharp decline in avocado pricing that more than offset higher shipment volumes.

The segment posted an operating loss of $3.8 million (including transaction advisory costs) versus an operating income of $7.6 million in the prior-year quarter. Segment adjusted EBITDA was $7.2 million, a 57.1% decline from $16.8 million last year, mainly due to weaker per-unit gross margins.

International Farming: The segment sales were $7.7 million, down 4.9% from $8.1 million a year earlier.

The segment recorded an operating loss of $3.9 million compared with an operating loss of $1.3 million last year. Segment adjusted EBITDA was a loss of $1.3 million versus a positive $1.5 million in the year-ago quarter, reflecting a $2.8 million deterioration. Management attributed the weaker performance mainly to higher per-unit mango production costs and lower blueberry packaging and storage service volumes.

Blueberries: The segment sales were $11.0 million, down 29.9% from $15.7 million a year ago. The decline was mainly due to lower volume sold, partially offset by a higher average selling price per unit.

Segment operating income improved to $0.7 million, up 16.7% from $0.6 million last year. Segment adjusted EBITDA rose to $1.2 million, a 50.0% increase from $0.8 million, driven by the stronger per-unit pricing. That benefit was partly offset by lower per-acre yields, which increased per-unit production costs.

AVO’s Other Financials

Cash and cash equivalents were $33 million as of April 30, 2026 (down from $64.8 million as of Oct. 31, 2025). Net cash used in operating activities totaled $21.0 million for the six months ended April 30, 2026, compared with $13.0 million used in the prior-year period. The higher cash outflow primarily reflected weaker profitability in the current year, partly offset by a smaller working-capital build than last year. Capital expenditures were $22.9 million in the quarter versus $28 million a year earlier.

The increase in working capital this year was mainly tied to higher trade receivables, driven by seasonal patterns and the timing of sales in the Marketing & Distribution and Blueberries segments. Inventory also rose, reflecting higher volumes in Marketing & Distribution and the build of growing-crop inventory within the International Farming and Blueberries segments.

Mission Produce’s board authorized a new share repurchase program on June 3, 2026, allowing the company to buy back up to $100 million of common stock over the next 36 months. The plan replaces the prior program from September 2023, which was set to expire in September 2026, with about $11.2 million still available. No shares were repurchased under the new program through June 8, 2026.

Other Developments

Mission Produce completed its acquisition of Calavo Growers on May 28, 2026. The deal adds Calavo’s fresh produce and value-added prepared foods portfolio, strengthens Mission’s year-round avocado supply position in North America, and expands the company into the prepared foods category with potential upside from cost synergies and SG&A savings.

AVO’s Near-Term Outlook

For the third quarter of fiscal 2026, Mission Produce expects avocado industry volumes to increase 5-10% year over year. The company also anticipates exportable avocado production from its owned Peru farms of 120-130 million pounds, up from 105 million pounds in the fiscal third quarter of 2025, with sales of that owned production expected to be weighted toward the fiscal fourth quarter.

Management also expects pricing to be down about 15% year over year versus the $1.75 per pound average realized in the third quarter of fiscal 2025, citing higher anticipated volumes across U.S. and international markets.

Including the newly acquired Calavo business, Mission Produce guided fiscal third-quarter 2026 adjusted EBITDA to $28-$32 million, reflecting a partial-quarter contribution from Calavo, later-timed Peru farming contribution versus last year and lingering margin-compression impacts from the second quarter that continued at the beginning of the third quarter. For the second half of fiscal 2026, adjusted EBITDA is projected at $84-$88 million, supported by a full quarter of Calavo in the fourth quarter of 2025, stabilizing avocado margin dynamics and improved blueberry volumes on better yields. Synergies from Calavo are expected to begin materializing in the fiscal fourth quarter and build thereafter, with related expenses planned to be added back to adjusted EBITDA and adjusted net income alongside quarterly updates.

Full-year fiscal 2026 capital expenditures are expected to be approximately $45 million, including planned spending tied to the legacy Calavo business.

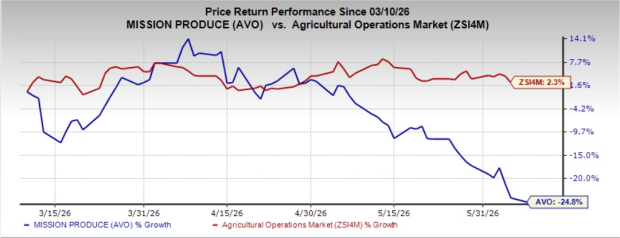

Shares of this Zacks Rank #3 (Hold) company have lost 24.8% in the last three months against the industry’s growth of 2.3%.

AVO stock's Price Performance

Image Source: Zacks Investment Research

Stocks to Consider

The Chef's Warehouse, Inc. CHEF, a specialty food distributor serving restaurants, hotels and hospitality customers, carries a Zacks Rank #2 (Buy) at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

The Zacks Consensus Estimate for The Chef's Warehouse’s current financial-year sales and earnings indicates growth of 8.3% and 24.7%, respectively, from the prior-year reported levels. CHEF delivered a trailing four-quarter earnings surprise of 28.9%, on average.

B&G Foods BGS is a branded packaged-food company that manufactures, markets, and distributes a portfolio of shelf-stable and frozen food products. BGS carries a Zacks Rank #2.

The Zacks Consensus Estimate for B&G Foods’ current and next financial-year earnings indicates year-over-year growth of 11.8% and 15.8%, respectively.

AmbeV S.A. ABEV is a beverage company that produces and distributes beer, draft beer, soft drinks and other beverages across the Americas. ABEV currently has a Zacks Rank #2.

The Zacks Consensus Estimate for Ambev’s 2026 sales and earnings implies growth of 19.2% and 16.7%, respectively, from the previous year’s reported numbers.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power .

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

B&G Foods, Inc. (BGS): Free Stock Analysis Report

The Chefs' Warehouse, Inc. (CHEF): Free Stock Analysis Report

Ambev S.A. (ABEV): Free Stock Analysis Report

Mission Produce, Inc. (AVO): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).