Shares of Accenture plc ACN have had a decent run over the past month. The stock has risen 1.2% compared with the industry's 1.9% growth. The Zacks S&P 500 composite declined 0.8% during the said time frame.

ACN has a Growth Score of A. This style score condenses key financial metrics to reflect a fair sense of the quality and sustainability of its growth.

The company’s third-quarter fiscal 2026 earnings are expected to increase 6.6% year over year. Earnings for fiscal 2026 and fiscal 2027 are projected to rise 7.4% and 7.7%, respectively, year over year. Revenues are expected to increase 6.6% in fiscal 2026 and 5.3% in fiscal 2027.

Factors That Bode Well for ACN

Accenture is benefiting from robust demand for application modernization and maintenance, cloud enhancements and cybersecurity. The company reported that revenues increased 8% year over year to $18 billion during the second quarter of fiscal 2026, driven by broad-based growth across geographic regions and service offerings. The Asia Pacific region delivered the strongest growth during the said time frame, with revenues increasing 10% in local currency. Revenues from the Americas grew 3%, while Europe, the Middle East and Africa posted 2% growth.

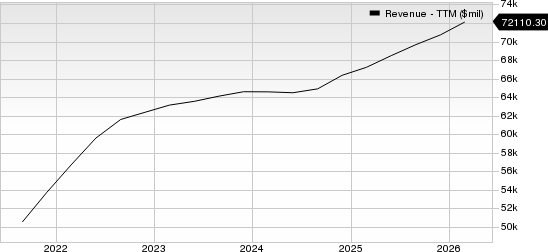

Accenture PLC Revenue (TTM)

Accenture PLC revenue-ttm | Accenture PLC Quote

The worldwide artificial intelligence (AI) boom also drives growth opportunities for ACN. The management highlighted growing demand from clients seeking to integrate advanced AI capabilities into core business processes. The company is employing more than 85,000 AI and data professionals, exceeding its fiscal 2026 target ahead of schedule. ACN reported that more than 100 additional clients initiated advanced AI engagements during the last reported quarter, creating a significant growth opportunity.

Accenture pursues acquisitions, partnerships and strategic investments as key drivers for long-term growth. It invested $1.6 billion in acquisitions during the second quarter of fiscal 2026 and expects to deploy approximately $5 billion toward acquisitions during fiscal 2026. The company recently acquired Faculty, a U.K.-based AI-native services company with a decision-intelligence platform and a majority stake in DLB Associates, a fast-growing data center engineering and consulting firm.

ACN expanded its relationship with Palantir, a data analytics platform provider, through the acquisition of Decho and RANGR Data. Decho is a U.K.-based technology and AI consultancy that helps organizations reinvent through the design, delivery and scaling of Palantir solutions. RANGR Data is a U.S.-based certified Palantir partner with deep experience in driving scaled transformation through a client-centric approach.

The company has a consistent track record of dividend payments. It paid dividends of $3.7 billion, $3.2 billion, $2.8 billion and $2.5 billion in fiscal 2025, 2024, 2023 and 2022, respectively. Such moves indicate its commitment to returning value to shareholders and underline its confidence in business.

Key Risks to Watch

ACN faces stiff competition from strong companies such as Genpact Limited, Cognizant Technology Solutions and Infosys. This tough competition, along with the limited scope for product differentiation, makes renegotiating large contracts increasingly important and creates pricing pressure on ACN.

ACN is witnessing growing cost pressures as operating expenses continue to rise. Total operating costs increased 5.9% in fiscal 2023, remained elevated in fiscal 2024 despite being flat and rose another 7.5% in fiscal 2025, highlighting persistent cost intensity. This trend underscores the need for tighter cost controls to prevent expenses from outpacing revenue growth and eroding profitability. Total operating expenses climbed a further 7.9% year over year in the second quarter of fiscal 2026, reinforcing near-term margin concerns.

Accenture currently carries a Zacks Rank of #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Stocks to Consider

A couple of better-ranked stocks in the broader Zacks Computer and Technology sector are Cisco Systems CSCO and Dell Technologies DELL.

Cisco Systems carries a Zacks Rank #2 (Buy) at present. It has a long-term (next five years) earnings growth expectation of 11.1%.

CSCO delivered a trailing four-quarter earnings surprise of 2%, on average.

Dell Technologies sports a Zacks Rank of 1 at present. It has a long-term earnings growth expectation of 26.4%.

DELL surpassed the Zacks Consensus Estimate in each of the trailing four reported quarters, with an average earnings surprise of 18.7%.

Radical New Technology Could Hand Investors Huge Gains

Quantum Computing is the next technological revolution, and it could be even more advanced than AI.

While some believed the technology was years away, it is already present and moving fast. Large hyperscalers, such as Microsoft, Google, Amazon, Oracle, and even Meta and Tesla, are scrambling to integrate quantum computing into their infrastructure.

Senior Stock Strategist Kevin Cook reveals 7 carefully selected stocks poised to dominate the quantum computing landscape in his report, Beyond AI: The Quantum Leap in Computing Power .

Kevin was among the early experts who recognized NVIDIA's enormous potential back in 2016. Now, he has keyed in on what could be "the next big thing" in quantum computing supremacy. Today, you have a rare chance to position your portfolio at the forefront of this opportunity.

See Top Quantum Stocks Now >>Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Accenture PLC (ACN): Free Stock Analysis Report

Cisco Systems, Inc. (CSCO): Free Stock Analysis Report

Dell Technologies Inc. (DELL): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).