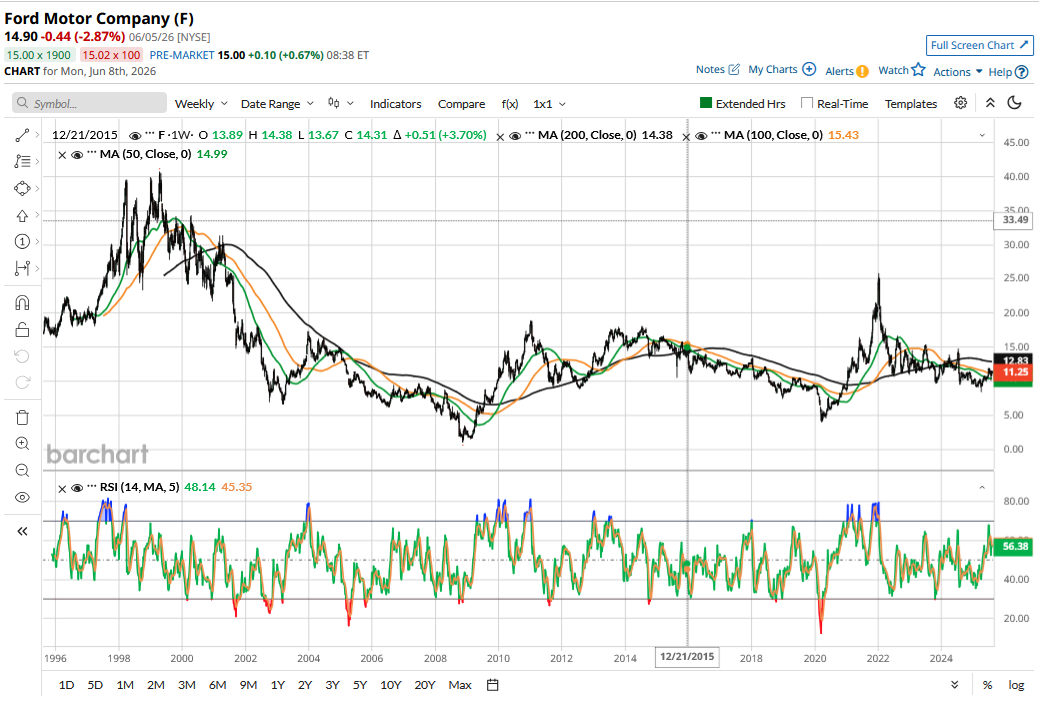

While Detroit rival General Motors (GM) fell by just over 1% last week, Ford (F) lost nearly 15%. The price action of the two stocks has diverged in recent weeks, particularly since Ford announced a foray into the energy storage business in May.

While energy storage might not be a hot business otherwise, the sector is seen as a play on artificial intelligence (AI). Hyperscalers have been signing massive power purchase agreements to ensure their power-guzzling data centers have sufficient energy. Since data centers cannot afford any power disruption, they also need energy storage systems to maintain 100% uptime and navigate grid constraints.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

www.barchart.com

www.barchart.com AI Stocks Fell Last Week

Ford’s energy storage announcement came at a time when the euphoria toward AI was gaining traction. However, the AI trade came under pressure last week, and names like Nvidia (NVDA) and Micron (MU) plunged on June 5. Since Ford’s recent rally was largely driven by optimism about its energy storage business and the participation of the "Blue Oval" in the AI ecosystem, Ford came under selling pressure last week.

Back in late May, I noted that while Ford’s energy storage business looks positive for the company, F stock had run ahead of its fundamentals. Now, let's take a look at whether Ford shares have entered the buy zone following the recent correction.

Ford’s Legacy Business Continues to Do Well

To begin, let’s dive into Ford’s current business. The company expects to post adjusted earnings before interest and taxes (EBIT) between $8.5 billion and $10.5 billion this year. Ford Pro, the company’s commercial business, remains a mainstay of its profitability, and the company expects the segment’s adjusted EBIT to be between $6.5 billion and $7.5 billion this year. For Ford Blue, the legacy internal combustion engine (ICE) business, the metric is expected to be between $4.5 billion and $5 billion. Finally, Ford projected $2.5 billion adjusted EBIT for its credit arm while forecasting electric vehicle (EV) losses to be between $4 billion and $4.5 billion.

Ford’s EV business has long been a drag on profitability, and while the segment’s losses have come off the peak, they are still high for comfort. The current guidance calls for a quarterly pre-tax loss in the ballpark of $1 billion.

Ford has made several changes to its EV business and adjusted production to align it with tepid demand. The firm announced a massive $19.5 billion write-down in its EV business last year, which was much higher than GM but below Stellantis (STLA). In April, Doug Field — Ford’s chief EV, digital, and design officer — departed the company after five years. Ford also announced a new Product Creation and Industrialization segment headed by Chief Operating Officer Kumar Galhotra.

Ford has revamped its EV strategy and shifted focus to profitability. It is looking to build a $30,000 electric pickup truck, touting the new platform as the “next Model T." These vehicles will be available in showrooms next year, and Ford expects the new models to be profitable from the get-go.

It remains to be seen whether Ford can win over buyers with the new models, but the company’s track record in EVs does not leave much to talk about, as even the electric F-150 — whose ICE equivalent has been the best-selling gas pickup in the U.S. for years — failed to cut ice with buyers.

Where Does Energy Storage Fit Into Ford’s Strategy?

The energy storage business holds a lot of promise considering the expected bump from AI power demand. Morgan Stanley analyst Andrew Percoco believes that Ford’s partnership with China’s Contemporary Amperex Technology (CYATY) is its “underappreciated strategic competitive advantage.”

Morgan Stanley expects Ford's energy storage business to generate pre-tax profits of $588 million at 20 GWh annual production, at which point it predicts it would have a $10 billion enterprise value based on its assumption of a pre-tax earnings multiple of 17.5 times.

Is Ford Stock a Buy After the Recent Correction?

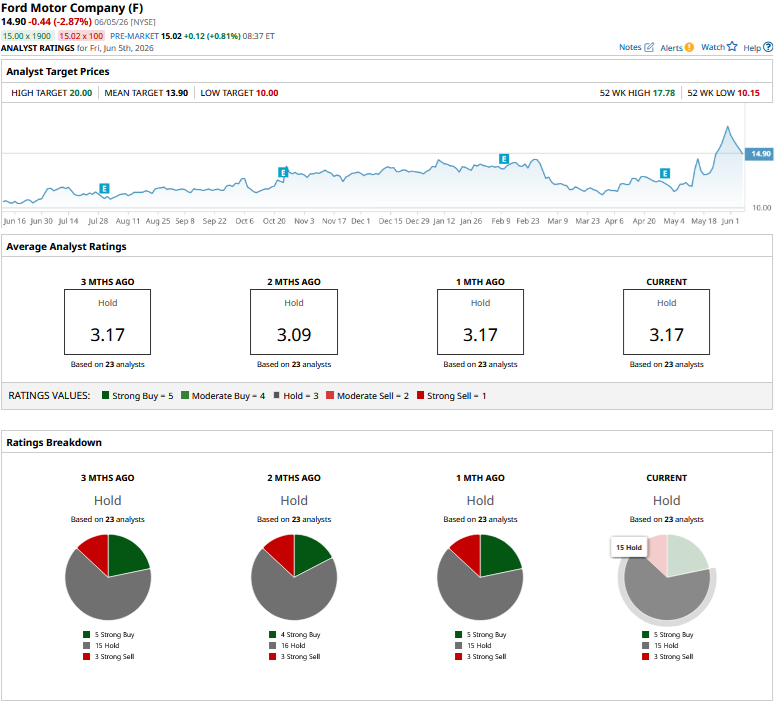

While Ford still trades ahead of its mean target price of $13.90, sell-side analysts have been raising their target prices lately to bake in the company’s nascent energy business. Late last month, Bank of America analyst John Murphy raised his F stock price target to a Street-high of $20. Similarly, Citigroup analyst Michael Ward raised his target to $19 earlier this month.

While there is optimism over Ford's energy storage business, the company has to deliver on execution, something it hasn't really impressed with in recent years. From a valuation perspective, F stock trades at a forward price-to-earnings (P/E) multiple of 9.1 times while the 2027 P/E is closer to 8 times. I see the risk-reward as a lot more balanced here, even though I still don’t find the valuations compelling enough to buy shares.

www.barchart.com

www.barchart.com On the date of publication, Mohit Oberoi had a position in: F , GM , NVDA . All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

RIVN Stock Alert: What to Know as Rivian Begins Deliveries of R2 EV Apple Kicks Off WWDC. How to Play AAPL Stock Here. This Newly Listed Closed-End Fund Just Revealed SpaceX as Its Top Holding at $117 Million. Ford’s AI Euphoria Just Faced a Reality Check. How to Play F Stock After the Dip.