BGC Group, Inc. BGC exited the first quarter of 2026 with liquidity of $878.4 million, consisting of cash and equivalents plus financial instruments owned at fair value. That was down from $979.1 million at year-end 2025, largely reflecting year-end bonus and tax payments and normal timing between first-quarter commissions earned and fourth-quarter collections. Cash and segregated cash ended the quarter at $803.1 million.

That liquidity backdrop matters because it keeps BGC’s capital return options open even as working-capital needs fluctuate through the year. The company also reported cash and cash equivalents of $781 million as of March 31, 2026, alongside total assets of $5.9 billion and stockholders’ equity of $1.1 billion, reinforcing balance-sheet capacity to support capital distributions.

BGC Global is pairing that flexibility with a sizable authorization. In November 2025, management authorized a $400 million share repurchase program. As of March 31, 2026, $386.9 million remained available, and management expects repurchases to increase as seasonal cash uses abate.

BGC Group’s Dividend Adds a Baseline Yield

Alongside buybacks, BGC has maintained a regular quarterly dividend of 2 cents per share since June 2024. That dividend establishes a baseline shareholder return while leaving more room for repurchases to flex with cash generation and market conditions.

The most recent declaration kept that cadence intact. On May 6, BGC announced a quarterly dividend of 2 cents per share, payable June 10 to Class A and Class B stockholders of record as of May 27.

Dividend

Image Source: Zacks Investment Research

For context, many market-structure peers lean heavily on recurring payouts. CME Group CME, for example, pairs a regular dividend with additional variable distributions, while Tradeweb Markets TW has emphasized share repurchases as a way to return capital. Against that backdrop, BGC’s dividend looks steady, but the buyback is positioned as the larger lever.

BGC’s Cost Program Is a Real, Dated Catalyst

BGC Global is not relying on revenue growth alone to lift profitability. The company launched a cost-reduction program in 2025 with $25 million of annualized savings and later expanded the target to $35 million.

The actions are specific and tied to core cost lines. The program targets compensation and infrastructure costs and includes the closure of a loss-making logistics business. Management also expects to keep identifying and executing additional savings initiatives through 2026.

This is central to the margin narrative. The combination of disciplined cost actions and scaling electronic platforms is positioned to drive positive operating leverage, where incremental revenue contributes more meaningfully to earnings as fixed costs are absorbed.

BGC Group’s Expenses Are Rising With Investment

The key risk case is that expenses keep running ahead of the operating leverage story. Total expenses have been steadily increasing over the last three years, and that trend continued in the first quarter of 2026.

Compensation and employee benefits are a focal point. Even with the $35 million annualized cost target, compensation and benefit expenses are expected to rise as revenues improve.

Non-compensation pressures also matter. Continued investments in franchises, new product and service launches, higher marketing spend, technology upgrades, and evolving regulation are all expected to keep expenses elevated as the platform expands. That mix can mute the benefit of revenue growth if spending scales in parallel.

BGC’s Q1 2026 Shows Both Sides at Once

The first-quarter 2026 results show why the debate is so live. Revenues jumped 43.8% year over year to $955.5 million. Adjusted earnings per share rose 41.4% to 41 cents and pre-tax adjusted earnings increased 44.9% to $232.1 million, producing a 24.3% pre-tax adjusted margin.

BGC Group, Inc. Price, Consensus and EPS Surprise

BGC Group, Inc. price-consensus-eps-surprise-chart | BGC Group, Inc. Quote

At the same time, expense growth remained heavy. Total expenses for adjusted earnings were $725 million, up 43.7% year over year. For adjusted earnings, compensation rose 51.5%, and non-compensation expenses increased 27.4%.

That is the near-term investor decision point: BGC must keep translating growth into incremental margin, not just headline revenue. The buyback can amplify per-share results over time, but execution still needs to show that scaling platforms and cost actions are outpacing the investment cycle.

BGC Group’s Near-Term Trading Call: Rank and Style

BGC currently carries a Zacks Rank #3 (Hold). Its Style Scores are Value A, Growth B, Momentum F, and VGM B. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

That combination frames the setup clearly. The stock screens as value-tilted with supportive growth characteristics, but weaker momentum signals suggest the near-term tape may remain choppy.

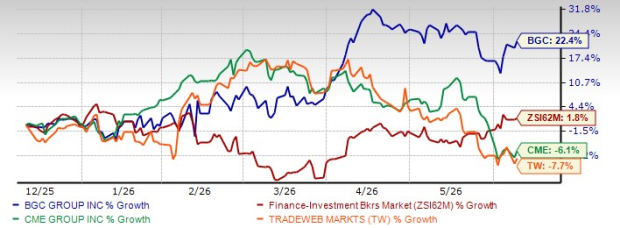

Over the past six months, BGC shares have soared 22.4%, outperforming the industry’s gain of 1.8%. The stock has also fared better than CME Group and Tradeweb Markets in the same time frame.

Six-Month Price Performance

Image Source: Zacks Investment Research

For investors, the practical takeaway is fit. Value-oriented holders may focus on capital return capacity and the cost program’s margin potential, while more momentum-driven profiles may want clearer evidence that expense growth is easing and operating leverage is strengthening through 2026.

Research Chief Names "Single Best Pick to Double"

From thousands of stocks, 5 Zacks experts each have chosen their favorite to skyrocket +100% or more in months to come. From those 5, Director of Research Sheraz Mian hand-picks one to have the most explosive upside of all.

This company targets millennial and Gen Z audiences, generating nearly $1 billion in revenue last quarter alone. A recent pullback makes now an ideal time to jump aboard. Of course, all our elite picks aren’t winners but this one could far surpass earlier Zacks’ Stocks Set to Double like Nano-X Imaging which shot up +129.6% in little more than 9 months.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

CME Group Inc. (CME): Free Stock Analysis Report

BGC Group, Inc. (BGC): Free Stock Analysis Report

Tradeweb Markets Inc. (TW): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).