United Natural Foods, Inc. UNFI reported third-quarter fiscal 2026 results, wherein the top line declined year over year but the bottom line improved. However, both metrics missed the Zacks Consensus Estimate.

United Natural posted adjusted earnings of 77 cents per share for the fiscal third quarter, missing the Zacks Consensus Estimate of 81 cents. However, the adjusted earnings per share increased 75% year over year from 44 cents.

United Natural Foods, Inc. Price, Consensus and EPS Surprise

United Natural Foods, Inc. price-consensus-eps-surprise-chart | United Natural Foods, Inc. Quote

Net sales decreased 4.2% year over year to $7,723 million, missing the Zacks Consensus Estimate of $7,882 million. The decline included an approximate 450-basis-point impact from accretive optimization actions. Results were also affected by the initial unwind of previously referenced short-term project work for a single customer.

UNFI’s Quarterly Performance by Division

A key feature of the quarter was the divergence between Natural and Conventional trends. Natural segment sales increased 4.4% year over year to $4,342 million, reflecting continued demand for natural, organic, fresh and specialty products.

By contrast, Conventional sales declined 13.6% to $3,136 million, largely tied to the company’s accretive optimization actions and portfolio reshaping. Retail sales decreased 10.1% to $515 million, with management pointing to planned store closures as part of ongoing footprint optimization.

Analysis of UNFI’s Costs & Margins

UNFI’s gross profit fell 3% year over year to $1,049 million. The gross profit margin was 13.6%, which expanded 20 bps from 13.4% reported in the year-ago quarter. This expansion was driven by benefits from network optimization and a favorable customer mix, partially offset by a lower gross margin rate in the Retail segment.

Operating expenses declined to $954 million from $1,025 million in the prior-year quarter, and the operating expense as a percentage of sales improved to 12.4% of net sales from 12.7%. The company attributed the rate improvement to insurance proceeds and the benefits of cost-saving initiatives, including network optimization and higher distribution-center productivity.

Adjusted EBITDA increased 16.6% year over year to $183 million from $157 million. Adjusted EBITDA margin also expanded by approximately 40 basis points to 2.4% of net sales.

United Natural’s Financial Position

UNFI generated free cash flow of $54 million in the quarter. Net cash provided by operating activities totaled $98 million, while payments for capital expenditures were $44 million.

Balance-sheet progress remained a focal point. Net debt at the end of the quarter was $1.63 billion, and the net leverage ratio improved to 2.5x, which management characterized as the lowest level since fiscal 2018. Liquidity was approximately $1.25 billion, which consisted of $43 million in cash and about $1.20 billion of available capacity under the company’s asset-based lending facility. The company also repurchased 82,233 shares, with an average price of $48.64 for approximately $4 million.

UNFI Maintains FY26 Midpoints, Narrows Key Metrics Range

Looking ahead, UNFI reiterated fiscal 2026 outlook midpoints and narrowed ranges across several metrics. The company now expects net sales in the range of $31.1-$31.3 billion for fiscal 2026, down from the prior range of $31-$31.4 billion.

UNFI expects adjusted EBITDA to be in the range of $685-$705 million compared with the previous guidance of $680-$710 million and net income is now expected to be in the range of $55-$70 million compared with the previous guidance of $50-$75 million.

Adjusted earnings are expected to be in the range of $2.40-$2.60 per share compared with the previous guidance of $2.30-2.70. Capital expenditures are expected to be $250 million, and free cash flow is expected to be $330 million.

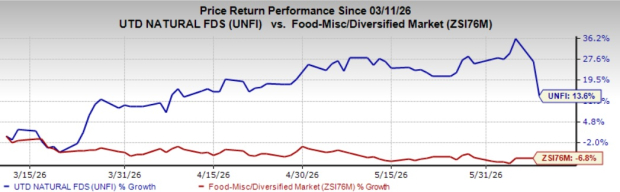

Shares of this Zacks Rank #3 (Hold) company have risen 13.6% in the past three months against the industry’s decline of 6.8%.

Image Source: Zacks Investment Research

Stocks to Consider

Some better-ranked stocks have been discussed below:

The Chef’s Warehouse, Inc. CHEF distributes specialty food and center-of-the-plate products in the United States, the Middle East, and Canada. CHEF currently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for CHEF’s current fiscal-year sales and earnings indicates growth of 8.3 and 24.7%, respectively, from the year-ago reported figures. CHEF delivered a trailing four-quarter earnings surprise of 28.9%, on average.

Armanino Foods of Distinction, Inc. AMNF produces and markets frozen food products in the United States. AMNF currently carries a Zacks Rank #2 (Buy).

The Zacks Consensus Estimate for Armanino Foods' current fiscal-year sales and earnings indicates growth of 7% and 1.7%, respectively, from the year-ago actuals. AMNF delivered a trailing four-quarter earnings surprise of 23.1%, on average.

Medifast, Inc. MED operates as a health and wellness company that provides habit-based and coach-guided lifestyle solutions to address obesity and support a healthy life in the United States. MED currently carries a Zacks Rank #2.

The Zacks Consensus Estimate for Medifast's current fiscal-year sales and earnings implies a decline of 25.9% and 140.2%, respectively, from the year-ago actuals. MED delivered a trailing four-quarter negative earnings surprise of 635.6%, on average.

Zacks' Research Chief Names "Stock Most Likely to Double"

Our team of experts has just released the 5 stocks with the greatest probability of gaining +100% or more in the coming months. Of those 5, Director of Research Sheraz Mian highlights the one stock set to climb highest.

This top pick is a little-known satellite-based communications firm. Space is projected to become a trillion dollar industry, and this company's customer base is growing fast. Analysts have forecasted a major revenue breakout in 2025. Of course, all our elite picks aren't winners but this one could far surpass earlier Zacks' Stocks Set to Double like Hims & Hers Health, which shot up +209%.

Free: See Our Top Stock And 4 Runners UpWant the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

United Natural Foods, Inc. (UNFI): Free Stock Analysis Report

The Chefs' Warehouse, Inc. (CHEF): Free Stock Analysis Report

MEDIFAST INC (MED): Free Stock Analysis Report

Armanino Foods of Distinction Inc. (AMNF): Free Stock Analysis Report

This article originally published on Zacks Investment Research (zacks.com).