Flex (FLEX) stock has made some big moves this year, witnessing a return of 216% in the last 52 weeks. The most recent news generating interest is the company's upcoming inclusion in the S&P 500 Index ($SPX) later this month. Scheduled for June 22, this impending event holds a great deal of importance, as it implies greater interest from institutional investors.

Of course, this is not the only factor to consider with FLEX stock. On May 5, Flex announced that its cloud and power infrastructure segment will be spun off as a separate entity. The new entity will be focused on “delivering end-to-end power and thermal management technologies.” With AI data centers as a key market, the potential spinoff is likely to unlock significant value.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Flex has already provided some initial guidance that has excited the markets. For fiscal 2027, the spun-off entity is expected to deliver top-line growth in the range of 65% to 75%. Further, Flex expects growth to accelerate to more than 80% in fiscal 2028.

For Flex post-spinoff, the expectation is low-to-mid-single-digit growth. At the same time, the firm expects its two segments to deliver margin expansion and cash flow upside in the coming years. Given the outlook for both businesses, FLEX stock seems attractive even after a meaningful rally.

About Flex Stock

Headquartered in Austin, Texas, Flex is a provider of design and engineering, supply chain, manufacturing, and integrated services, coupled with a portfolio of power and cooling products. The company’s customers come from a diverse set of industries, including data centers, healthcare, industrial, automotive, and communications, among others.

As of March 2026, Flex had three reportable segments: Integrated Technology Solutions, Regulated Manufacturing Solutions, and Cloud and Power Infrastructure. As of fiscal 2026, the company was well diversified from a geographic perspective, with 44% of net sales in North America, 16% in China, 20% in Europe, and 20% in other areas.

For fiscal 2026, Flex reported revenue growth of 8% year-over-year (YOY) to $27.9 billion. For the same period, adjusted operating income was $1.76 billion, which implied a margin of 6.3%. Considering multiple catalysts, the price action of FLEX stock has been significant, with shares rallying 92% in the last six months.

www.barchart.com

www.barchart.com Positive Outlook for Both Businesses

Besides the initial guidance for the growth momentum of the spun-off entity, Flex has ambitious long-term plans. For the spun-off company, the objective is to pursue capacity expansion and potential M&A transactions. With the AI infrastructure boom, there seems to be ample headroom for growth over the next five years.

For Flex, management is focused on high-value markets that can drive growth and margin expansion. These include regulated medical devices, automation, and power electronics.

An important point to note is that Flex has been delivering positive free cash flow on a consistent basis. This allows ample headroom for investment. For fiscal 2027, the company is targeting capital expenditures of $1.5 billion at the midpoint, which will be entirely funded through internal cash flows.

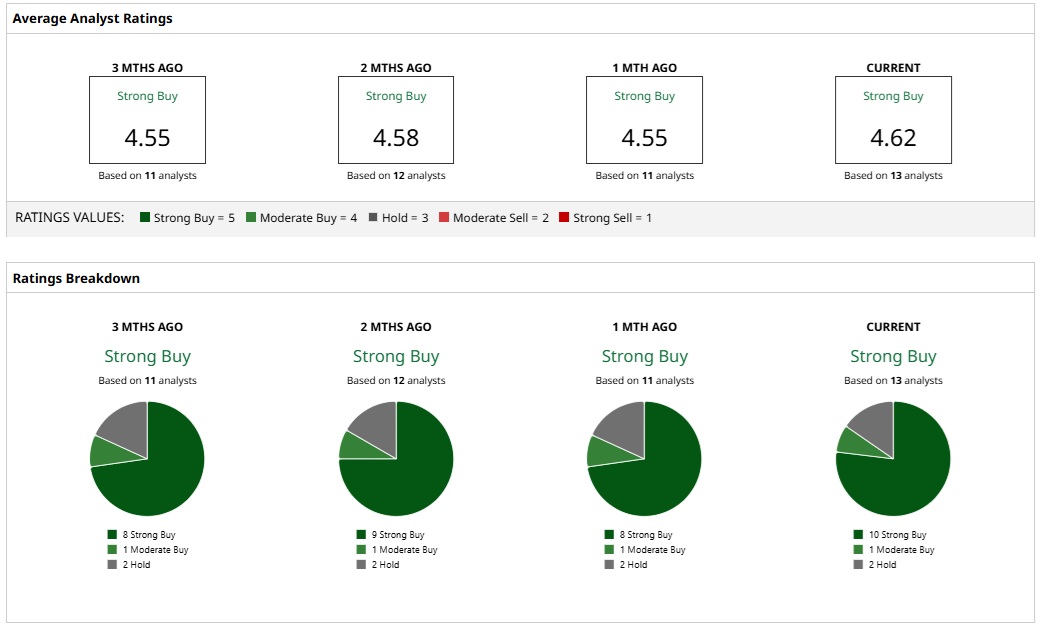

What Do Analysts Say About FLEX Stock?

Based on 13 analysts with coverage, FLEX stock has a consensus “Strong Buy” rating. While 10 analysts have a “Strong Buy” rating for FLEX stock, one has a “Moderate Buy,” and two have a “Hold” rating.

The mean price target of $164.45 represents potential upside of 18% from current levels. Further, the most bullish price target of $203 suggests that FLEX could climb as much as 46% from here.

www.barchart.com

www.barchart.com Conclusion

From a valuation perspective, FLEX stock trades at a forward price-to-earnings (P/E) ratio of 36.3 times. With fiscal 2027 and fiscal 2028 earnings growth expected at 39% and 43%, respectively, valuations are attractive. Further, the spinoff should help unlock value.

In the immediate term, Flex will receive higher visibility with its inclusion in the S&P 500. Flex has flown relatively under the radar, and with several positive catalysts, a rerating is in the cards.

On the date of publication, Faisal Humayun Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Quantum Computing Looks Like Nvidia in 2019. This Could Be the Generational Buy of the Decade. A Short Squeeze Is Underway in Cracker Barrel Stock. What to Know. Dear Flex Stock Fans, Mark Your Calendars for June 22 The $7 Billion Reason Super Micro Computer Stock Is Down Today