Few endorsements carry more weight than a nod from Nvidia (NVDA), CEO Jensen Huang. Speaking in Taiwan, Huang gave a strong thumbs‑up to AI spending and said the returns are now “insanely profitable.” He also singled out Micron Technology (MU) as one of the key winners from this trend.

The timing couldn’t be more telling. Micron has already joined the trillion‑dollar market cap club, driven by surging demand for its high‑bandwidth memory (HBM) chips. These chips are crucial for Nvidia’s AI platforms. Its shares have posted huge gains, with the stock recently hitting new all‑time highs of around $1,100.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Micron CEO Sanjay Mehrotra has backed up that enthusiasm. He says steady demand for advanced memory should keep lifting the company “for years to come.” That view is supported by sold‑out HBM capacity and strong pricing power through 2027.

MU now trades near peak valuations, with its market value at $1.1 trillion. That leaves investors with a big question. Has the market already priced in most of Micron’s AI potential, or is this just the early phase of a longer re‑rating story?

Micron’s Numbers Show Real AI Payoff

Headquartered in Boise, Idaho, Micron Technology designs and manufactures memory and storage semiconductors for data centers, AI systems, PCs, and mobile devices. Its share price has a year‑to‑date (YTD) gain of 212.5% and a 52‑week advance of 681.4%.

www.barchart.com

www.barchart.com The stock offers a forward annual dividend of $0.60 per share for a modest 0.07% yield. This puts Micron on a premium footing, as investors are effectively paying 44.03 times price-to-earnings GAAP (TTM) and 34.43 times price-to-cash flow (TTM) against sector medians of 35.66 times and 19.15 times, respectively.

It was on March 18, that Micron reported its fiscal second‑quarter results for the period ended February 26. Their Q2 revenue climbed to $23.86 billion, up from $13.64 billion in the prior quarter and $8.05 billion a year earlier.

This showed a strong acceleration that matches the rapid ramp in high‑bandwidth memory tied to Nvidia’s latest AI platforms. Its GAAP net income surged to $13.79 billion, or $12.07 per diluted share, marking a clear shift from the more muted profitability investors saw in past cycles.

Their non‑GAAP net income reached $14.02 billion, or $12.20 per diluted share, giving a clearer view of underlying earnings power once certain items are stripped out. Micron’s operating cash flow improved to $11.90 billion, up from $8.41 billion in the previous quarter and $3.94 billion in the same period last year.

Micron’s AI Bets Are Getting Bolder

Micron is building out AI‑focused capacity and products fast. The company agreed to buy a Taiwan microchip plant from Powerchip Semiconductor Manufacturing for $1.8 billion. That deal secures an existing 300mm fab to support advanced DRAM and high‑bandwidth memory.

It has also completed the acquisition of PSMC’s Tongluo P5 site in Miaoli County, Taiwan. That adds roughly 300,000 square feet of cleanroom space now. A second facility is planned to add another 270,000 square feet and is expected to start meaningful shipments in fiscal 2028.

Micron’s product roadmap lines up closely with data center AI demand. They have launched the world’s first high‑capacity 256GB LPDRAM SOCAMM2 module for data center infrastructure, built on a monolithic 32Gb LPDDR5X die. The module uses about one‑third the power and one‑third the footprint of standard RDIMMs.

Additionally, Micron is in high‑volume production of HBM4 36GB 12‑high stacks designed for Nvidia’s (NVDA) Vera Rubin platform. These stacks offer over 2.8 TB/s of bandwidth and about a 20% power‑efficiency gain versus Micron’s own HBM3E. It is also sampling 48GB 16‑high HBM4 cubes that increase the capacity per placement by 33%.

The same product lineup includes the 9650 PCIe Gen6 data‑center SSD in mass production. That drive delivers up to 28 GB/s sequential reads and 5.5 million random read IOPS. And there are SOCAMM2 modules from 48GB to 192GB tuned for Vera Rubin and similar AI systems.

Micron has started 1α DRAM production at its expanded Manassas, Virginia, fab. This is a project of more than $2 billion that will quadruple DDR4 wafer output. It is part of a roughly $200 billion U.S. investment plan across Virginia, Idaho, and New York. About 90,000 American jobs are tied to these efforts.

Analysts Stretch Targets To Match

The next major checkpoint is the fiscal Q3 report on June 24, after the market closes. In the current quarter ending May 2026, the average earnings estimate is $19.40 per share, versus $1.73 a year earlier, indicating a huge year‑over‑year (YOY) growth rate of 1,021.4%.

That kind of jump is pushing analysts to be more upbeat. Raymond James recently lifted its price target on MU to $1,100 from $530 and kept an “Outperform” rating ahead of the June 24 release. The higher target reflects confidence that AI-related demand, including high‑bandwidth memory for Nvidia platforms, can keep earnings strong enough to support a four‑digit share price.

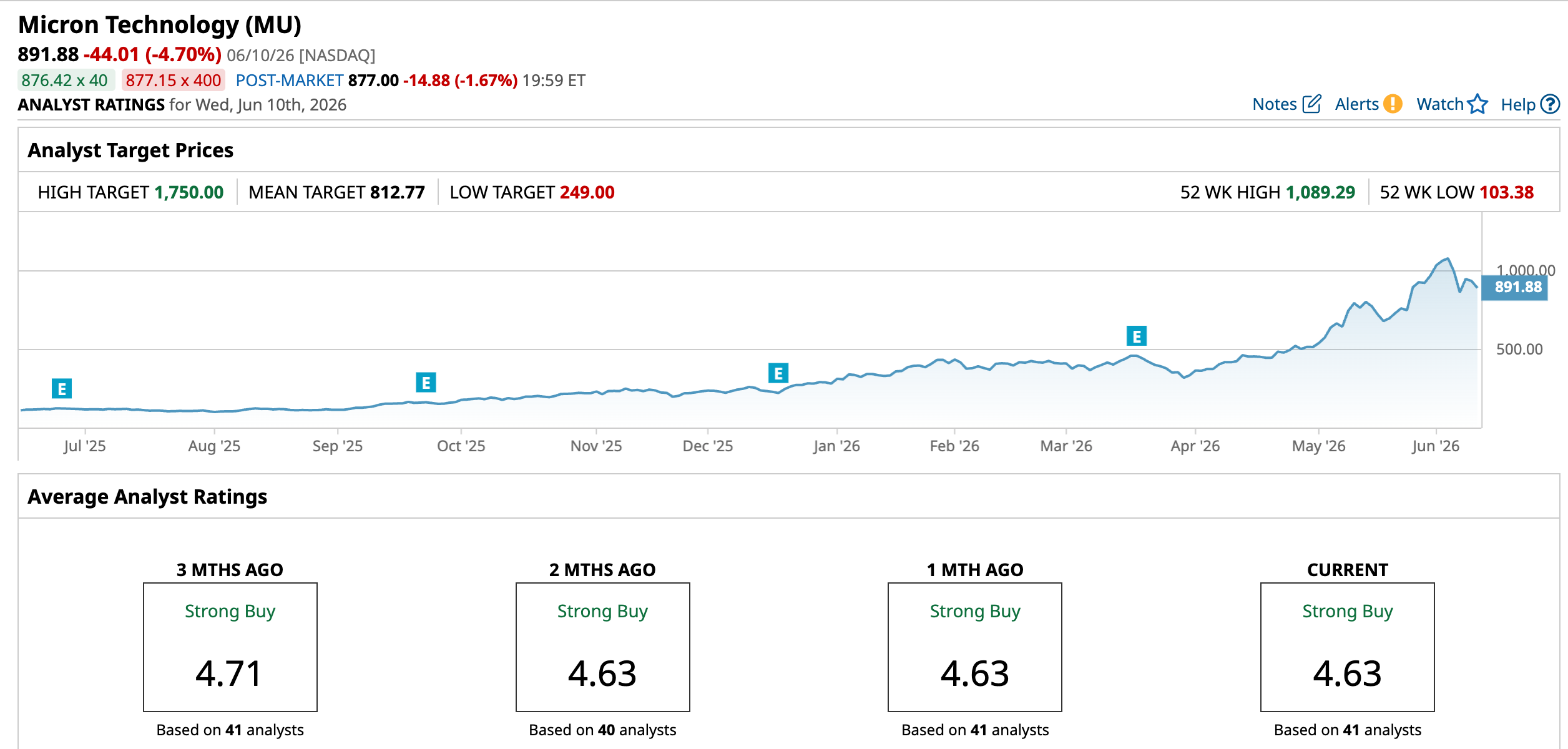

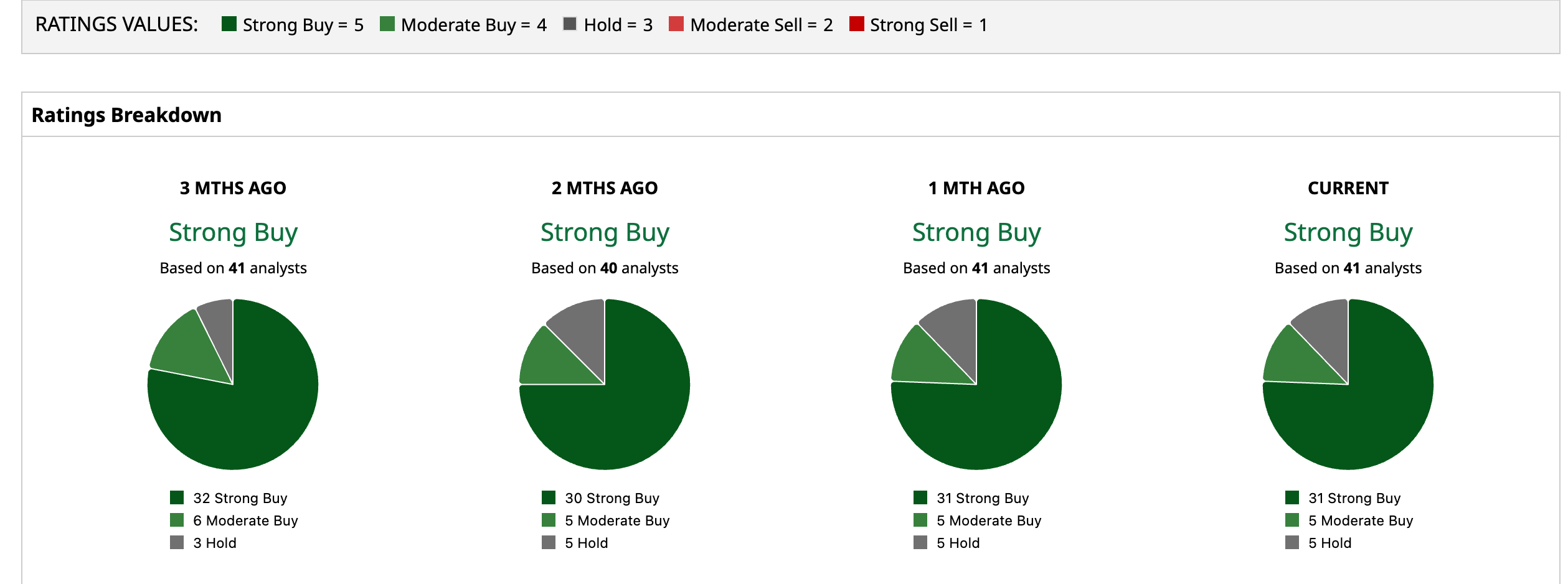

Across the Street, the message is similar. The consensus from 41 analysts is “Strong Buy.” The average price target sits at $812.77, an 8.9% downside to the stock's current price. The Street-high target price of $1,750 implies a potential upward climb of 96% from here.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com Conclusion

Micron has turned Jensen Huang’s vote of confidence into hard numbers, from triple‑digit earnings growth to record AI‑driven cash flow. Its valuation already reflects a lot of that optimism, so a smooth, straight‑up move from here looks unlikely. Bottom line, MU now looks more like an “accumulate on pullbacks in an AI uptrend” story than one that has completely run out of upside.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

FuelCell Energy Missed on Q2 Revenue. Investors Are Betting That AI Data Centers Will Save the Day. This AI Infrastructure Stock Is Up 650% This Year. Wall Street Still Sees More Upside. Cathie Wood Is Buying the Dip in Broadcom Stock Micron Got a Major Vote of Confidence From Nvidia’s Jensen Huang on AI Returns. I Still Wouldn’t Chase MU Stock Here.