China’s e‑commerce market has been stuck in a profit squeeze, with platforms cutting prices to keep shoppers spending while demand stays patchy. During last year’s Singles’ Day, the world’s biggest online shopping event, sales growth slowed to roughly half the pace seen in 2024 as bargain hunters traded down to cheaper options.

So when the big platforms rolled out fresh discount pushes and “billion‑yuan subsidy” campaigns ahead of the 2026 June 18 shopping festival, regulators were already on alert.

More Yield, Less Trap: Sign up free to get Barchart’s daily Dividend Investor newsletter straight to your inbox.

That scrutiny landed squarely on Alibaba Group (BABA) and JD.com (JD) on Thursday, June 11, when officials hauled in platform executives and publicly accused them of misleading shoppers with overstated discounts, saying the real subsidies were much smaller than advertised.

The warning hit Alibaba Group hard. The stock slid again after already dropping 41% from its 52‑week high of $192.67, adding to a long history of run‑ins with regulators that has included billions in fines since Beijing’s first big antitrust case in 2021. The fact that this latest slap came in the middle of the 618 shopping season made it sting even more.

So is this just another headline that passes, or a sign that even a revamped, AI-focused Alibaba Group still cannot escape Beijing’s grip on its most profitable levers?

Inside Alibaba’s Latest Financials

Alibaba runs a big online marketplace at the core of its business, and builds on that with cloud, digital media, and logistics, earning mainly from commissions, ads, and other paid services.

In the market, though, the stock has struggled. Over the past 52 weeks it is up marginally at 0.35%, and year-to-date (YTD) it is off 22.72%.

www.barchart.com

www.barchart.com Even with that slide, Alibaba Group trades at 16.7 times forward price-to-earnings, still richer than the sector’s roughly 15.97 times, so investors are paying a premium for its scale and assets.

The company now pays a dividend, with an annual yield of about 0.82%, which works out to a 0.95 annualized yield based on recent payouts. The most recent dividend of 1.030 was declared on June 11, 2026, and is paid once a year, with a forward payout ratio of 30.45% and only one year of back‑to‑back increases so far.

The latest March‑quarter numbers tell a mixed story. Revenue grew 3% year-over-year (YOY) to RMB 243.4 billion (approximately $35.3 billion), or 11% if you strip out the businesses Alibaba Group has sold, but adjusted EBITA fell 84% as it poured money into technology, quick commerce, and user experience.

Net income jumped 96% to RMB 23.5 billion (about $3.4 billion), mainly helped by mark‑to‑market gains and the absence of last year’s disposal losses, while non‑GAAP net income dropped to just RMB 86 million (around $12 million), showing how thin underlying profits have become. Cash also took a hit. Operating cash flow fell 66%, and free cash flow flipped to an RMB 17.3 billion (roughly $2.5 billion) outflow as Alibaba Group stepped up spending on AI infrastructure and its commerce ecosystem.

Key Drivers Sustaining Business Momentum

Alibaba Group is now leaning on AI to keep the story moving. It rolled out the beta version of its Happy Horse AI model for broad use across its ecosystem, and added the Happy Oyster AI model to target video game development, pushing into more creative and consumer-facing niches that sit well beyond its core shopping apps. On the back end, it has shifted its full-stack AI platform from incubation to full commercialization and rolled out new AI tools aimed squarely at lifting cloud and AI-service revenue, even if that means more margin strain for now.

To keep things tighter, Alibaba Group has folded its separate AI efforts into a single unit and is preparing an IPO for its chip arm to cut dependence on foreign suppliers and build up local AI hardware. On the infrastructure side, the 10,000-chip AI cluster unveiled in China and the launch of its first physical robot shows the group's deeper push into heavy compute and robotics at the same time regulators are squeezing its room to compete on discounts.

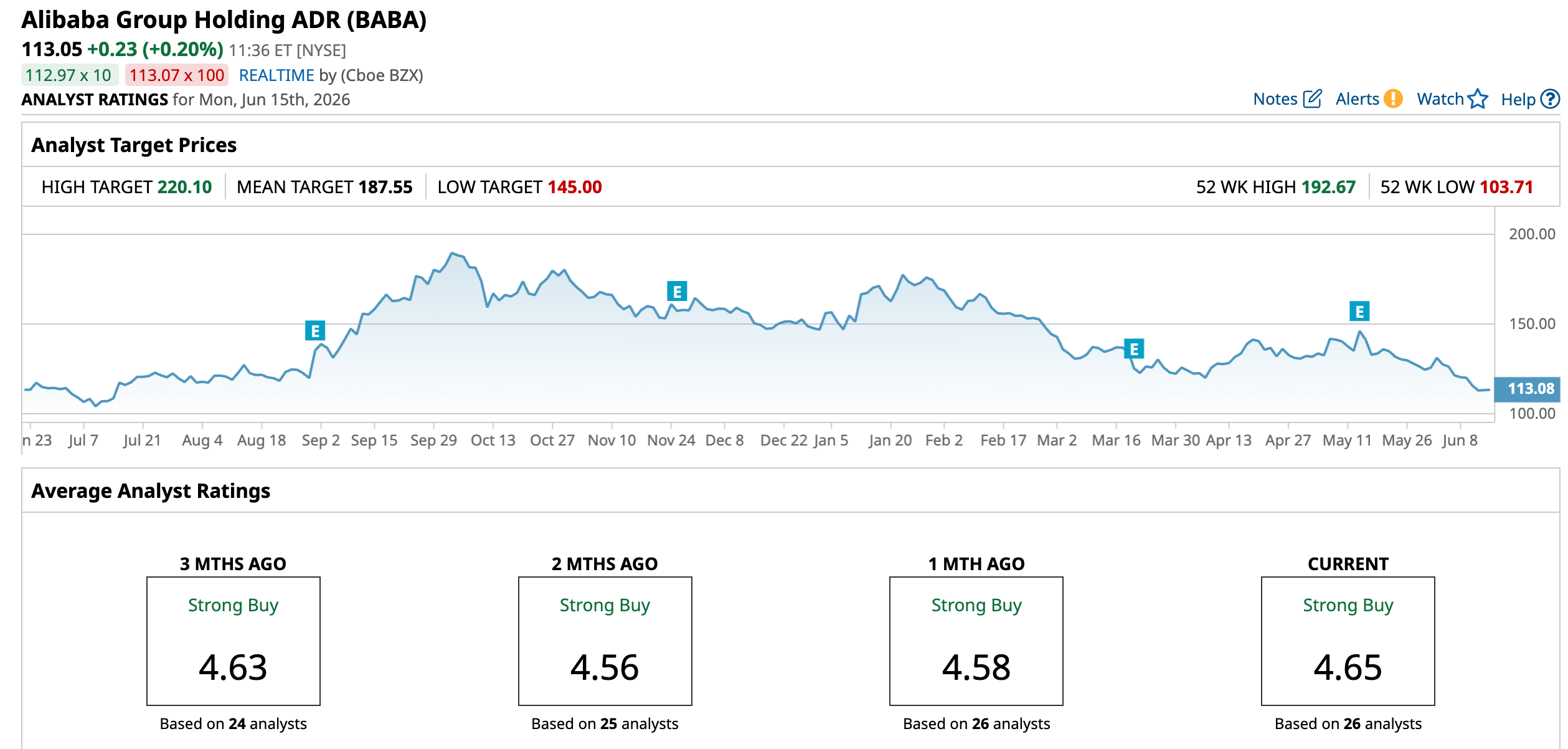

Analyst Sentiment and Price Outlook

The next earnings release is scheduled for September 4, 2026. For the June 2026 quarter, analysts are looking for earnings of $2.44 per share, up from $1.89 a year ago, which works out to about 29.10% growth.

For the September 2026 quarter, the bar is $1.26 versus $0.44 last year, a much steeper 186.36% jump. Further out, the Street is modeling full‑year EPS of $6.75 for fiscal 2027, more than double the prior year’s $3.23, a 108.98% increase.

In April, Barclays kept its “Overweight” rating but nudged its target down from $190 to $186, saying Alibaba Group’s higher spending is the cost of building a leading AI franchise, not a sign that the story is broken.

After Alibaba Group’s Q3 miss, Susquehanna also stuck with a “Positive” call, cutting its target from $190 to $170 and highlighting the hit to near‑term profits from heavy AI investment, while still pointing to solid positions in Chinese e‑commerce, cloud, and AI as the backbone of the long‑term case.

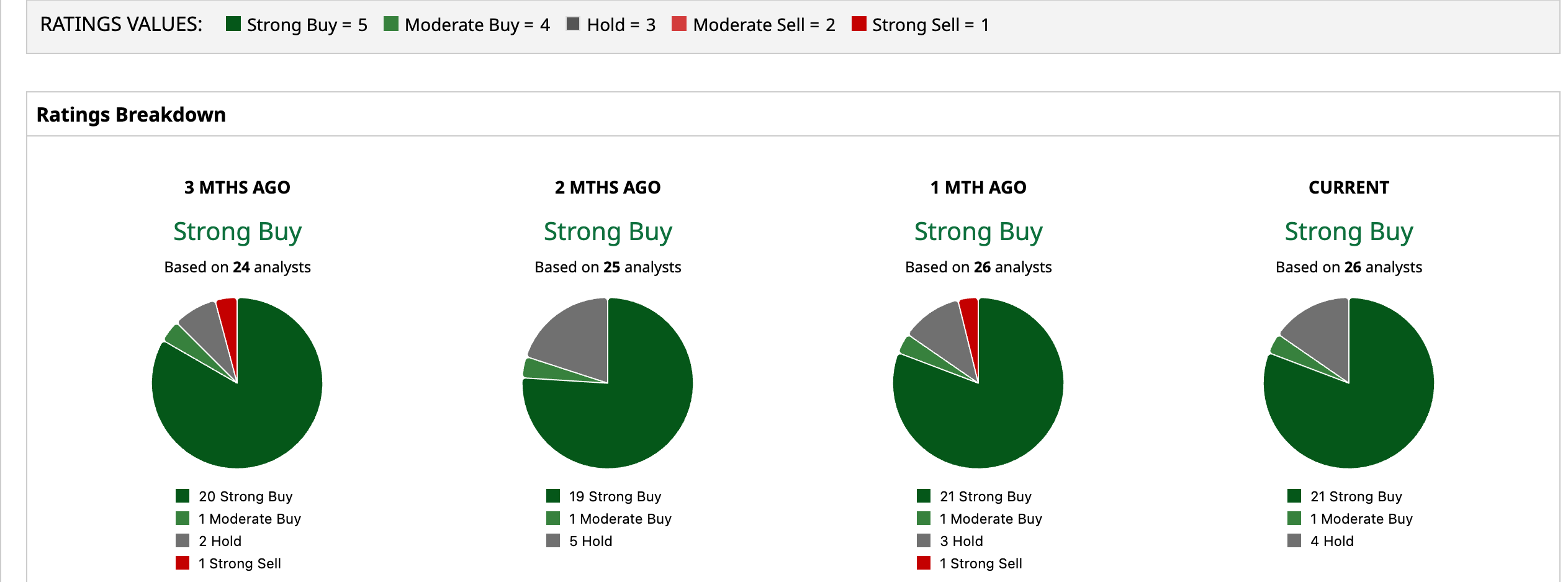

Of 26 analysts, 21 rate BABA a “Strong Buy”, one rates it a “Moderate Buy,” while the remaining four are siding with a “Hold.” With an average target of $187.55, the stock could potentially have a 66% climb, and with a Street-high price point of $220.10, BABA may rise 94.7% from here.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com Conclusion

At this point, Beijing’s rebuke looks more like another sharp reminder of who sets the rules than a lasting break in Alibaba’s story. The core tension is clear: regulators are forcing discipline on the subsidy arms race just as Alibaba is spending heavily to scale AI, cloud and infrastructure, which is crushing near-term margins but building out longer term earnings power. With the stock still trading well below analysts’ targets and the business pivoting toward higher value AI and services, the setup leans toward a grind higher rather than a collapse, though headline risk and policy surprises are likely to keep BABA volatile on the way up.

On the date of publication, Ebube Jones did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

Beijing Rebukes Alibaba and JD.com Over Misleading Discount Practices. How to Play Leading Chinese Stocks Here. A Major Short Squeeze Could Be Brewing in Cracker Barrel Stock A $1.24 Trillion Reason to Buy Dell Stock Now Why Wells Fargo Is Warning That Surging AI Token Costs Is a Death Knell for Hyperscaler Stocks Like Meta and Microsoft