Alphabet (GOOG) (GOOGL) has been one of the best-performing mega-cap tech stocks over the past year, with shares soaring 111.46%. By comparison, Amazon (AMZN) has gained just 16%, while Microsoft (MSFT) has declined 15.83% during the same period.

While Alphabet stock has more than doubled, the tech giant’s recent quarterly results suggest the rally may be far from over. Alphabet's aggressive AI investments are already driving business gains and revenue backlog through stronger user engagement in Search, advertising efficiency, and accelerating adoption of Google Cloud services.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

As enterprises continue to increase AI-related spending, Alphabet could capture a larger share of that demand. With AI increasingly embedded across its advertising, search, and cloud ecosystems, Alphabet has multiple catalysts that could support earnings growth and drive GOOGL stock to new highs.

www.barchart.com

www.barchart.com Alphabet Poised to Deliver Solid AI-Led Growth

Alphabet’s massive investment in AI is translating into stronger financial results across its businesses. From Search and YouTube to Cloud and AI, the platform has strengthened its existing revenue streams and created strong monetization opportunities.

The first quarter highlighted this momentum. Alphabet extended its streak of double-digit revenue growth to 11 consecutive quarters in Q1, with revenue rising 22% year-over-year (YOY) to $109.9 billion. Google Search generated $60.4 billion in revenue during the quarter. Features such as AI-generated overviews are helping improve user engagement while creating new monetization opportunities, positioning Search for continued growth.

AI is also strengthening Alphabet's advertising business. YouTube advertising revenue increased 11% YOY, supported by ongoing improvements in targeting and campaign performance. The integration of Gemini AI models into Google's advertising platform is helping advertisers generate better results, which could further reinforce Alphabet's competitive advantage and pricing power.

Another key catalyst is Google Cloud. The segment delivered another quarter of accelerating growth, driven by surging demand for AI products and infrastructure. Revenue increased 63% YOY, surpassing $20 billion. In addition, Google Cloud’s backlog nearly doubled sequentially to $462 billion, highlighting strong customer demand and providing substantial visibility into future revenue growth.

Management expects more than half of this backlog to be recognized as revenue over the next two years, indicating that the company’s growth trajectory will remain solid. Demand is driven by enterprise AI solutions, infrastructure services, and Tensor Processing Unit (TPU) hardware.

Revenue from products built on Alphabet's generative AI models surged nearly 800% YOY, while Gemini Enterprise recorded strong growth in paid users. The company is also seeing rising demand from large enterprise customers. New customer acquisition has accelerated, major contract wins are increasing, and enterprises are investing in Google's AI capabilities.

For instance, Google reported that new customer acquisition doubled compared with the same period last year, signaling growing market acceptance of its AI and cloud offerings. Large enterprise deal activity was equally impressive, with the number of contracts valued between $100 million and $1 billion doubling YOY. And, Alphabet secured multiple deals worth more than $1 billion.

Overall, Alphabet’s investments in AI position the company to drive strong future growth and strengthen its leadership within the AI ecosystem.

Alphabet Stock Still Has More Upside

Alphabet has already delivered impressive gains, with shares rising more than 100% over the past year. However, the company's AI-driven growth story appears far from over.

Several catalysts could continue fueling growth. Google Cloud's expanding backlog points to strong future revenue visibility, while growing enterprise adoption of Gemini-powered AI solutions is creating solid monetization opportunities. At the same time, Google's core advertising business remains resilient, providing a solid base for future growth.

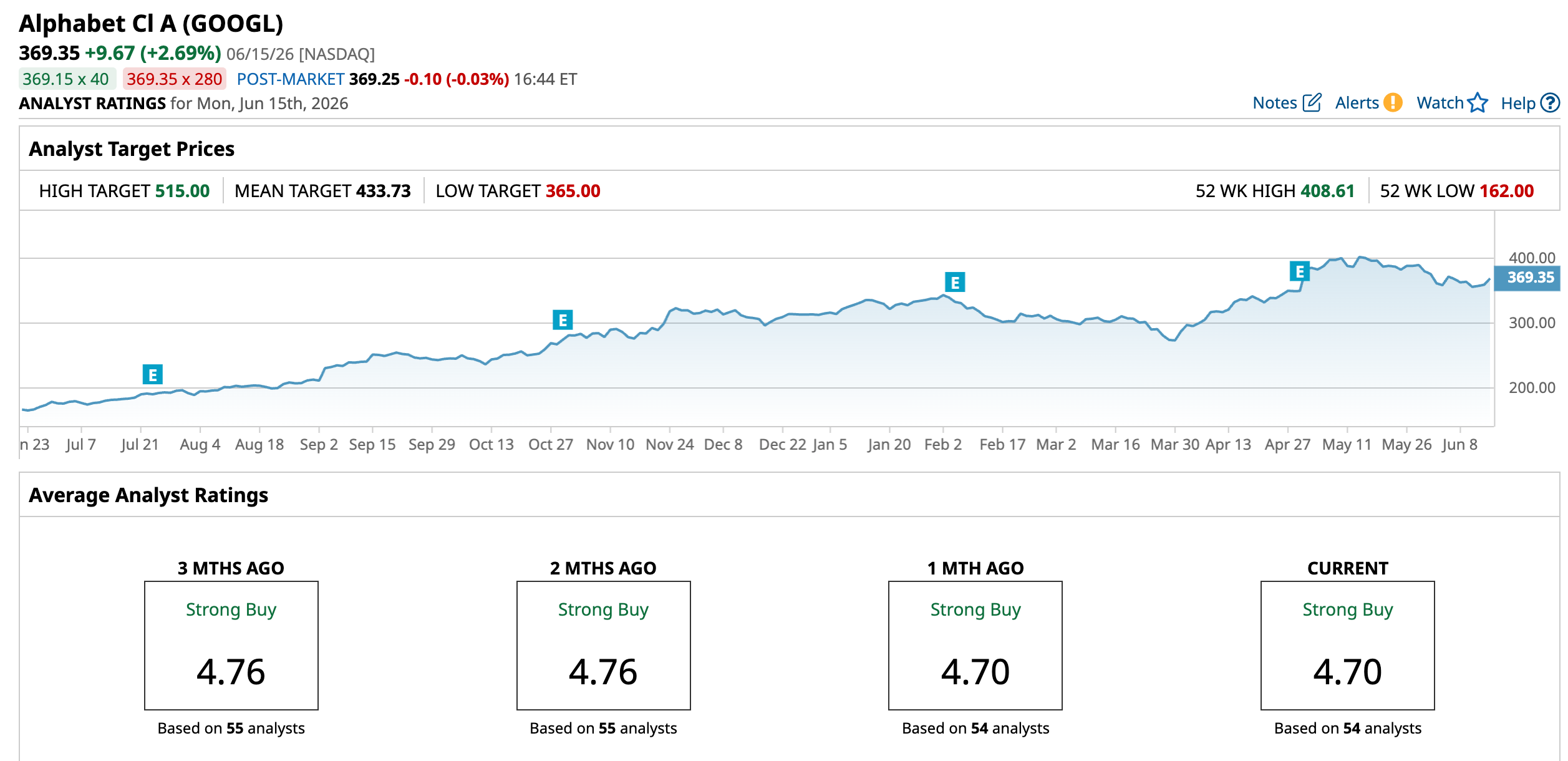

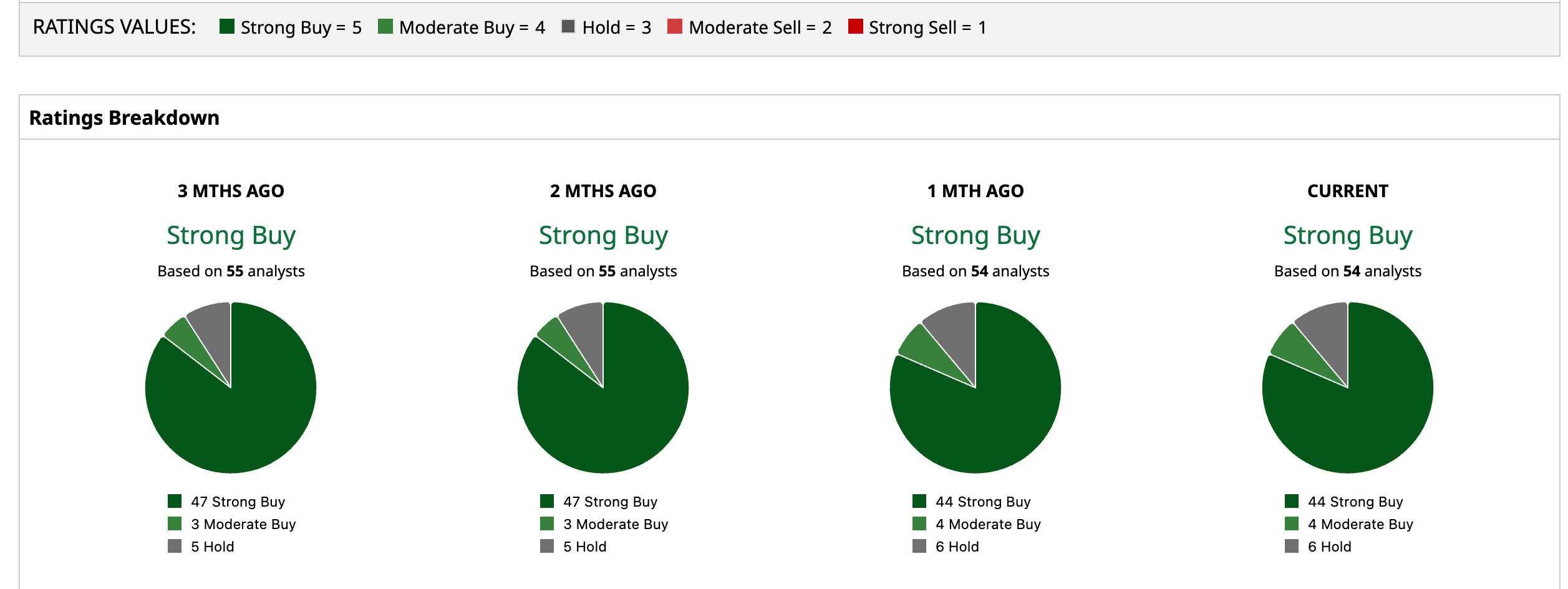

Wall Street remains optimistic, with analysts maintaining a “Strong Buy” consensus rating. In addition, GOOGL’s valuation appears reasonable relative to its earnings growth potential. Overall, Alphabet appears well-positioned to deliver strong growth ahead, suggesting the stock could still have significant upside. The highest price target for GOOGL stock is $515, implying 39.4% upside from here.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com On the date of publication, Amit Singh did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

ROKU Stock Alert: What to Know as Fox Buys Roku in $22 Billion Deal Why GOOGL Stock May Have More Room to Run Even After a 100% Rally Why Wedbush Says WWDC Was the First Step for Apple to Add $100 to Its Stock Truist Just Upgraded Datadog Stock. Here's Why.