Founded in 1984, Dell Technologies (DELL) started as a personal computer (PC) company. For decades, investors largely viewed Dell as a PC maker whose earnings were heavily tied to the computer market. Today, however, the company looks very different. Its biggest growth opportunities are coming from artificial intelligence (AI) infrastructure, servers, storage, and data centers, rather than laptops and desktops. And this opportunity has led Dell’s business to explode, with a massive AI backlog in the first quarter.

Investors are pouring money into DELL stock as the company evolves from just a PC maker to an AI and data center powerhouse. The stock is up 209% year-to-date (YTD), massively outperforming the S&P 500 Index ($SPX) 8% gain. Here’s why DELL stock still looks attractive despite its recent rally.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

www.barchart.com

www.barchart.com The PC Business Is Now the Bonus, Not the Main Attraction

Dell built its reputation by building and selling PCs to customers. But now Dell's future is increasingly being shaped by AI rather than PCs. In the first quarter of fiscal 2027, Dell booked $24.4 billion in AI orders and generated $16.1 billion in AI server revenue. Through its Dell AI Factory initiative, the company offers integrated solutions that combine compute, storage, networking, software, and services. This allows customers to move AI projects from testing environments into full-scale production more quickly.

Encouragingly, its AI backlog currently stands at $51.3 billion, indicating that customers are making long-term commitments to its AI platform. Management also noted that its AI pipeline remains several times greater than the current backlog. Furthermore, Dell's traditional infrastructure business continues to attract recurring customer relationships and attractive margins. Traditional server and networking revenue surged 92% year-over-year (YoY) as businesses refresh aging systems, expand computing capacity, and prepare their data centers for increasingly demanding AI workloads. Total revenue in the quarter surged 88% to $43.8 billion, while the bottom line climbed an impressive 214% YoY to $4.86 per share.

Ironically, Dell's PC business remains healthy even though it is no longer the primary reason investors own the stock. Commercial revenue increased 18% during the quarter, marking the seventh consecutive quarter of growth. Management also highlighted that roughly one-third of the installed PC base is now four years old or older. That leaves a lot of room for upgrades, including AI-powered applications.

Dell Has Become an AI Infrastructure Giant

The strongest argument for Dell’s long-term investment case now is that Dell no longer depends on just PCs to succeed. The PC business can continue generating revenue and profits while AI infrastructure, enterprise servers, storage, and data center modernization drive the company's next phase of growth. Its partnership with industry leaders such as Nvidia (NVDA), Crowdstrike (CRWD), OpenAI, Alphabet (GOOG) (GOOGL), Palantir (PLTR), and ServiceNow (NOW) has the potential to strengthen its AI ecosystem even further.

Management predicts AI server revenue of roughly $60 billion in fiscal 2027, with total revenue growth of 45% over the prior year. The company is confident the momentum will continue beyond fiscal 2027, as Dell is increasingly becoming a one-stop shop for servers, storage, networking, and AI infrastructure.

The Bottom Line on DELL Stock

Investors who still look at Dell as just a PC maker may be missing the bigger picture. The company has evolved into a major AI infrastructure player, yet the stock trades at only 21x forward fiscal 2027 estimated earnings, which are expected to surge 78% YoY.

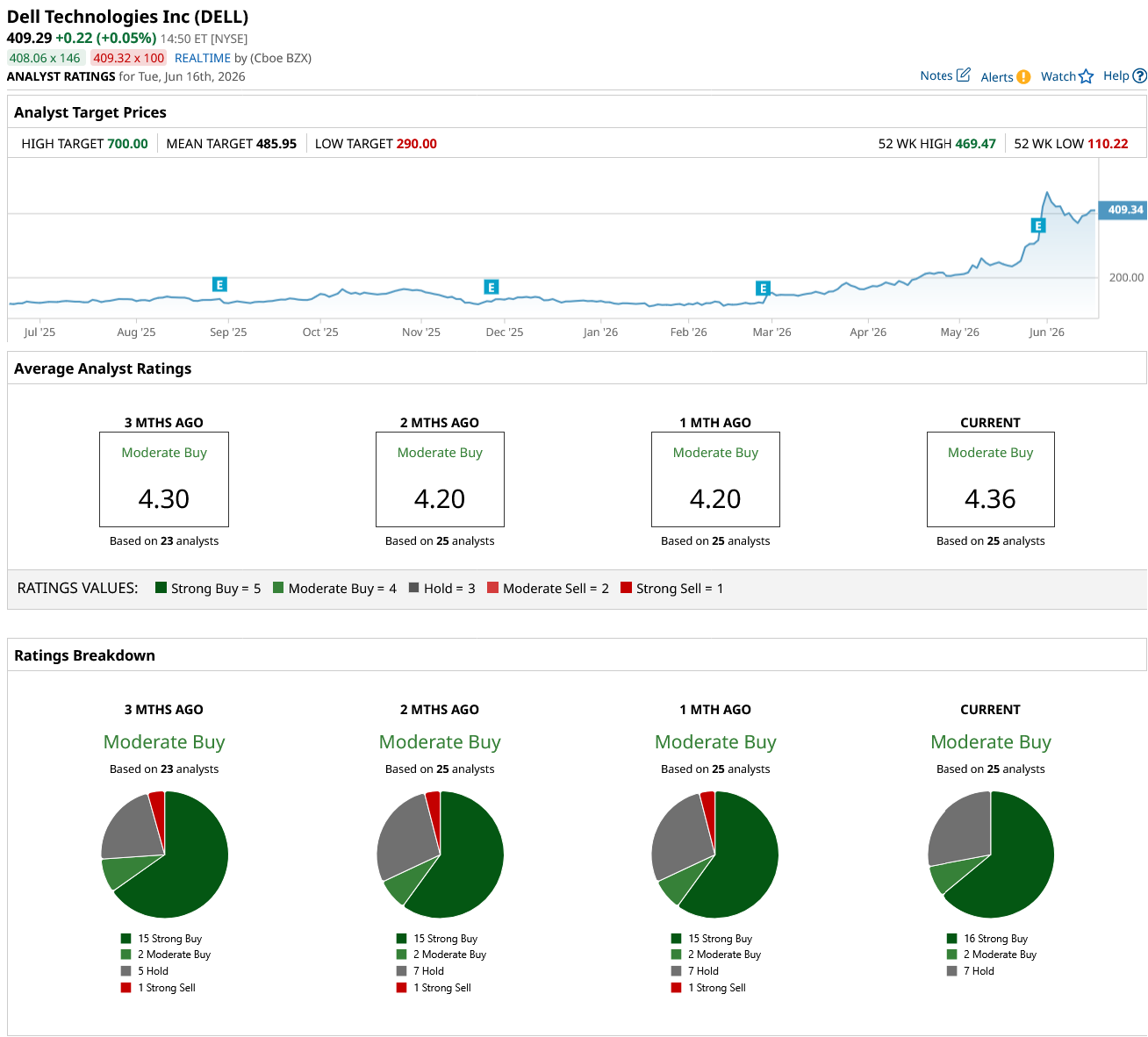

Dell’s strong first quarter and management’s confidence for fiscal 2027 and beyond have prompted analysts to raise target prices. The average target price of $485.95 suggests the stock can climb 19% from current levels. Furthermore, Susquehanna upgraded DELL stock to “Positive” from “Neutral” and has assigned the highest price estimate of $700, which implies an upside potential of 71% over the next 12 months.

Overall, DELL stock holds a consensus “Moderate Buy” rating on the Street. Of the 25 analysts covering the stock, 16 rate it a “Strong Buy,” two say it is a “Moderate Buy,” and seven rate it a “Hold.”

www.barchart.com

www.barchart.com On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

This Lesser-Known Stock Is a ‘Bunker’ for Your Capital Thanks to Technical Strength The Battle of the Musks: Why Cathie Wood Sold Tesla Stock to Buy SpaceX The Dell Story Is No Longer Just About PCs. Here’s Why the Stock Still Looks Undervalued. CVNA Stock Alert: What to Know as Carvana Expands Into New Vehicles