Wolfe Research analysts resumed coverage of Palantir (PLTR) with a “Peer Perform” rating this morning — an upgrade from their previous “Underperform” rating — reflecting the firm’s reassessment of PLTR’s positioning within the enterprise AI landscape.

The investment firm did not assign a specific price target but described the company as one of the most compelling stories in enterprise software and artificial intelligence, using the phrase “Too Big to Ignore” to characterize Palantir’s growing market significance.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Still, Palantir stock is currently down about 25% versus the start of this year.

www.barchart.com

www.barchart.comWhy Wolfe Research Turned Bullish on Palantir Stock

The central thesis behind Wolfe’s upgrade revolves around Palantir’s proprietary Ontology framework, which the firm identified as its key differentiator.

Ontology functions as a database that organizes critical connections within business workflows, making them more accessible for users to understand, manage, and modify.

Wolfe argued that while advanced AI models can solve complex problems, they often lack the business context necessary to deliver actionable results.

PLTR bridges that gap by combining artificial intelligence capabilities with an organization’s existing data and workflows through its Foundry and Gotham platforms, it added.

PLTR Shares Have a Massive Addressable Market

Wolfe highlighted Palantir’s evolution from a custom software provider into a leading enterprise AI platform that helps organizations apply advanced AI models to real-world business challenges.

Its analysts pointed to exceptionally strong growth metrics, including net sales retention of 150%, year-over-year revenue growth of 85% that continues to accelerate, and a 97% increase in backlog.

Average revenue per customer has climbed 40% year-on-year, which supports their base-case for revenue to grow at a 39% compound annual rate through 2029 with potential upside to 55% growth annually.

Wolfe also identified a massive growth runway, citing an estimated $385 billion total addressable market across more than 100,000 enterprise firms. This suggests Palantir has barely scratched the surface of its potential customer base despite its rapid expansion.

Moreover, the broader AI ecosystem continues to validate PLTR’s positioning as the company was recently named among enterprise adopters of Nvidia’s (NVDA) agentic AI agent frameworks alongside key technology companies.

How Wall Street Recommends Playing Palantir

The broader market context is also worth noting: Palantir’s valuation premium, while still elevated at roughly 68x sales, has been overtaken by the newly public SpaceX that’s going for about 110x.

This relative repositioning may make PLTR appear somewhat less extreme on a valuation basis compared to the newest entrant in the high-growth tech cohort, even as it, nonetheless, remains one of the most expensive names in the S&P 500 Index ($SPX).

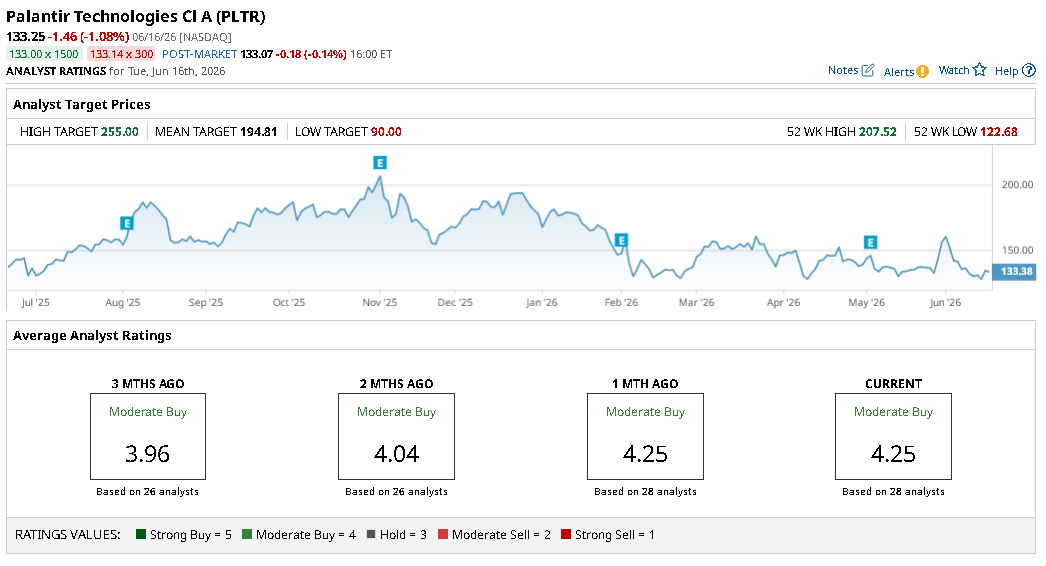

The valuation concerns likely saw Palantir shares edge lower on Tuesday, despite Wolfe’s upgrade. But Wall Street more broadly continues to recommend buying them at current levels, with potential upside to nearly $195 on average.

www.barchart.com

www.barchart.comThis article was created with the support of automated content tools from our partners at Sigma.AI. Together, our financial data and AI solutions help us to deliver more informed market headline analysis to readers faster than ever.

On the date of publication, Wajeeh Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

This Analyst Just Upgraded Palantir Stock. Here's Why. Rocket Lab vs. Redwire: 1 Stock Has the Stronger Growth Story for the Next Decade Rocket Lab Stock Sinks After SpaceX IPO. If You’re In It for the Long Haul, Buy the Dip. The $2.7 Billion Reason YUM Stock Is Up Today