SpaceX (SPCX) has been moving at warp speed, and Wall Street has been hanging on for the ride. In just three trading sessions, Elon Musk’s space and technology giant pulled off something remarkable. The company surged past Amazon (AMZN) in market cap, becoming the fifth-most valuable company on the planet and shaking up the pecking order of corporate America.

That’s no small feat. Amazon spent nearly three decades building its empire. SpaceX, meanwhile, raced ahead in a matter of days, powered by a wave of investor optimism and a growing belief that Musk’s ventures still have plenty of runway left.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

The stock’s latest jump pushed SpaceX’s valuation to around $1.4 trillion, in comparison to Nvidia (NVDA), Alphabet (GOOG) (GOOGL), Apple (AAPL), and Microsoft (MSFT).

What makes this rally even more interesting is that investors are not just betting on today’s numbers. They are betting on Musk himself. From reusable rockets and Starlink to new ambitions in artificial intelligence, many see SpaceX as a collection of future growth engines rather than a company defined by current profits. Some have even compared Musk’s long-term vision to the value-creating magic Warren Buffett built at Berkshire Hathaway (BRK.A) (BRK.B).

SPCX hit the brakes on Wednesday after its blistering post-IPO run, but SpaceX has still been climbing the ranks at breakneck speed. With the dust settling after its meteoric debut, where does SPCX go from here, and how should investors play it?

About SpaceX Stock

Founded in 2002 and headquartered in Starbase, Texas, SpaceX has grown from an ambitious rocket startup into one of the world’s most valuable technology companies. Led by Elon Musk, the company operates across space, connectivity, and artificial intelligence.

Its Starlink business delivers high-speed satellite internet to consumers, businesses, and governments around the world through a growing network of low-Earth orbit satellites. On the space side, SpaceX designs, builds, and launches reusable rockets, including Falcon 9 and Falcon Heavy, while also developing Starship and operating Dragon spacecraft for commercial customers and government missions.

Beyond rockets and satellites, SpaceX has expanded into AI. The company runs the Grok large language model, offers AI products for consumers and businesses, operates the X platform, and is building the computing infrastructure needed to support advanced AI systems. Together, these businesses position SpaceX at the intersection of several fast-growing industries.

After pulling off the biggest IPO Wall Street has ever seen, shares of Elon Musk’s space and AI giant soared 19.6% in their first full day of trading as investors rushed to grab a piece of one of the market’s most interesting stories.

The debut reflected strong demand from both institutions and everyday investors, with many betting that Musk can once again turn bold ideas into massive businesses. But as the dust began to settle, the conversation shifted from excitement to execution. Some market veterans say much of the early action has been driven by traders chasing momentum rather than long-term investors. And after such a huge run, the stock gave back some ground as analysts started asking whether SpaceX would eventually grow into its sky-high valuation.

As Peter Boockvar of One Point BFG Wealth Partners put it, excitement can only carry a stock so far. Eventually, the fundamentals have to do the heavy lifting. He believes the upside is there, but it could take years for the business to fully justify its enormous market value.

Meanwhile, fresh catalysts are already lining up. Options trading kicked off with heavy bullish activity, showing that investors are eager to keep betting on the company’s future. SpaceX also plans to unlock shares for resale before the traditional six-month post-IPO lockup period expires, while the IPO’s greenshoe option provides another cushion against wild swings.

The stock’s first few days have been a blastoff, and now comes the harder part of proving that the business can keep pace with the hype, as evidenced below.

www.barchart.com

www.barchart.com SpaceX's Revenue Growth and Rising Losses

SpaceX is not trying to squeeze out every dollar of profit, but instead, it is spending heavily to build businesses that management believes could be much larger down the road. In the first quarter of 2026, SpaceX generated $4.7 billion in revenue, up 15.4% year-over-year (YOY). Growth came mainly from a rising number of Starlink subscribers and stronger demand for AI offerings tied to X and Grok. The Space division grew at a slower pace as launch activity and the timing of government contracts created some headwinds.

The company’s spending spree, however, grabbed most of the attention. SpaceX posted an operating loss of $1.94 billion and a net loss of $4.3 billion. Even so, adjusted EBITDA reached $1.1 billion, suggesting the core business remained healthy. The biggest cash outlay came from AI, where SpaceX invested $7.7 billion in the quarter. By comparison, Connectivity received $1.33 billion, and the Space segment accounted for $1.05 billion.

That same pattern showed up throughout 2025. Revenue reached $18.7 billion, while adjusted EBITDA totaled $6.58 billion. Yet aggressive investment pushed operating losses to $2.6 billion and net losses to $4.9 billion. Capital spending included $12.7 billion for AI infrastructure, $4.18 billion for Connectivity, and $3.8 billion for Space operations.

Perhaps the biggest surprise from SpaceX’s S-1 filing was that the company is evolving into far more than a rocket maker. Management increasingly sees AI infrastructure as a major growth engine. Beginning in late 2026, Alphabet’s Google is expected to pay about $920 million per month to tap SpaceX’s AI computing platform, which includes roughly 110,000 Nvidia GPUs. That translates to more than $11 billion in annual revenue from a single customer.

Another large agreement with Anthropic could bring combined annual revenue from the two contracts to roughly $26 billion and more than $70 billion over their lifetimes. Those deals alone could eventually surpass the company’s entire 2025 revenue.

And there’s another asset hiding on the balance sheet. SpaceX owns 18,712 Bitcoin, now worth well over $1 billion, giving investors exposure not only to rockets, satellites, and AI, but also to cryptocurrency.

Analysts tracking the company expect its fiscal 2026 losses to be $0.91 per share, and in fiscal 2027, the loss per share is estimated to narrow by 74.7% YOY to -$0.23.

What’s Wall Street’s Take on SpaceX Now?

Ever since SpaceX rang the opening bell on Nasdaq, the company has been front and center, with analysts and investors kicking the tires on everything from its valuation to its place in the next wave of tech. The stock has been on a tear, but not everyone is ready to jump aboard without asking a few tough questions.

CFRA analyst Keith Snyder rates SpaceX a “Sell” with a $115 target, arguing the company is leaning heavily on Starship, which is still far from full commercial deployment. He warns that delays could slow several growth plans. Snyder also points to SpaceX’s cash-hungry business model, noting that investors often price in Musk’s big dreams without fully accounting for the possibility that ambitious projects can take years or hit roadblocks.

Steve Westly, founder of The Westly Group and a former Tesla (TSLA) board member, believes the excitement around SPCX is real, especially among retail investors, who poured roughly $100 billion into the stock. But he also warned that the honeymoon period may not last forever. Building rockets, satellites, and AI businesses is no easy task, and if SpaceX falls short of the growth targets it outlined before going public, investors could quickly lose patience after a few disappointing quarters.

Others are even more cautious. For instance, Matthew Maley, chief market strategist at Miller Tabak, said the IPO was executed brilliantly but argued that SPCX is simply too expensive. While the stock does not have a formal price-to-earnings ratio, at current levels, its valuation implies a P/E multiple approaching 100 times, far above Nvidia’s roughly 31 times and Apple’s near 36 times. Morningstar analyst Nicolas Owens has echoed that view, calling the shares significantly overvalued.

Still, the bulls are not backing down. Maley himself believes patient investors could be rewarded over the long haul. Westly remains optimistic as well, pointing to Elon Musk and SpaceX President Gwynne Shotwell as a powerful team capable of tackling the steep challenges ahead.

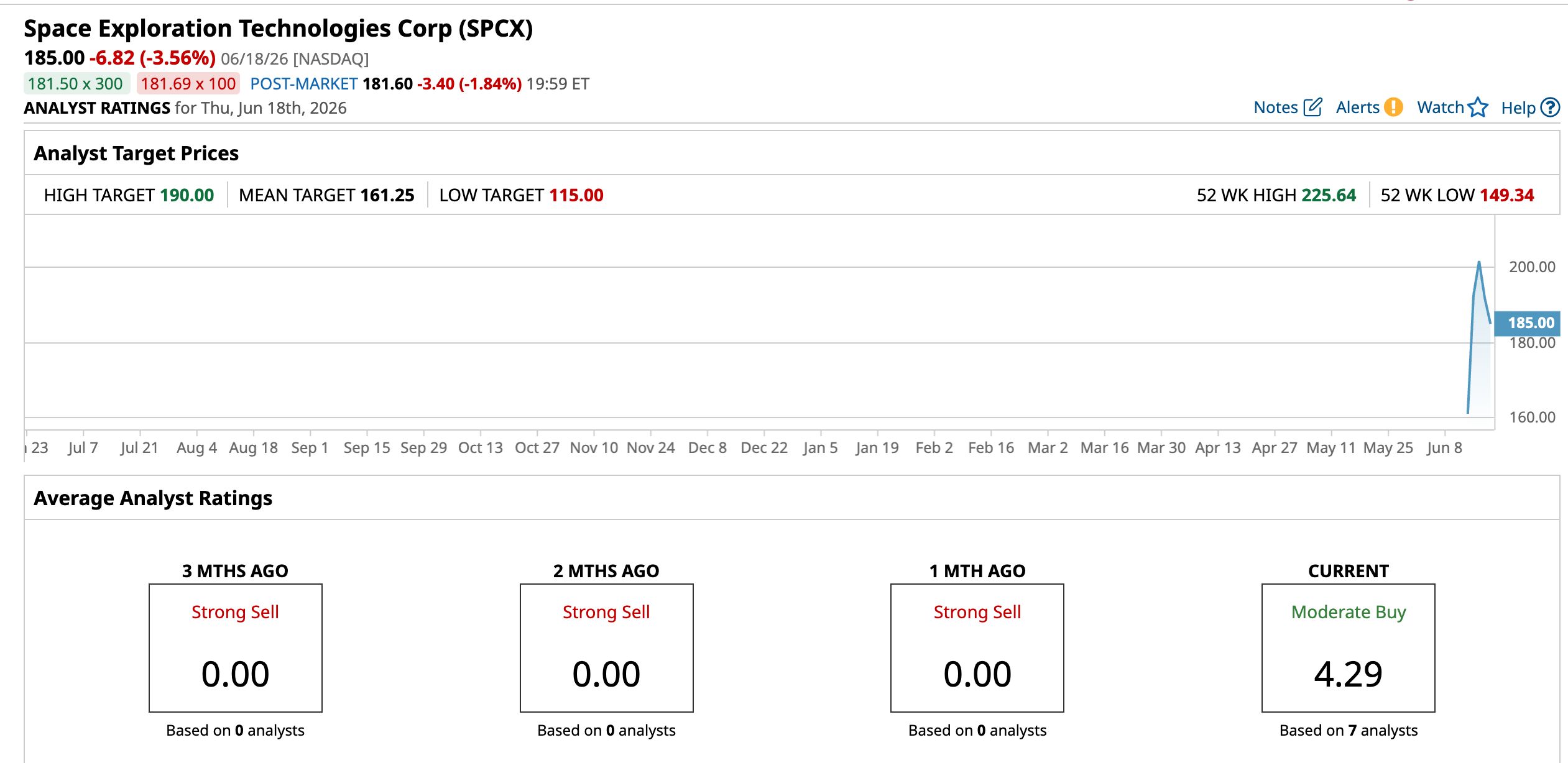

SpaceX has already raced past New Street’s $161.25 price target, but the firm’s most optimistic view stretches much further. In its long-term bull-case scenario, New Street sees the stock reaching $330 by 2040. That outlook assumes the global space economy grows to $20 trillion, with SpaceX controlling about half of it. To support that vision, the firm estimates SpaceX would need roughly $127.7 billion in AI revenue, $57.9 billion from connectivity services, and $9.7 billion from space operations by 2030, implying annual revenue growth of around 60% over the next five years.

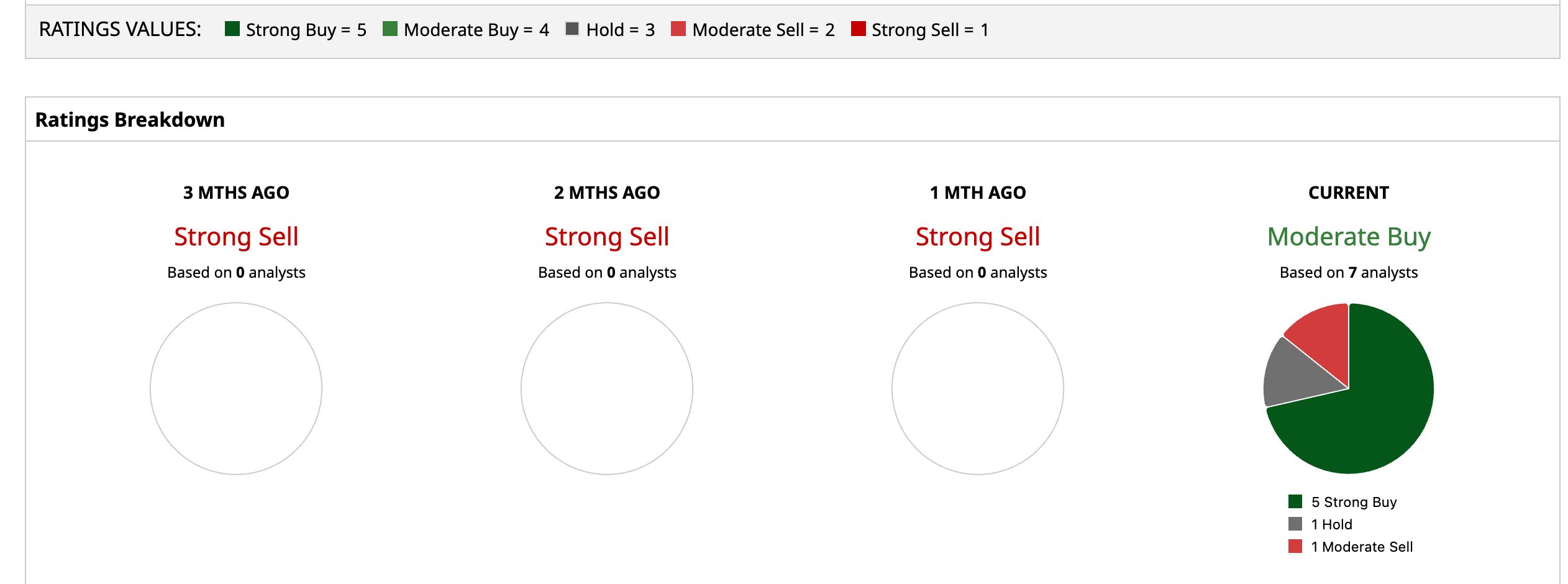

The debate on Wall Street is far from settled. Bears see a stock that has already flown too close to the sun, while bulls believe SpaceX is just getting off the launch pad. Wall Street is still kicking the tires on how fast SpaceX can grow into its sky-high valuation, but the bulls seem to have the wind at their backs. SPCX stock carries a “Moderate Buy” rating overall. Of the seven analysts covering the stock, five are pounding the table on a “Strong Buy,” one is playing it safe with a “Hold,” and the remaining one is waving a cautious flag with a “Moderate Sell.”

After its stellar run, SPCX has sailed past expectations, climbing above the average analyst target and ever-so-near Wall Street’s biggest bull case of $190.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com Final Thoughts on SpaceX

SpaceX had muscled its way into fifth place among the world’s most valuable companies, surpassing Amazon’s market cap. SPCX’s breathtaking climb shows that investors are willing to bet on the jockey as much as the horse. As CFRA’s Keith Snyder notes, SpaceX carries a “Musk premium,” with many shareholders willing to buy into the story and look beyond today’s numbers.

Still, investors should avoid getting carried away. The stock has been hotter than a Fourth of July barbecue, and expectations are through the roof. Long-term believers may want to keep their eye on the horizon, while newcomers might be wise not to put all their eggs in one basket. After all, on Wall Street, trees don’t grow to the sky.

On the date of publication, Sristi Suman Jayaswal did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

SpaceX Is Now the Fifth Most Valuable Company on the Planet. How to Play SPCX Stock Here. Plug Power Stock’s Turnaround Is Starting to Look Real Record AI Backlog and Swelling Cash Flows Make HP Enterprise Stock Attractive Strategy Sells Shares to Buy Bitcoin. What This Means for MSTR Stock.