Micron (MU) is heading into earnings with Wall Street already moving the goalposts. That is usually a sign of confidence, but it also raises the pressure. Stifel and Wedbush both lifted their price targets before the report, and that tells you analysts are still getting more bullish on the AI memory story. The catch is that MU stock has already sprinted much higher.

So ahead of earnings, investors are asking the same question from two angles. Is the business still getting better? And is the stock still worth buying after such a huge run? Let's try to find out.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

A Huge Run Has Already Changed the Story

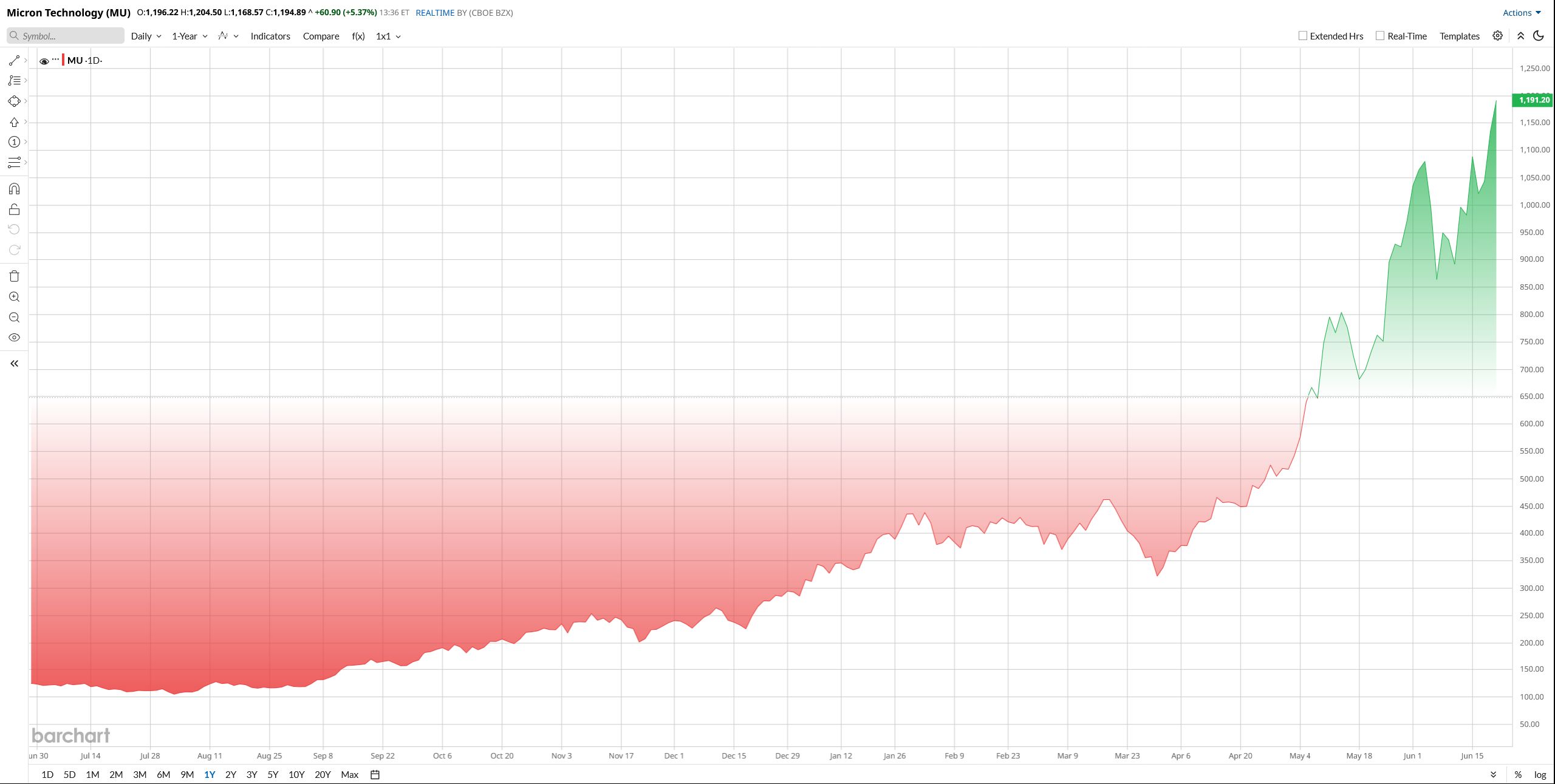

Micron's stock has been on fire in 2026. It is up about 317% year-to-date (YTD) and roughly 864% over the past year with dividends reinvested. That is not a normal move. That is the kind of move you get when the market thinks a company is in the middle of a powerful cycle. MU stock has also kept reacting to every sign of tighter memory supply and stronger AI demand. In other words, buyers are not just chasing the chart. They are chasing the earnings power behind it.

Micron still looks rich on some metrics. Its price-to-book ratio is about 17.7 times, which is well above the sector median. That is a premium valuation, no question.

But the forward P/E tells a different story. Micron trades at about 19 times forward earnings, which is below the sector median. So the stock is not screaming cheap, but it is also not priced like a total bubble on earnings. That is why the debate around MU is so split. Bulls see growth. Bears see a stock that has already run a long way.

www.barchart.com

www.barchart.com What Happened Ahead of Earnings

The big move came when Stifel and Wedbush both raised their MU stock price targets before earnings. Stifel lifted its target to $1,500 from $550. Wedbush raised its target to $1,300 from $550.

That kind of move tells a lot because analysts usually do not make huge changes unless they think the setup has improved in a real way. The takeaway was clear. Both firms think AI demand is still pulling hard on memory pricing, and both think Micron has room to benefit when the company reports on June 24.

Also, Micron is not just riding the cycle. It is spending to stay in it. The company is investing more than $25 billion in fiscal 2026 capex, and it is pushing ahead with its new megafab project in New York. It also recently produced 1-alpha DRAM in Virginia, its most advanced memory ever made in the U.S.

Investors liked that message. Micron hit a fresh record after the upgrades, which shows the market is still willing to pay up for the AI story. But it also means expectations are now very high. When a stock is already at a peak, even a strong report can turn into a “not good enough” reaction if guidance does not impress.

Micron’s Last Quarter Was Blistering

Micron's second quarter was the kind of report that makes people sit up. Revenue came in at $23.8 billion, up from $8.05 billion a year ago. Net income reached $13.79 billion, compared with $1.58 billion in the same quarter last year. Adjusted EPS came in at $12.20, up sharply from $1.56.

The business was strong across the board. Cloud memory revenue was $7.75 billion. Core data center brought in $5.69 billion. Mobile and client contributed $7.71 billion. Auto and embedded added $2.71 billion.

Free cash flow was $6.9 billion, and Micron ended the quarter with $16.7 billion in cash, marketable investments, and restricted cash. That gives it plenty of flexibility. CEO Sanjay Mehrotra said memory has become a strategic asset in the AI era, and that message fits the numbers.

Micron also guided for revenue of $33.5 billion, plus or minus $750 million, and adjusted EPS of $18.90, plus or minus $0.40.

Note that the Micron earnings are due on June 24 after the market close.

Analysts Still Like MU Stock, but the Bar Is High

Other than Stifel and Wedbush, the analyst crowd is still positive overall. UBS recently raised its target to $1,625 and argued that Micron deserves to trade more like a top-tier AI chip name. Morgan Stanley remains at “Overweight” with a $1,050 target. Goldman Sachs is the more cautious voice, with a target closer to $900 and a reminder that memory is still a cyclical business.

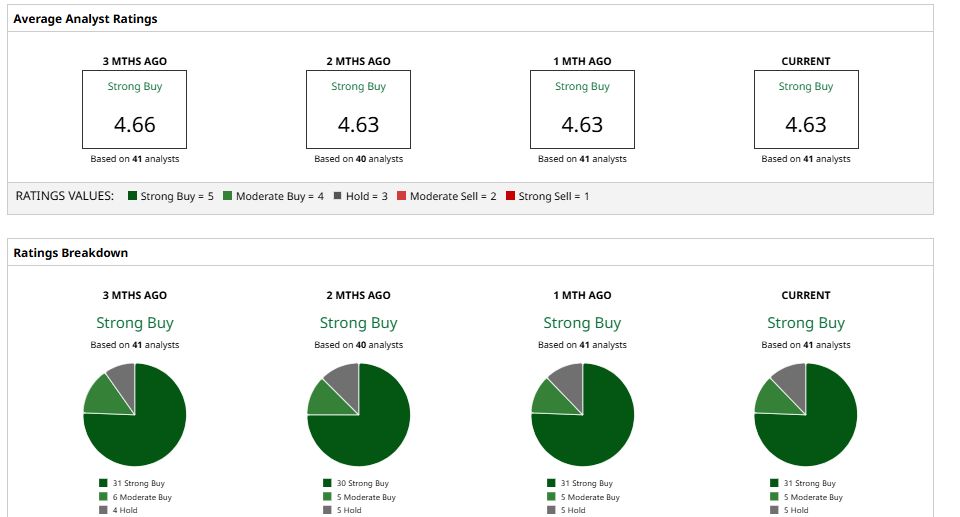

Moreover, MU stock has a “Strong Buy” consensus based on 41 analysts. The average target is $940.63, which is about 21% below the current stock price. That tells you the Street is bullish on the business, but the stock has already outrun a lot of the targets.

That is the whole Micron setup right now. The story is strong. The numbers are strong. But the stock has also already done a lot of the work.

www.barchart.com

www.barchart.com On the date of publication, Nauman Khan did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

SpaceX Is Apparently a Value Stock as Schwab Adds SPCX to Its Popular SCHV ETF Jabil Shares Jumped on Earnings as AI Demand Boosts Its Business. JBL Stock Is No Longer Cheap. These 2 Veteran Wall Street Firms Just Revamped Their Micron Stock Price Targets Ahead of Earnings D-Wave Just Unveiled a Major Quantum Breakthrough. QBTS Stock Looks Ready for Another Surge.