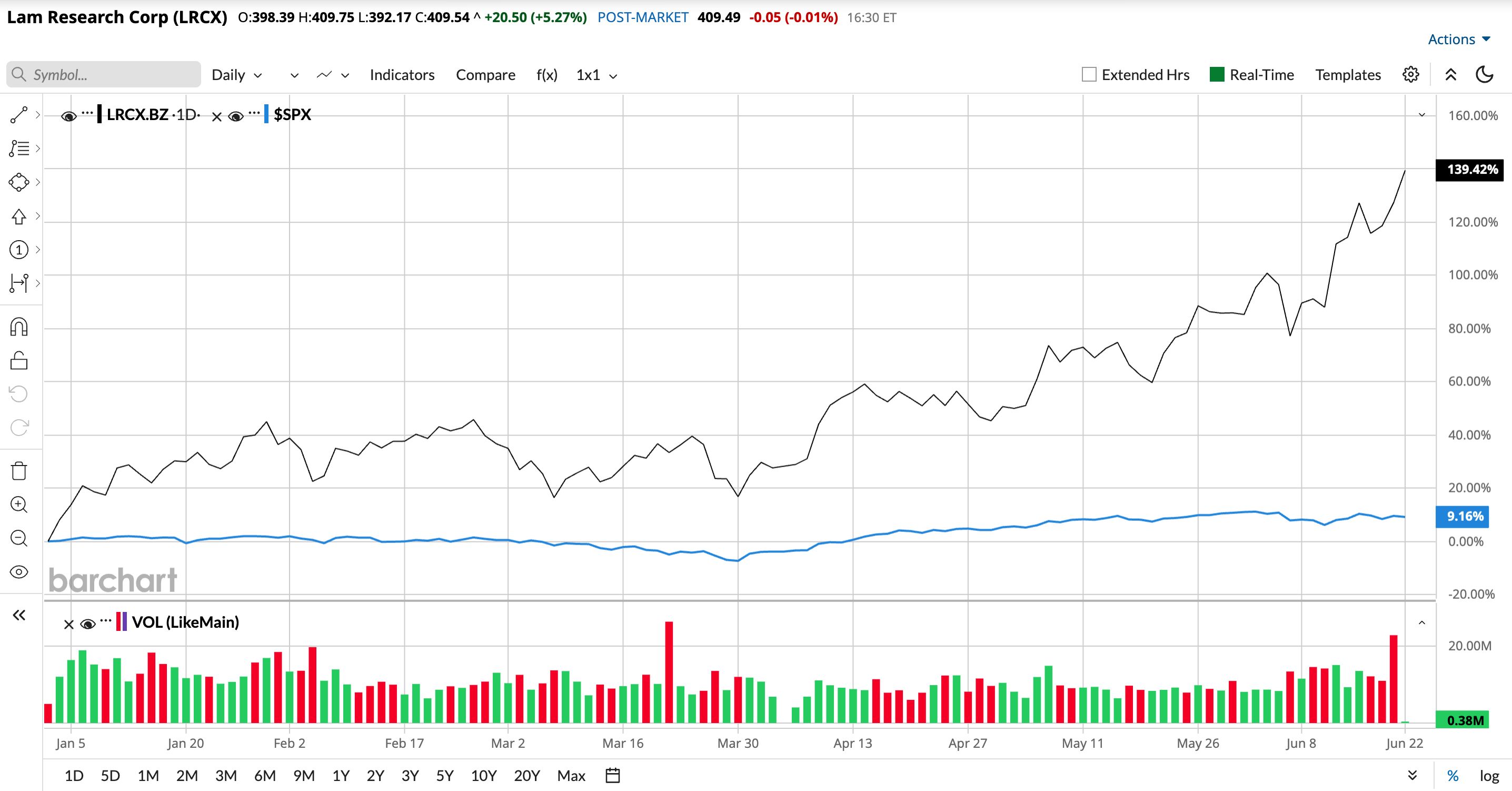

Lam Research (LRCX) shares have rallied a massive 139.25% so far this year, massively outperforming the broader market. This critical AI supplier is cashing in by supplying the deposition, etching, and wafer fabrication equipment needed to manufacture the advanced chips and memory devices powering AI. After a rally like this, investors would be assuming that most of the upside is gone. But Lam’s story is far from finished.

www.barchart.com

www.barchart.com About Lam Research

On the surface, Lam’s business might look small compared to semiconductor powerhouses like Nvidia (NVDA) or Advanced Micro Devices (AMD). However, it is a key supplier of equipment, without which chip manufacturing would be harder. Lam manufactures and supplies equipment used by chipmakers to manufacture chips on silicon wafers inside fabs. Its main products include etch (carving the tiny features into the wafer), deposition (laying down the ultra-thin films that build the chip), strip & clean (removing residues and keeping wafers pristine), software, and other fab productivity tools.

More Top Stocks Daily: Go behind Wall Street’s hottest headlines with Barchart’s Active Investor newsletter.

Its customers are the companies that make chips, DRAM, NAND, HBM, and advanced packaging structures, such as Micron (MU), Taiwan Semiconductor Manufacturing Company (TSM), and Samsung, among others. Although Lam is not the only equipment supplier, it would be very hard to replace Lam without sacrificing time, yield, and performance.

Lam’s Financial Model Still Looks Powerful Even After the Stock’s Huge Run

Lam Research’s March quarter showed that the AI spending cycle is accelerating. Revenue grew 24% year-over-year (YOY) to $5.84 billion. Adjusted earnings per share (EPS) increased 16% YOY to $1.47, beating consensus estimates. In the March quarter, memory accounted for 39% of systems revenue, up 34% sequentially. Within that, DRAM alone reached 27% of systems revenue, up 23% YOY. Foundry also accounted for 54% of systems revenue, up 35% YOY, led by robust spending at both the leading edge and mature nodes, while advanced packaging remained a particularly strong growth area. Lam expects advanced packaging revenue to increase by more than 50% in calendar 2026.

Furthermore, its services business is another valuable part of its business model, as services revenue tends to be more stable and margin supportive than pure systems sales. The company now has more than 100,000 chambers installed, which generates ongoing revenue from maintenance, updates, software, and productivity improvements. Its Customer Support Business Group (CSBG) delivered its first-ever $2 billion-plus quarter, increasing 25% YOY.

Why this AI Infrastructure Stock May Still Have Room to Run

For the June quarter, Lam guided for $6.6 billion in revenue (plus or minus $400 million) and EPS of $1.65 (plus or minus $0.15), along with a 50.5% gross margin. Lam even anticipates revenue in the second half of calendar 2026 to exceed that in the first half, as demand remains strong. This is an encouraging sign for the stock, which has already doubled this year. Lam currently anticipates that wafer fab equipment (WFE) spending would total roughly $140 billion by 2026. But the interesting thing is that Lam's served available market (SAM) as a percentage of WFE is expected to rise slightly over the mid-30% range by 2026. Management believes the company is on track to achieve a high-30% SAM share within the next few years.

Lam continues to invest in its next phase of expansion from a strong financial position, while also rewarding its shareholders. Capital expenditures rounded up to $332 million in the March quarter to support a second manufacturing facility in Malaysia and lab investments in the U.S. and Taiwan. Yet, the company ended the quarter with $4.8 billion in cash, having spent roughly $800 million on buybacks, $326 million on dividends, and retiring $750 million of unsecured notes. It still has $4.3 billion remaining under its authorized buyback program. Lam is still expanding production and investing in technology because management anticipates a longer runway ahead.

While Lam may appear to be just another semiconductor supplier, its strength lies in the messy, difficult, and high-value steps of chip manufacturing. Its exposure to the fastest expanding segments of semiconductor capital spending, such as advanced NAND, HBM, next-generation DRAM, foundry inflections, and advanced packaging, adds to the bullish case for this AI stock.

The Bottom Line on LAM Stock

As AI becomes more advanced, the more difficult chip making will become, making Lam’s business even more valuable. Investors have most likely realized Lam’s growing potential and this optimism, as evident from Lam’s premium forward price-to-earnings multiple of 68 times, based on 2026 earnings, which are expected to increase by 37% YOY. Analysts further predict earnings to increase by another 41% in 2027.

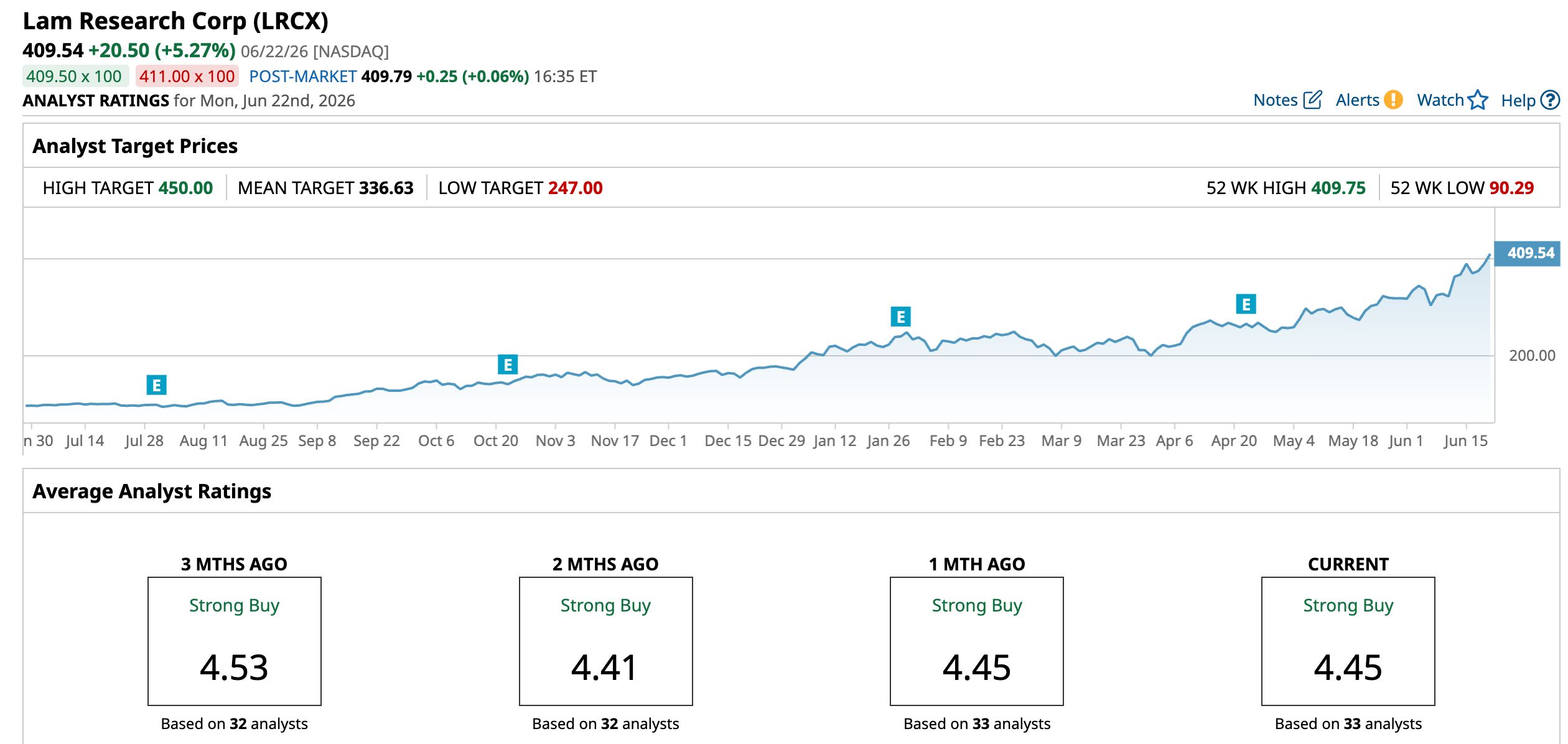

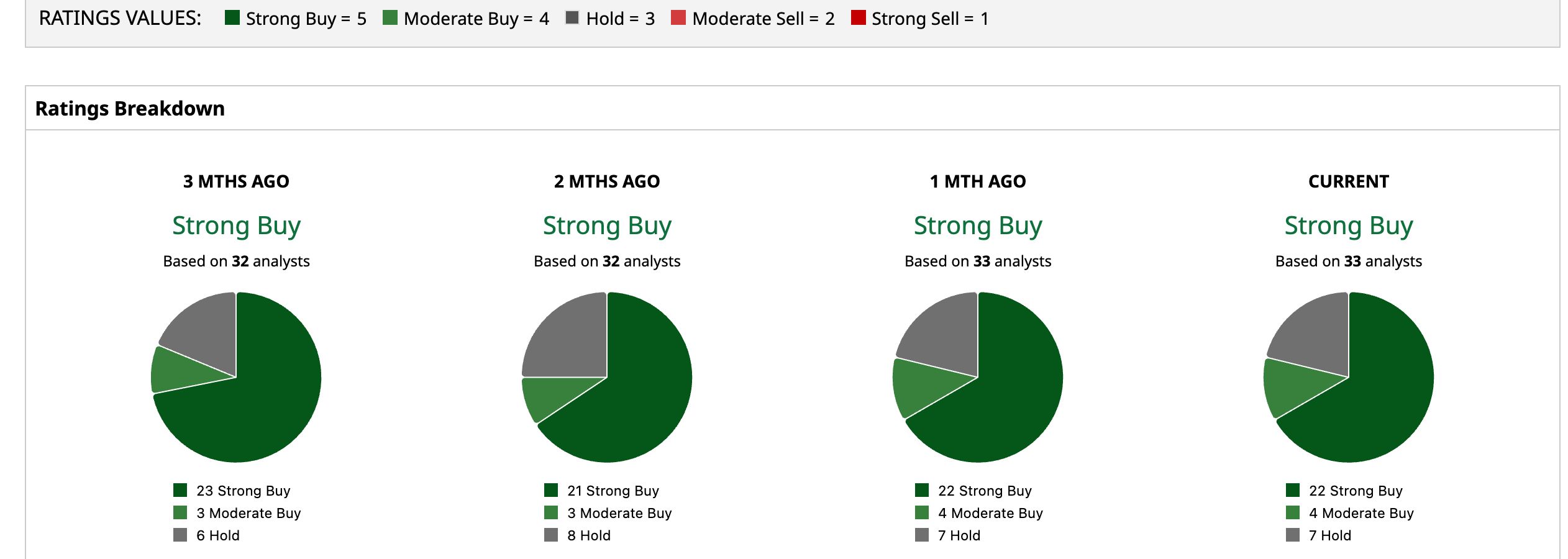

Overall, on Wall Street, analysts rate Lam Research stock a “Strong Buy.” Of the 33 analysts covering the stock, 22 offer a “Strong Buy” rating, four have a “Moderate Buy,” and seven analysts offer a “Hold” rating. The stock has crossed its average target price of $336.63. But the Street-high estimate of $450 implies that shares can rally as much as 9.9% over the next 12 months.

www.barchart.com

www.barchart.com  www.barchart.com

www.barchart.com On the date of publication, Sushree Mohanty did not have (either directly or indirectly) positions in any of the securities mentioned in this article. All information and data in this article is solely for informational purposes. For more information please view the Barchart Disclosure Policy here.

More news from Barchart

As Qualcomm Diversifies, Growth Acceleration Will Support Stock Upside Lam Research Stock Is Up 114% So Far in 2026. This AI Infrastructure Stock Is Far From Finished. The $11 Billion Reason Abbvie Stock Is Up Today SpaceX Is the World’s Most Ambitious Company. You Should Still Wait for a Pullback in SPCX Stock Before You Buy.